Overview

Moody’s shifted Germany’s property and casualty insurance market outlook to stable, ending the negative view it carried before. Beinsure analyzed Moody’s and AM Best’s reports and highlighted key trends.

The agency ties this move to stronger underwriting margins, steadier market dynamics, and pricing that’s finally catching up with loss trends.

Premium hikes tell most of the story. Motor insurance, hammered by claims inflation between 2022 and 2024, had seen years of underwriting losses.

5 Key Highlights

- Moody’s revised Germany’s P&C insurance sector from negative to stable, driven by stronger underwriting margins, balanced market conditions, and premium hikes.

- Motor insurance premiums rose ~30% since 2022, homeowners’ insurance ~40%, restoring profitability but raising affordability risks for consumers by 2026.

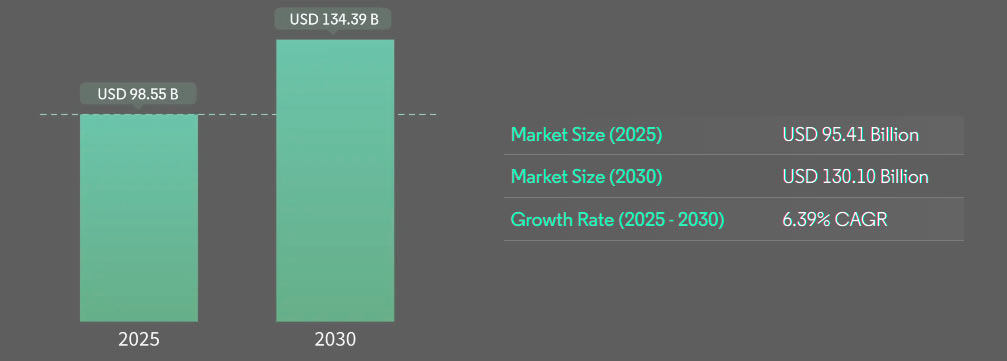

- Germany’s P&C insurance market is projected to grow from $95.4 bn in 2024 to $130 bn by 2030, a CAGR of 6.4%, with specialty lines like cyber and environmental liability gaining traction.

- Life insurers hold robust Solvency II ratios (188-522%), while non-life insurers are expected to improve their combined ratio to 94% by 2026, backed by premium growth and reinvestment returns.

- Rising NatCat losses, high reinsurance costs, inflation-driven claims pressure, and structural economic issues (labor shortages, energy costs, sluggish productivity) remain key challenges.

The life insurance sector gets a stable call too, though for different reasons. Longer-term yields help life insurers keep guarantees on savings products.

Insurance Premiums and Price Outlook

The property and casualty insurance market in Germany is among the largest and most mature in Europe, with a significant number of domestic and international players operating in the market.

In terms of product offerings, German insurers provide various P&C insurance products to individuals, businesses, and other organizations. This includes coverage for property damage, liability, motor vehicles, and other risks.

The Germany P&C Insurance Market size in terms of gross written premiums value is expected to grow from $95.4 bn in 2024 to $130 bn by 2030, at a CAGR of 6.4% during the forecast period (2025-2030).

In addition, specialty insurance products that are specific to particular sectors and risks, e.g., cyber or environmental liability protection, are becoming increasingly popular, Beinsure noted.

Germany P&C Insurance Market size forcast

Since 2022, average motor insurance premiums climbed around 30%, pulling the segment back toward profitability.

Homeowners’ insurance moved even harder – premiums there jumped about 40% in the same window, lifting results after long strain.

