Overview

The crypto fundraising landscape is showing signs of recovery. In the last six months to maybe even a year, we’ve been in the same cycle in terms of sentiment, increasing capital going into the space and more developers coming and building, according to PitchBook’s Report.

The crypto VC landscape mirrors the broader crypto and blockchain space, marked by volatility and rapid innovation. Over the last decade, it has undergone several distinct phases.

After the initial-coin-offering boom in 2017, there was a recalibration where investors became more selective. A new growth cycle began in 2020, fueled by decentralized finance (DeFi) and increasing institutional interest. This led to record-breaking fundraising levels in 2021 and 2022, as the crypto ecosystem matured, especially in infrastructure development.

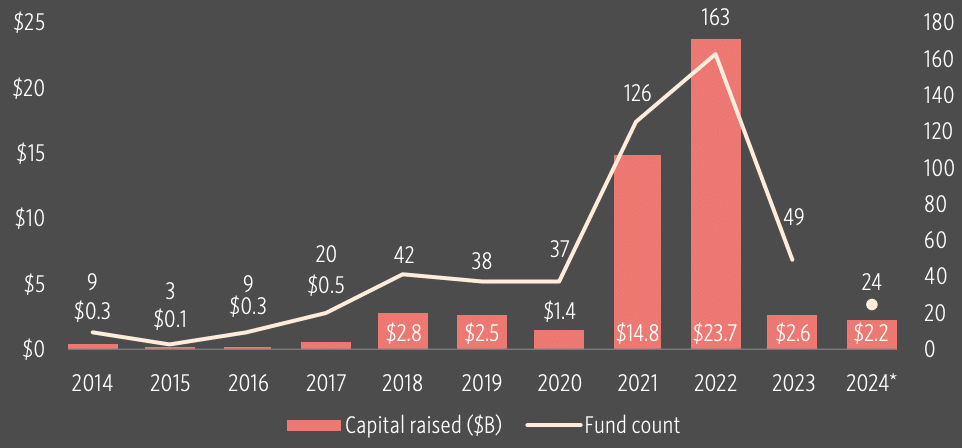

The crypto VC landscape has seen major fluctuations in recent years. In 2022, fundraising hit a record high at $23.7 bn, nearly doubling 2021’s total. But in 2023, it plunged by 88.9%, dropping to $2.6 bn.

Despite the downturn, the median fund size grew by 65.1% in 2024, reaching $41.3 mn. Midsized funds, ranging between $100 mn and $500 mn, have become more prominent, offering the flexibility needed to navigate current market challenges without the burdens of managing megafunds.

A key factors crypto market decline

In 2024, however, the crypto market entered a bear phase, leading to a sharp drop in fundraising. Several key factors contributed to this decline. Macroeconomic pressures, such as inflation and rising interest rates, slowed the flow of capital into riskier assets like crypto.

At the same time, regulatory scrutiny increased, influencing fund managers’ strategies and making LPs more cautious. These factors have led to greater emphasis on portfolio diversification, favorable jurisdictions, risk management, and thorough due diligence.

Despite these challenges, some areas within crypto continue to attract attention, including blockchain infrastructure, trading platforms, and physical resource protocols like DePIN.

These sectors are seen as holding the most potential for growth, signaling where investors are still placing their bets.

PitchBook remains optimistic about the upcoming months, predicting that more token launches will soon be announced.

PitchBook’s Robert Le noted that there are already plans for the third and fourth quarters of this year, but the market is currently in a “prisoner’s dilemma” as projects wait to see how the market will move, aiming to time their launches.

While everyone prefers a rising market, some may decide to launch their tokens regardless of the ideal conditions, potentially creating a “tipping point” or a full-blown bull market.

