Overview

- Macro Trends Outlook – Current Global Focus Areas

- Identifying and tracking macro trends

- Big Tech: A Dependency Risk

- Democratizing Financial Information Through Social Media

- Beyond Broken Infrastructure: The Cascading Effects of Natural Catastrophes

- Cyber-Enabled Fraud: A New Era for Organized Crime

- AI: Unintended Insurance Impacts and Lessons from “Silent Cyber”

The world undergoes constant change and this gives rise to emerging risks. These are new and changing risks that are difficult to quantify, yet can have significant impact on the insurance industry. Swiss Re identifies emerging risks by gathering signals and feedback from underwriters, client managers, risk experts and others across the Group, and also from external specialists and research institutions.

This year’s SONAR report features 13 emerging risk themes and three trend spotlights. The emerging risk themes are what could be new or changing risks, with both up- and downside potential for insurers.

The “trend spotlight” items highlight contextual developments we deem relevant for the industry, without necessarily profiling a specific risk.

The emerging risk themes outlined in the SONAR report are based on early signals collected over the course of a year. They do not reflect industry-wide thinking with respect to emerging risks, nor do they necessarily cover the full list of associated topics currently on Swiss Re’s radar screen.

Macro Trends Outlook – Current Global Focus Areas

Political and Economic Environment

Global macro trends remain in a “high-alert” state. Geopolitical instability, highlighted by ongoing wars, has shifted government spending priorities.

Military budgets are rising worldwide, diverting funds from other crucial areas like civil infrastructure. This political instability and gaps in infrastructure funding increase the risk of supply chain disruptions.

Inflation persists, varying across regions, and its trajectory depends heavily on central bank policies and domestic economic growth.

Elections in 2024 will shape global politics. While the U.S. presidential election takes center stage, votes in India, the European Union, and other regions will also influence geopolitical alliances, international conflicts, and collaboration on critical issues like climate change and the transition to a low-carbon economy.

Demographic and Social Environment

Inflation continues to strain households, businesses, and governments. Healthcare systems face rising costs and workforce shortages, exacerbated by an exodus of healthcare professionals seeking better opportunities.

As populations age, demand for healthcare services outpaces supply, leading to affordability challenges and growing social inequalities.

Addressing these disparities could improve health outcomes across different demographics. Social isolation and loneliness, both rising issues, negatively impact physical and mental health.

Aging populations in developed markets exacerbate skill shortages, further stressing the balance between productive and dependent demographics. Migration offers a potential solution, but immigration remains a sensitive and divisive issue, sometimes triggering social unrest.

Technological and Natural Environment

Climate risks pose a significant threat to societies. Record-high temperatures in 2023 illustrate the growing frequency and severity of natural hazards, leading to increased economic losses in certain regions. Climate change also threatens food and water security, potentially destabilizing societies and international relations.

The shift to a low-carbon economy remains a global priority. Wind, solar, and new nuclear technologies are advancing rapidly.

However, the energy transition introduces new risks, including heightened competition for critical minerals and environmental threats from activities like deep-sea mining. Additionally, managing the end-of-life stages of green technologies and recycling presents ongoing challenges.

The growing density of green energy infrastructure increases competition for space, raising the risk of service interruptions. Furthermore, technology dependence heightens macro-trend risks, including cyber threats. Digital innovation expands both opportunities and exposures, while social media impacts decision-making and financial market stability.

Competitive and Business Environment

Digitalization continues to transform the insurance industry. Artificial intelligence brings both opportunities and challenges, impacting risk categories such as cyber and fraud.

The rapid pace of AI development adds complexity to compliance and regulation.

Insurers face evolving demands from stakeholders, alongside increased pressure to meet Environmental, Social, and Governance (ESG) standards. Transparency and fairness in insurance practices are under growing scrutiny.

Identifying and tracking macro trends

Identifying and tracking macro trends sharpens our understanding of future risks. Swiss Re maintains a portfolio of macro trends that we expect to significantly impact the insurance industry over the next decade.

Since 2015, we have shared this information publicly through SONAR. The current portfolio consists of 27 macro trends, unchanged from the 2023 version, which was reviewed and updated last year.