Germany P&C Insurance Market Trends & Insights

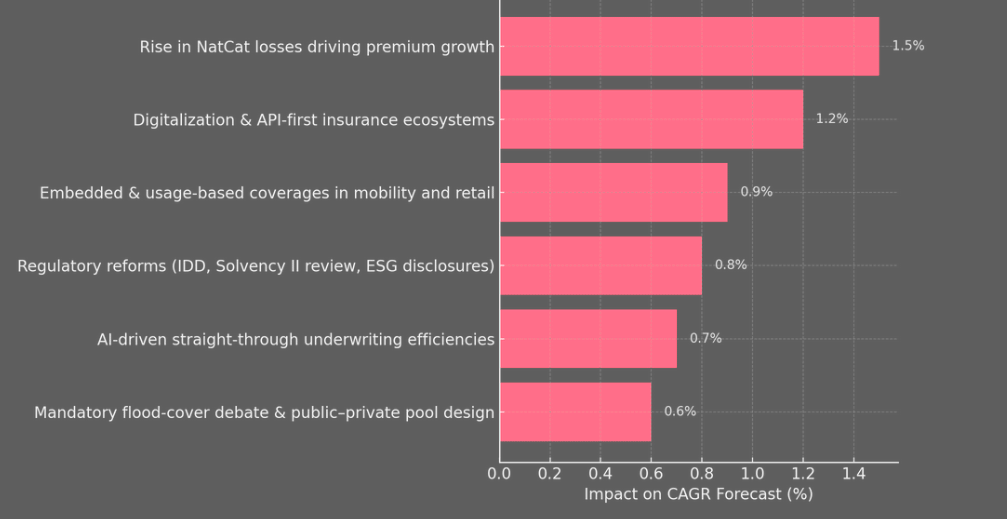

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

| Rise in NatCat losses driving premium growth | +1.5% | National, concentrated in Bavaria, Baden-Württemberg | Short term (≤ 2 years) |

| Digitalization & API-first insurance ecosystems | +1.2% | National, with early gains in Munich, Hamburg, Berlin | Medium term (2-4 years) |

| Embedded & usage-based coverages in mobility and retail | +0.9% | National, with urban concentration | Medium term (2-4 years) |

| Regulatory reforms (IDD, Solvency II review, ESG disclosures) | +0.8% | National, aligned with EU framework | Long term (≥ 4 years) |

| AI-driven straight-through underwriting efficiencies | +0.7% | National, led by major insurers | Medium term (2-4 years) |

| Mandatory flood-cover debate & public–private pool design | +0.6% | National, priority in flood-prone regions | Long term (≥ 4 years) |

Moody’s says the combined ratio should drift toward the mid-90s, back in line with the long-term average. Insurers still have to rebuild claims reserves and equalisation buffers after extended pressure.

Yet 2025 has so far avoided major natural catastrophe losses, no repeat of storm and flood-heavy years, and that’s easing the weight on ratios.

There’s the affordability issue, though. Price hikes restore earnings but also stretch household budgets. Premium growth could stall in 2026 if consumers push back, analysts says. That tension stays on the table.

Forecast CAGR Impact Drivers for German Insurance Market

German life insurers maintained very strong Solvency II ratios in 2024, driven by market rates exceeding guaranteed rates in the legacy books. Total premium growth was above expectations. Life insurers have Solvency II ratios ranging from 188% to 522% at 2025, Beinsure noted.

German non-life insurers are expected to see a net combined ratio improvement to 94% by 2026, driven by strong premium growth of 6% in 2025 and 4% in 2026, alongside higher reinvestment rates boosting investment returns to 2.9% in 2026.

AM Best predicts the segment will report an average net combined ratio close to breakeven at year-end 2024.

That result might marginally improve in 2025 as more rate discipline feeds through in response to continued claims inflation and a larger number of weather-related larger losses during 2024.

Claims expenses are expected to remain magnified by high inflation pressures on the costs of repair and spare parts, with those pressures only expected to ease gradually during the second half of 2025 or early 2026, Beinsure noted.

Although inflation has started to decrease steadily during 2024, claims inflation trends have remained sticky during the second half of 2025.

This is partly because the development of claims inflation trends tends to lag changes in consumer price index.

Insurers raised premium rates during the main motor policy renewal round in January 2025 in response to the drop in technical results, however, most failed to fully reflect the intensity of claims inflation in the prior year.

Germany 2025 macro outlook: weak growth, big fund bets on infrastructure

On the investment side, the setup looks steadier. Long-term bond yields remain stable, which keeps portfolio returns healthy.

The macro view isn’t spectacular but manageable – GDP expected at 0.3% in 2025 and 1.4% in 2026, following a 0.5% drop in 2024, according to Moody`s.

Inflation should slip to 2.3% in 2025 and 2.1% in 2026. No further European Central Bank cuts expected, a stance that supports investment income and capital adequacy.

Germany’s economy is expected to experience only minor growth 0.2% in 2025, but a rebound is anticipated in 2026 (from 1.1% to 1.8%) driven by increased government infrastructure and defense spending.