Token launches have dried up

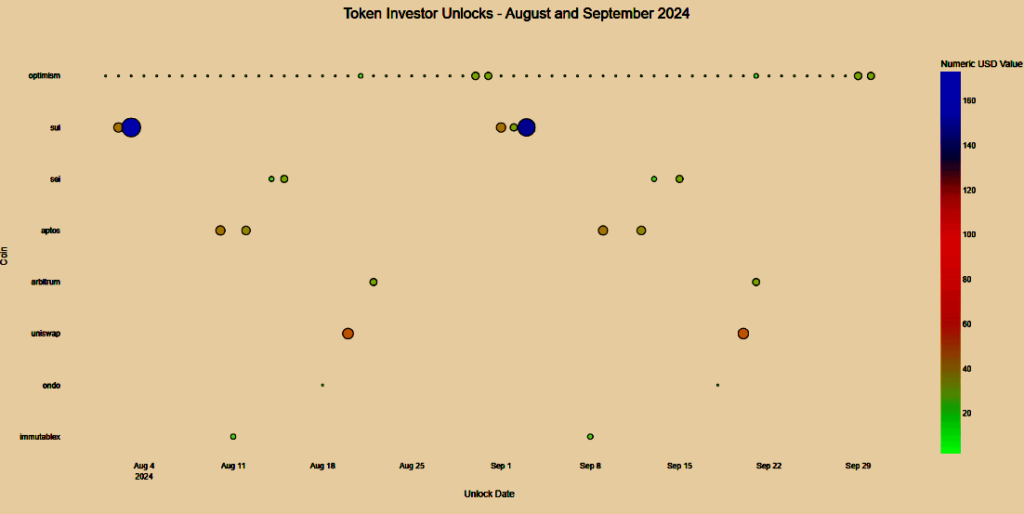

Even token unlocks have been sparse, with the $350 mn SUI unlock in September being one of the more significant events recently, according to DeFi Fundraising Review.

However, the market could experience a bull run sometime in 2025, regardless of the U.S. presidential election outcome.

PitchBook doesn’t expect the election to have a substantial impact on crypto, stating that the industry is often viewed skeptically by governments due to its challenge to the traditional financial system.

Token investor unlocks

Crypto will need to work with both political sides moving forward, regardless of party affiliation.

Crypto-native VC funds, run by individuals with deep industry knowledge and long-term belief in blockchain technology, have played a key role in supporting the sector’s most promising startups.

These funds, unlike traditional VCs that may only partially engage with crypto, often have a clear investment thesis and a thorough understanding of blockchain’s technological foundations. Their networks span both decentralized and traditional finance, making them uniquely positioned to navigate and support growth in the crypto ecosystem.

Crypto fundraising and venture capital activity

Emerging managers continue to lead the crypto VC space, capitalizing on their specialized expertise in areas like “tokenomics” and governance. However, first-time funds have dropped from 58% in 2020 to 45.8% in 2024, indicating a more cautious approach to market entry. A “barbell effect” is expected to emerge, with both first-time and established crypto-native managers likely to succeed in raising capital.

Fundraising timelines have extended, reflecting growing caution among investors. Both the time between raises and the duration to close funds have lengthened, suggesting a challenging future for fundraising.

LPs are becoming more selective and risk-averse due to recent market downturns.

The fundraising environment will remain difficult as the market continues to recover. Some fund managers may need to liquidate token holdings at lower values. Without substantial returns to LPs, seasoned crypto investors are expected to maintain a cautious stance, while newer LPs may be drawn to trending sectors like restaking or the intersection of crypto and AI.

Reflecting on venture capital activity, while it hasn’t returned to the peak levels of 2022, the landscape is looking better compared to last year. As of July 30, 2024, $2.2 bn has been raised across 24 funds, putting it on track to surpass 2023’s total.

