Overview

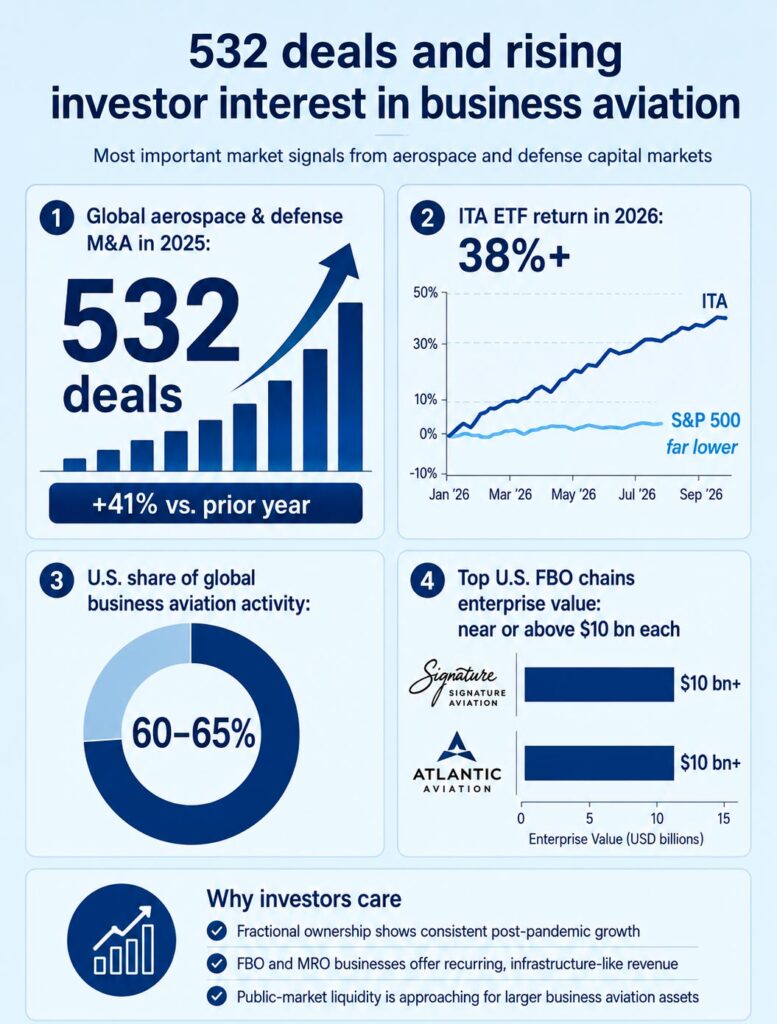

The aerospace and defense industry has entered its busiest capital markets cycle in decades. Global M&A announcements rose 41% in 2025 to a record 532 transactions, as defense priorities in the U.S. and international markets increased demand for next-generation technologies and specialized capabilities, according to Jefferies’ report.

The IPO window has reopened for aerospace and defense companies. Private equity has also become more active across the sector. The defense market, measured by the ITA ETF, has returned more than 38% this year, far ahead of the S&P 500.

Growth across aerospace and defense has been uneven in recent years. During the post-COVID recovery, maintenance, repair, and overhaul companies, fixed base operators, and aftermarket suppliers outperformed.

Key highlights

- Global aerospace and defense M&A announcements rose 41% to 532 transactions in 2025.

- The defense sector, measured through the ITA ETF, returned more than 38% this year.

- The U.S. accounts for about 60% to 65% of global business aviation activity.

- Signature Aviation and Atlantic Aviation have enterprise values near or above $10 bn each.

- Business aviation investment opportunities now center on FBOs, MROs, parts distribution, aviation software, and disciplined operators.

Original equipment manufacturers lagged because production constraints and supply chain pressure limited output. The current cycle looks broader, with nearly every major segment participating in the upturn, according to Aviation Insurance Market report.

One part of aerospace now stands out despite its older reputation as a niche market. Business aviation has started attracting private equity funds, family offices, and growth equity investors seeking stronger risk-adjusted returns.

For much of its history, business aviation sat in a blind spot for institutional finance. Wall Street followed commercial airlines, Airbus, Boeing, and large defense contractors. The private jet sector looked too small, scattered, and relationship-driven for serious institutional capital. That view has changed.

The largest change in business aviation

The largest change in business aviation over the past five years has been the expansion of its addressable market. COVID-19 forced many travelers to use private aviation out of necessity, and many never fully returned to commercial flights.

Once travelers experience the productivity, privacy, scheduling control, and reliability of private travel, their preferences often change for good. That shift has created a larger, more durable customer base for business aviation operators and infrastructure providers.

The data supports the change. Fractional ownership remains the only major category with consistent post-pandemic growth. Traditional charter and whole-aircraft ownership have declined modestly (see Deadliest Aircraft Crashes and Worst Aviation Accident Statistics).

This matters for investors because fractional operators produce recurring revenue, multi-year contracts, and predictable aircraft utilization. Those features give the sector a cleaner financial profile and make valuation work less speculative.

Aerospace and defense M&A deals

Infrastructure attracts steadier capital

Investors that prefer not to pick winning operators have another option: infrastructure-like businesses that earn revenue regardless of which aviation brand gains share. Fixed base operators, MRO providers, avionics shops, parts distributors, and aviation software platforms serve aircraft across ownership structures and usage models.