Key challenges remain, including sluggish productivity growth, labor shortages due to an aging population, and high energy costs.

Investment is currently hindered by financing conditions and uncertainty, but a new $500 bn investment fund aims to address structural issues by focusing on infrastructure, climate protection, and digitalization.

Macroeconomic outlook

Growth prospects stay muted. Forecasts peg GDP at just 0.2% in 2025, with recovery penciled in for 2026, somewhere between 1.1% and 1.8%. Private consumption looks set to carry the expansion in 2025, lifted by stronger purchasing power.

Private investment, on the other hand, appears stuck. Tighter financing conditions and lingering uncertainty keep corporate spending weak through the year. Inflation holds above 2% in the near term before easing later.

Germany’s structural headwinds remain unresolved – sluggish productivity, an aging workforce driving labor shortages, and elevated energy costs all continue to weigh.

Producer prices in January rose 0.5% year-on-year but slipped 0.1% month-on-month. Import prices climbed 1.1%. These data points underline the uneven path forward.

Investment view

Policy turns more ambitious. Berlin approved a $500 bn special fund to channel capital into infrastructure, renewable energy, climate protection, and digitalization. Execution is the tricky part. The government wants faster planning and permitting, cutting red tape to get projects moving.

Risks linger. Trade disputes could flare, while deep structural bottlenecks might blunt the long-term effect of fiscal stimulus. Without reforms, spending alone risks being a short-lived push.

Still, opportunities exist. Infrastructure and renewables stand out as clear winners, with digitalization also likely to attract capital flows. For investors, those sectors align with both political backing and market demand.

Moderate Growth Prospects on an Inflation-Adjusted Basis

AM Best expects the German non-life segment to experience premium growth on a nominal basis over the next 12 months, although premium levels will likely be static or show marginal growth only on a real basis.

- Premium growth levels are reflecting inflation-driven rate adjustments but remain subdued by weak economic growth and an increasingly competitive environment.

- Premium growth in Germany’s non-life insurance segment has historically been correlated with the state of the economy.

Germany’s economy is expected to continue to show a path of sluggish recovery in 2025, in the face of continued headwinds, such as the recent collapse of the German coalition government and high industrial energy costs.

The latest economic trajectory is likely to lead to a modest but underwhelming economic recovery over the next 12 month, underpinned by the IMF’s current GDP growth forecast for 2025 of

0.8%.

All major non-life insurance business lines achieved premium growth in the first six months of 2024, benefiting largely from robust inflation-adjusted price momentum.

AM Best assumes that the need to continue to enforce strong price increases to offset claims inflation and reinsurance costs, as well as the impact of inflation on insured values, will lead to higher premium levels, either through repricing or automatic rate adjustments.

Insurance alternative asset holdings

Germany’s BaFin confirmed reports it is approaching 30 to 40 insurance companies with significant alternative asset holdings. This focus stems from the complexity of these investments.

At some insurers, private debt makes up over 30% of their portfolios, while alternative investments reach up to 70%.

Norbert Pieper, a BaFin spokesperson, emphasized the need to monitor these high exposures. He noted that managing complex assets requires solid risk management, adequate staffing, and specialized knowledge.

This oversight forms part of BaFin’s 2025 supervisory agenda. The regulator’s 2025 risk report highlights a 2024 investigation into insurers’ investment strategies.

Digitalization, insurance tech upgrades and regulatory compliance

Growth, however, remains concentrated in single-premium contracts, not in ongoing premium inflows.

Analysts at Moody’s don’t sugarcoat the industry’s long-term squeeze. Heavy spending on tech upgrades and regulatory compliance remains unavoidable.

Smaller and mid-tier insurers are getting absorbed into stronger groups, and that trend probably won’t slow.

The shift to digitalization is a further notable trend in Germany’s insurance market. Insurtech and digital insurance platforms are increasingly gaining attention, challenging the established players.

The increased focus on sustainability and climate risk is another significant development in the market.

With the growing awareness of climate-related risks, insurers are offering climate-friendly products and integrating climate risk management into their underwriting processes.

Moreover, digitalization is revolutionizing the underwriting process. Insurers are harnessing advanced machine learning algorithms, artificial intelligence, and data analytics to more precisely identify threats and efficiently.