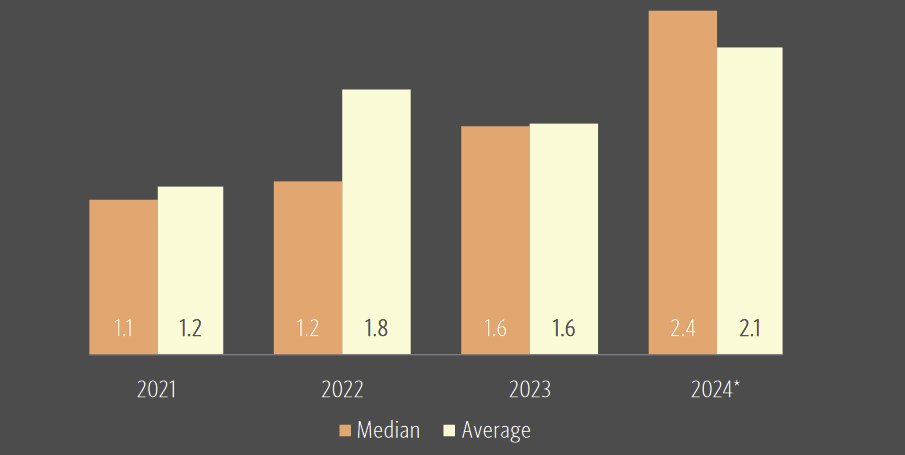

Median and average time between crypto VC funds

From 2021 to 2024, the time between fundraises has steadily increased, with the median time between funds more than doubling from 1.1 years to 2.4 years. This lengthening period suggests that fund managers are taking longer to return to market, likely due to spending more time with their portfolios and deploying capital much slower during the crypto bear market.

Signs of recovery in crypto fundraising

We note that the crypto industry has historically followed a four-year cycle, often tied to Bitcoin’s halving events, which have had significant market impacts.

Fundraising trends have mirrored these cycles, with peaks observed in 2014, 2018, and 2022. If these historical trends continue, we anticipate another fundraising peak in 2026, aligning with the next expected major cycle in the crypto market.

One of the primary factors was the lack of liquidity events, particularly the slowdown in token launches in the second half of 2022 and much of 2023. Without these exits, fund managers were not able to produce DPI for LPs, which led investors to be less motivated to commit fresh capital to crypto-native VC funds.

Another factor contributing to the sharp decline in crypto VC fundraising in 2023 was the significant devaluation of tokens distributed during the 2021-2022 token-launch boom.

Many fund managers who received these tokens as part of their investments during this period chose to hold on to them, either due to lockup periods or because they believed the tokens were undervalued and would appreciate over time.

However, as the broader crypto market experienced a severe sell-off in 2022, the mark-to-market value of these holdings declined precipitously.

This sharp reduction in the value of their portfolios likely affected the overall performance metrics of these funds, making it more challenging for fund managers to raise new capital for follow-on funds.

Crypto venture capital fundraising activity

LPs observing these diminished returns and increased volatility became more cautious, leading to a more conservative approach to committing new capital in 2023.

The recovery of the broader crypto market is partially responsible for this rebound, with the total market cap reaching 93% of its previous cycle’s peak by March 2024.

August alone saw 167 raises totaling $981 mn, with DeFi projects leading the way with $210 mn. There has also been a noticeable uptick in gaming and metaverse-related projects, which raised $65 mn last month.

