Overview

Like in other economic areas, differences between the Eastern European countries and the rest of Europe are also disappearing in insurance. CEE states have travelled a long way after the fall of the Iron Curtain: they started at a very low point of insurance volume, but insurance penetration has steadily been growing, “Western” insurance practices and legislations have been introduced very fast.

Today the CEE insurance market consists of both subsidiaries of international groups and strong local companies.

Whereas at the beginning there was only motor insurance and industrial insurance in the focus, the population can by now afford better insurance for their property as well as life insurance. Only liability insurance remains behind, as the jurisdiction is still not at the high level of protecting the interests of claimants like in the rest of Europe.

Forcast for CEE Insurance Market

Insurers across the 17 CEE markets under the scope of the XPRUIMM reports ended 1Q2024 with GWP amounting to EUR 11.4 billion, up by 10.20% y-o-y. Paid claims increased at a higher pace of 15.6%, to EUR 6.35 billion.

The change in underwriting behaviour we are currently facing is somehow smoother on the CEE markets, but the general strategy of international groups and business exchange with reinsurance will lead to similar situations like in other highly developed markets.

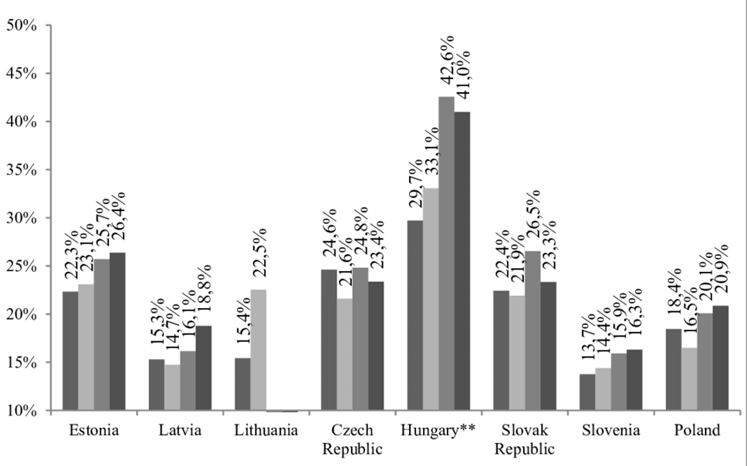

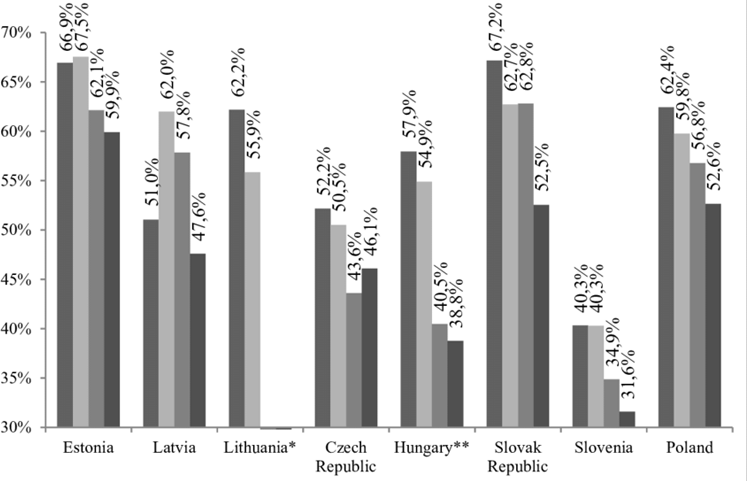

The share of property insurance premiums in total gross written premiums of non-life insurance markets

The best growth rates were recorded in Romania (+45%) and Czechia (+23.2%), among the bigger markets of the region, while other 6 markets recorded double digit growth rates. Slovakia was the only market reporting decreasing GWP, but the negative trends was mostly driven by the local Generali company becoming a branch of an insurance company from another Member State.

The insurance market has gone well through the Covid-19 pandemic, as the peril was excluded from all wordings except travel insurance.

It seems that the market will become interesting for MGAs working with the capacity of German and British insurers. The year was relatively good for the insurance market with the same claims experience like in the previous year.

The Non-life insurance premium of this traditional industrial nation amounted in 2023 to 94.7 bn CZK (3.6 bn EUR) and the Life insurance premium reached 46.5 bn CZK (1.8 bn EUR). This results in a good average insurance penetration of 3.2 %.

Market shares of the insurers working in the country remain stable. After the integration of former state-owned market leader Ceska pojistovna into Generali a short time ago, the market is dominated by the big European insurance groups. Generali will also reach out to integrate their company in neighbouring Slovakia into Generali CZ, thus again creating one market for both countries.

The mandatory MTPL insurance line provided for the largest contribution to the regional premium growth, with GWP increasing at the above average rate of 15%, to EUR 2.55 billon.

By far, the most impressive growth was recorded in Romania, where GWP doubled y-o-y, reaching to EUR 478.7 million, driven mostly by the raising prices following the City Insurance failure. As a result, Romania’s market chare in the region’s MTPL business increased from 10.7% to 18.7%.

In this paper (as the first part of the study) wider attention was given to the changes of products’ structure of non-life markets. It was found that motor third party liability insurance still remains the most relevant insurance line in the non-life markets of the examined countries.