FBOs are the clearest example. These businesses provide fuel, handling, and aircraft services at airports. An FBO lease at a major hub generates revenue from every landing, refueling, and service interaction, whether the aircraft belongs to NetJets, a Fortune 500 flight department, or a single-owner operator.

Lease terms often run long, switching costs remain high, and regulatory entry barriers protect existing operators. Those features explain why infrastructure investors value the sector.

Signature Aviation and Atlantic Aviation, the two largest U.S. FBO chains, already have backing from major institutional investors, with enterprise values approaching or exceeding $10 bn each.

MRO businesses offer a similar profile with one extra advantage: regulatory demand. Aircraft maintenance is mandatory. Inspections, certifications, engine overhauls, and avionics upgrades follow fixed schedules regardless of economic conditions. That makes MRO revenue predictable and resistant to short-term demand swings.

Business aviation offers investors a cleaner U.S. market exposure than commercial aerospace

The U.S. accounts for about 60% to 65% of global business aviation activity. Most major operators, MRO providers, and FBO networks in the sector are domestic companies.

That structure gives investors less exposure to currency swings, trade disputes, sanctions, and cross-border supply issues that complicate commercial aerospace investing.

During periods of global uncertainty, that domestic tilt makes business aviation more attractive.

Consolidation opportunity remains open

The pandemic-era buying rush has ended. Large operators no longer chase charter companies and fleets at inflated prices with the same intensity. The market now has well-funded fractional and charter brands at the top and a fragmented group of smaller operators below them.

That setup creates room for consolidation. The mid-market B2B charter sector, where operators support large fractional brands, weakened during COVID. Demand for those services has since increased.

A disciplined management team with growth capital has a chance to build a scaled platform and later sell to a major aviation brand or financial sponsor (se How Global Aviation Re/Insurance Market Has Gone Through a Turbulence?).

New fractional entrants are also drawing capital at the premium end of the market. KKR’s 2025 investment in BOND, founded by veterans of earlier fractional aviation ventures, shows investor appetite for experienced operators and repeatable models.

Large fractional providers still serve only part of the potential demand base, leaving room for more scale players focused on ultra-high-net-worth customers.

Public market liquidity is getting closer

Business aviation is moving toward a valuation milestone as larger public-market comparables appear. Standard Aero’s 2024 IPO showed what public investors will pay for an aerospace MRO business with material exposure to business aviation. The company listed at a strong premium, giving private investors a useful reference point.

Pure-play business aviation operators and FBO platforms have not yet listed as standalone public companies. That should change as Signature, Atlantic, Flexjet, and Vista continue to show scale.

Public listings would create clearer valuation benchmarks and draw more institutional attention.

Private equity investors that take positions before public price discovery stand to benefit from valuation re-rating. Sectors often trade at private-market discounts before their first public comparables mature. Once listed companies create transparent multiples, similar private assets often receive higher valuation treatment.

The investment playbook

The strongest entry points remain infrastructure and supply chain assets. FBOs, MRO providers, parts distribution platforms, and aviation-specific software companies offer high revenue visibility and still trade at reasonable valuations compared with cash flow quality.

Operator-level investing requires more selectivity. Investors need fleet discipline, efficient operating certificates, strong management, and a credible growth plan. Scale matters, but badly financed fleet growth destroys value quickly in aviation.

Business aviation has moved from Wall Street curiosity to a real institutional asset class. The sector now offers durable demand growth, recurring revenue models, infrastructure-style economics, strong U.S. exposure, and a coming wave of public-liquidity events.

According to Beinsure analysts, the opportunity sits in the sector’s transition from fragmented private ownership toward institutional capital structures. The window to buy assets at valuation levels tied to the industry’s older cottage-business image is getting smaller.

FAQ

The sector is benefiting from new defense priorities, higher demand for next-generation technologies, stronger investor appetite, and reopened IPO markets. Global aerospace and defense M&A announcements rose 41% to 532 deals in 2025, the highest level recorded.

Business aviation now offers stronger demand visibility, recurring revenue, and infrastructure-style economics. Private equity funds, family offices, and growth investors are targeting the sector because demand expanded after COVID-19 and has remained more durable than many expected.

COVID-19 pushed many travelers into private aviation for safety, flexibility, and reliability reasons. Many of those travelers kept using private aviation because it offered better productivity, privacy, and schedule control than commercial flight.

Fractional ownership creates recurring revenue, multi-year contracts, and more predictable aircraft use. That financial profile makes business aviation easier to value and more attractive to investors than irregular charter demand or full aircraft ownership.

FBOs and MRO providers serve aircraft regardless of ownership model or operator brand. FBOs benefit from airport leases, fueling demand, and high switching costs, while MROs benefit from mandatory maintenance, inspections, certifications, and aircraft upgrade cycles.

The U.S. accounts for about 60% to 65% of global business aviation activity. Because the sector is heavily domestic, investors face less exposure to currency swings, trade tensions, sanctions, and cross-border volatility than in commercial aerospace.

Public listings of large business aviation operators or FBO platforms could create clearer valuation benchmarks. If companies such as Signature, Atlantic, Flexjet, or Vista move toward public markets, similar private assets could receive higher valuation multiples.

…………..

AUTHOR: Nick Fazioli – Jefferies Financial Group, Edited by Nataly Kramer – Lead Insurance Editor at Beinsure