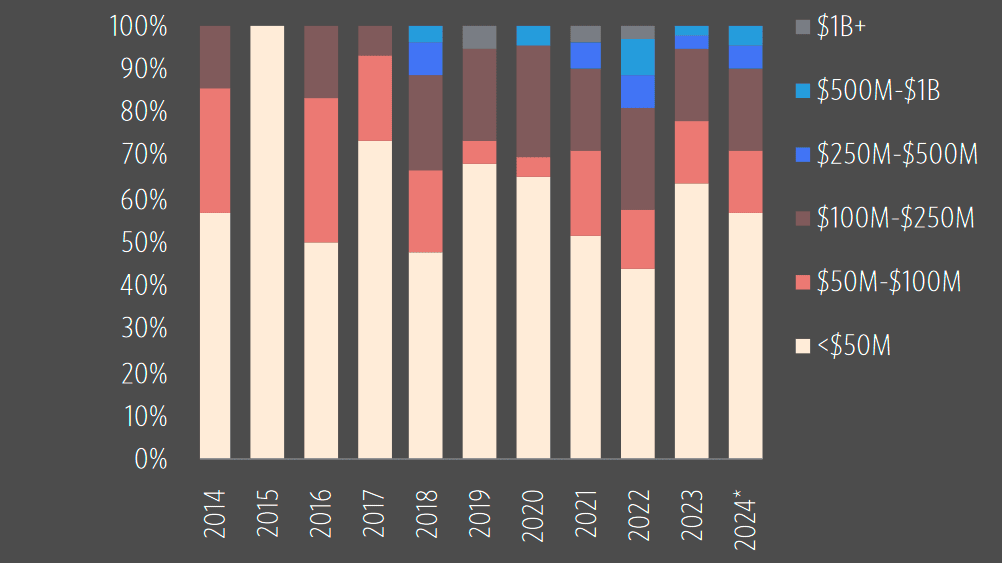

Share of crypto VC fund count by size bucket

The median fund size has risen significantly, jumping 76% from $25 mn to $41 mn in just a year. Many of these are midsized funds, ranging from $100 mn to $500 mn.

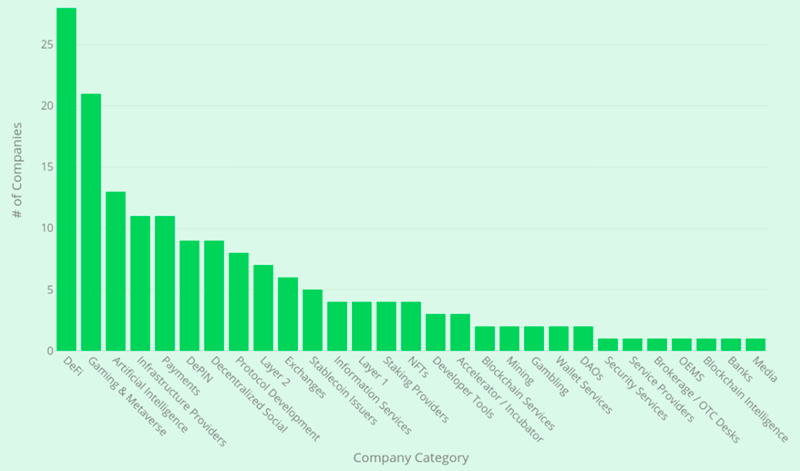

Number of fundraises by category

This fund size strikes a good balance for investors—large enough to support the growth of the industry but not so large that they struggle to find viable investment opportunities.

Larger funds, especially those over $1 bn, may have difficulty in writing checks between $25 mn and $50 mn, as startups at that scale remain rare in the crypto space.

While the market is rebounding, the fundraising environment will remain tough as the market recovers. However, staying below the venture capital frenzy of 2022 could ultimately benefit the industry, allowing it to grow more sustainably without being driven by hype.