The share of MTPL premiums in total gross written premiums of non-life insurance markets

Motor Hull GWP reached EUR 1.6 billion, almost 13% up y-o-y. Property insurance GWP grew by almost 15%, to EUR 1.76 billion, while paid claims went by up by 35%, to EUR 579 million. Life insurance, on the other hand, saw an only 2% increase in premiums, to EUR 3.16 billion.

The negative change in premiums recorded in Poland (-5%) due to legal changes that hampered somewhat life insurance sales was the main factor causing the low growth rate in the regional premiums volume.

Polish insurance market achieved a premium volume of 20.7 bn PZN (4.6 bn EUR) in Life insurance and 40.7 bn PZN (9 bn EUR) in Non-Life. Insurance penetration stands at 3.7 %, thus reflecting the country’s overall picture as one of the well-advanced economies among the Eastern countries.

There is a typical consolidation tendency on the insurance market, as shown by the recent sales between international groups: Nationale Nederlanden bought MetLife, Allianz took over Aviva and Uniqa purchased Axa.

Despite these changes, most European insurance groups are active in Poland, contributing largely to the capacity of the market along with major Polish insurer PZU.

One of the great changes the Polish economy will have to face is the transformation from coal as the country’s most important energy source, to other, “green”, sources.

Although this will take some time, opportunities for innovation of both the technical bases and insurance solutions will positively influence the insurance market.

Still, one of the main concerns of the insurers is to obtain higher market shares, which leads on the one hand to product innovation and product enrichment in life insurance and to a wild price war on the other.

The structure of gross premiums written in non-life insurance market

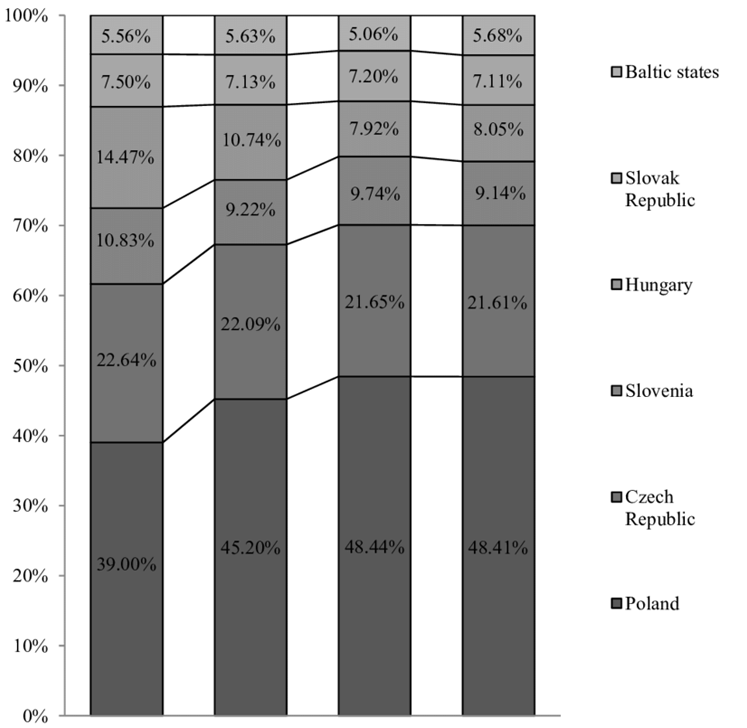

The course of the development of non-life insurance markets in CEE countries differs in many aspects from the Western-European countries. This study shows how these changes performed in the eight CEE countries, that overcame transition in similar time and accessed the European Union.

Key CEE Insurance Market Outlook:

- In 2024 the average gross written premiums (GWP) increased by 12% in the region on a yearly basis. All countries of the region demonstrated a stable growth, but this high increase rate is mostly due to the significant increase in the Polish market.

- The average GWP penetration remained stable at around 2.5% over the last three years in the examined twelve countries. In addition, GWP/capita increased to an average EUR 360.

- Paid claims increased 17% in the CEE region, mainly due to Poland’s large increasing claim volume.

- Non-life insurance experienced higher growth than life insurance at 15.6% compared to 6.5% year over year.

- Both life and non-life insurance markets can be considered competitive. Typically, the markets of each each country are dominated by 3-5 insurance companies, and, as certain major international insurance groups own several insurance companies on the same market, the concentration of the markets might be higher.

- The top 10 leading life insurance groups in the CEE region cover around 67.8% of the total life gross written premiums. A typical top 10 group is present in 4-5 CEE countries in the life insurance sector owning EUR 879m GWP in total. In the case of the non-life business line, the top 10 leading insurance groups cover around 67.8% of the total non-life gross written premiums. They are typically present in 5-6 countries and have an average gross written premium of EUR 1,516m.

- The most active buyers in the region were Vienna Insurance Group (VIG), with 8 transactions, followed by Fairfax Financial Holdings.

- The most active sellers in the region were AIG with 6 sales, followed by Munich RE (ERGO) with 3 sales.

Leveraging on the success of the 1st release of the CEE insurance, we decided to continue our research, provide intelligence on insurance market trends and present the recent activity in the CEE region.

Although the consolidation has started in some of the markets, most of them are still fragmented in both, life and non-life segments.

There are a relatively high number of insurance companies with less than 5% market share in many countries, which signals a need for further consolidation.

Besides market dynamics, the new regulatory requirements such as Solvency II and the introduction of IFRS 17 are likely to make insurance business more capital extensive thus requiring robust profitability. The market is heavily working towards the implementation of IFRS 17, which is expected to bring substantially enhanced transparency via standardization of financial statements and consequently reducing costs of M&A.