This enables insurers to personalize premiums based on individual risk profiles, leading to more tailored and competitive insurance offerings for customers. Additionally, digitalization is enabling insurers to develop innovative insurance products and services.

For example, usage-based insurance (UBI) policies utilize telematics devices to track driving behavior, allowing insurers to offer personalized premiums based on actual usage and driving habits.

Insurers are leveraging big data analytics and predictive modeling to identify emerging risks, assess potential losses, and develop proactive risk mitigation strategies.

Pricing pressure and natural catastrophe risk

So yes, risks linger. Pricing pressure, natural catastrophe risk, and limited premium growth keep the landscape complicated. But the trajectory of profitability, plus the steadier capital base, fits a stable outlook.

Moody’s RMS estimates that insured losses in Germany from the Central Europe Floods will likely range from €2 bn to €3 bn. Southern Germany experienced intense rain, resulting in widespread flash and river flooding.

Initial flooding affected smaller rivers in Baden-Württemberg and Bavaria. The Danube River also reached flood stage as water accumulated downstream.

Moody’s latest loss estimate includes insured property damage, spoiled contents, and business interruption across residential, commercial, industrial, agricultural, and automobile sectors.

According to AM Best report, the German property insurance market is subject to volatility in its results due to its exposure to potentially large weather losses that can significantly add to the segment’s claims burden.

Natural catastrophe events have caused earnings volatility in the past as the product risk in the property segment is dominated by severe weather events.

However, the impact of natural catastrophe events on the market’s capitalisation has proven to be low historically.

That said, the recent and severe occurrences of flood events in Germany have sparked a renewed discussion about the introduction of a state-backed system to provide comprehensive natural hazard insurance protection.

These events have brought to light a significant insurance gap among households exposed to specific natural hazards, including flooding.

AM Best believes that most German non-life insurers are well-positioned to manage the financial impact of weather-related catastrophes, as most carriers benefit from adequate access to reinsurance capacity and comprehensive aggregate reinsurance covers.

However, the cost of reinsuring natural catastrophe events has risen sharply because of general hardening conditions in the reinsurance market.

As a result, insurance companies ended up buying reinsurance at higher attachment points, which is likely to result in greater earnings volatility.

FAQ

Moody’s shifted its outlook after stronger underwriting margins and steadier market dynamics began to emerge. Higher premiums across motor and homeowners’ insurance helped restore profitability, while a relatively quiet 2025 natural catastrophe season reduced claims pressure.

Since 2022, motor premiums increased by roughly 30% and homeowners’ insurance premiums by about 40%. These hikes improved underwriting results but raised affordability concerns, with analysts warning that premium growth could slow in 2026 if consumers resist further increases

The market is expected to grow from $95.4bn in gross written premiums in 2024 to $130bn by 2030, representing a CAGR of 6.4% over 2025–2030. Specialty products like cyber and environmental liability insurance are contributing to this expansion

Key drivers include rising NatCat losses (+1.5% CAGR impact), digitalization and API-first ecosystems (+1.2%), embedded and usage-based insurance (+0.9%), regulatory reforms (+0.8%), AI-driven underwriting efficiencies (+0.7%), and the ongoing debate over mandatory flood coverage (+0.6%).

Life insurers benefit from strong solvency ratios ranging from 188% to 522% in 2025, supported by higher yields. Growth is concentrated in single-premium products rather than recurring premiums. Non-life insurers are on track for a combined ratio improvement to 94% by 2026, driven by premium growth and stronger reinvestment returns.

Germany’s GDP is forecast to expand only 0.2% in 2025, with a rebound of 1.1%–1.8% in 2026. Inflation should ease to 2.3% in 2025 and 2.1% in 2026. Structural challenges like labor shortages, high energy costs, and low productivity continue to weigh, but a $500bn government fund for infrastructure, climate, and digitalization aims to boost investment.

Flood events in Bavaria and Baden-Württemberg highlighted the insurance gap for households at risk. Moody’s RMS estimates insured losses from the Central Europe Floods at €2–3bn. While reinsurers provide strong protection, rising reinsurance costs and higher attachment points are increasing volatility for German insurers.

AUTHORS: Yana Keller — Lead Insurance Editor of Beinsure Media, Nataly Kramer — Lead Editor of Beinsure Media