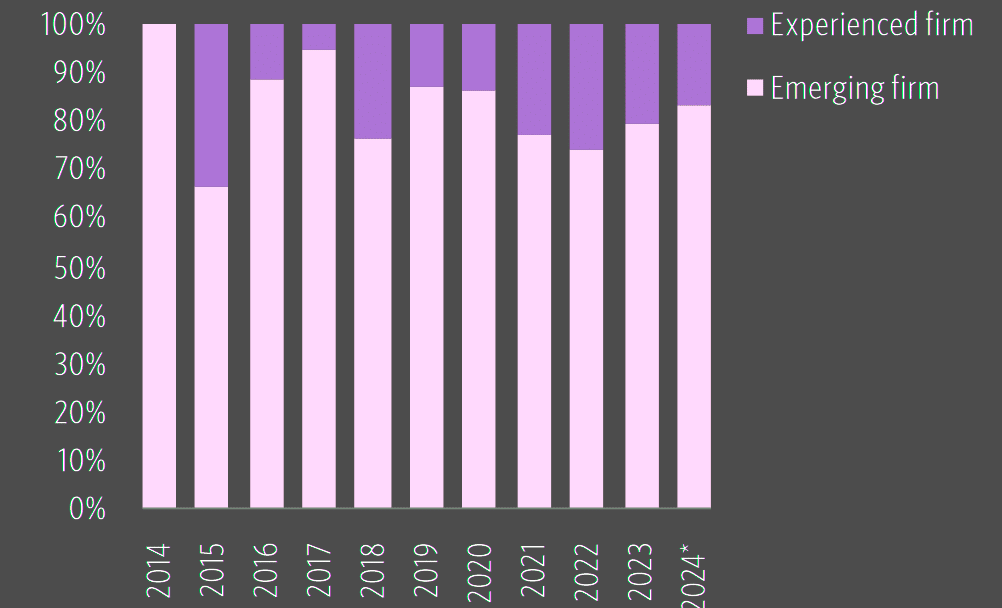

First-time funds are poised for a rebound

Emerging managers continue to dominate the crypto VC space, accounting for 77% to 87% of funds raised annually over the past five years. These managers often possess deep, specialized expertise in areas like tokenomics, governance, and liquidity provisioning, skills that are now essential in crypto investing.

Many crypto-native firms are relatively new, with most managing fewer than four funds.

Generalist VCs, which traditionally launched new crypto funds, are playing a more passive role, choosing to invest through existing vehicles rather than starting new funds. However, established players like Andreessen Horowitz and Bain Capital have dedicated crypto investment teams.

Share of crypto VC fund count by manager experience

Despite the decrease in first-time funds from 58% in 2020 to 45.8% in 2024, a market recovery could boost the number of first-time funds in the coming years, signaling a potential rebound for new entrants. Emerging managers are expected to maintain their edge in this space, while generalist firms may take a backseat.

We will likely see a “barbell effect” taking shape, with the lowest and highest ends of the spectrum—first-time managers and established crypto-native fund managers—experiencing the most success in raising capital, as they are well-positioned to meet the unique demands of crypto startups.

As the top-quartile emerging managers become experienced firms, expect the number of funds raised to shift to established managers. Meanwhile, new entrants with deep crypto expertise will continue to enter the VC space.

FAQ

The crypto fundraising landscape is showing signs of recovery. After a sharp decline in 2023 due to a bear market, inflation, and regulatory scrutiny, 2024 has seen renewed interest, especially in blockchain infrastructure, DeFi, and gaming projects. In August 2024 alone, 167 raises were recorded, totaling $981 mn, showing a positive trend in crypto VC fundraising.

The decline in 2024 was due to multiple factors: economic pressures such as rising interest rates, regulatory challenges, and decreased liquidity events in the crypto space. This caused many investors to become cautious, resulting in an 88.9% drop in fundraising. Additionally, the value of tokens held from previous investments declined, affecting overall returns for fund managers.

Yes, despite challenges, there is strong interest in areas like blockchain infrastructure, DeFi platforms, and physical resource protocols (e.g., DePIN). These sectors show potential for growth, and VCs are focused on projects that bring long-term value to the ecosystem.

Median fund sizes have grown, reaching $41.3 mn in 2024—a 65.1% increase from previous years. Midsized funds between $100 mn and $500 mn are becoming popular as they provide flexibility in the current market. However, first-time funds have decreased, signaling a cautious approach from new entrants.

Crypto-native VCs are crucial, as they bring deep knowledge of blockchain and tokenomics, often supporting the most innovative startups. Unlike traditional VCs, crypto-native funds typically have clear investment theses rooted in blockchain fundamentals, making them well-equipped to guide emerging crypto companies.

Token launches have slowed, with only a few significant events like the $350 mn SUI unlock in September 2024. However, PitchBook predicts more token launches in late 2024, potentially leading to a market tipping point. If this occurs, it could trigger a bull market in crypto, helping to boost liquidity and fundraising.

There is potential for a rebound in first-time funds, as the market recovers and investor confidence improves. While first-time funds dropped from 58% in 2020 to 45.8% in 2024, emerging managers with specialized expertise continue to dominate the space. This “barbell effect” suggests both new and established managers may succeed in raising capital as the industry grows.

………………..

AUTHOR: Robert Le – Senior Analyst, Emerging Technology PitchBook. Reviewed by Peter Sonner