Below is an overview of these trends, followed by insights into key global issues and emerging risks linked to this year’s SONAR topics.

| Competitive and Business Environment | Disaggregation of the re/insurance value chain Regional champions expanding globally Increasing digital customer interactions A more litigious environment Growing importance of ESG |

| Demographic and Social Environment | Shifting demographics and global aging Expanding middle class in high-growth markets Longevity and medical innovations Mass migration and urbanization Changing workplace dynamics and talent shortages Widening social inequality and unrest |

| Political and Economic Environment | Macroeconomic instability Challenges to globalization Geopolitical and economic volatility Rising interest rates and the threat of sustained inflation Growing infrastructure funding needs |

| Technological and Natural Environment | Transitioning to a low-carbon economy Expanding digital and cyber risks Treating data as a valuable asset Impact of generative AI Growth of digital products Autonomous transportation and robotics |

Climate Change: An Evolving Threat to International Security

While not a direct cause of civil unrest, terrorism, or conflict, climate change acts as a destabilizing force. The impacts are varied and far-reaching. One critical consequence is the exacerbation of global food insecurity, driven by shifting weather patterns.

250 mn people across 58 countries faced acute food insecurity, with 35 mn on the brink of starvation due to conflicts and severe weather.

Additionally, the world faces a fresh water crisis, with experts predicting a 40% gap between supply and demand by 2030, driven by climate change, resource misuse, and pollution.

Climate change also reduces agricultural output, threatening rural livelihoods and triggering mass migration. The UN estimates that by 2050, 216 mn people across six regions may be displaced within their countries due to climate change.

70% of the most climate-vulnerable nations are also the most socially and economically fragile. Increasingly severe weather, irregular precipitation, and rising temperatures worsen these vulnerabilities.

Potential Business Impacts

- Insurance Demand Shifts: Climate change and geopolitical uncertainties may alter insurance demand. Interest in climate peril coverage will likely rise, along with political risk insurance. Increased civil unrest could drive demand for strike, riot, and civil commotion insurance, though insurability might become challenging.

- Operational Challenges: Climate change could disrupt supply chains, posing significant operational risks for businesses.

- Economic and Strategic Shifts: Domestic and international conflicts could hinder economic growth, reducing overall demand for insurance. War may stress insurers’ liability and asset portfolios, raising capital costs.

- Arctic Expansion: Melting ice in the Arctic will likely boost interest in the region for trade, fishing, mining, and tourism, creating new risk pools and strategic interest.

Beyond the physical risks posed by climate-change induced variations in the patterns of severe weather and other natural peril events, the impacts of warming temperatures are manifold.

They include, for example, the contribution of changing weather patterns in driving global food insecurity to record levels.

Global Supply Chains: Resilience Against Business Interruption Risks Weakening

Post-COVID-19, supply chain security became a priority for management. However, two to three years later, cost reduction has overshadowed this focus.

Decreased investment in supply chain resilience increases vulnerability to shocks, including natural disasters, technology failures, and political events. This heightens the risk of business interruption and related losses.

The pandemic revealed how severely disrupted supply chains can cause long-term consequences. Supply chain resilience is crucial for preventing breakdowns, maintaining delivery value, and ensuring rapid recovery or alternative route mobilization.

Protecting supply chains is vital for companies to preserve market share and profitability, a balance that cost-cutting alone cannot achieve.

Potential Business Impacts

- Rising Loss Ratios: Less resilient supply chains could lead to higher business interruption loss ratios, including contingent and non-damage-related interruptions.

- Increased D&O Risk: Reduced investment in supply chain resilience may expose management to Directors and Officers (D&O Insurance) claims due to potential disruptions, which could be viewed as negligence.

- Healthcare Risks: Disruptions in medical supply deliveries may lead to increased morbidity and mortality rates.

- Broader Economic Impacts: Prolonged disruptions from events like pandemics, civil unrest, blockades of major trade routes, or natural disasters could trigger economic downturns and negatively affect insurance markets.

Political Risks

Beyond major conflicts such as those in Ukraine, Gaza, the Red Sea, and Taiwan, political instability has worsened globally.

The 2023 Fragile State Index shows that fragility has spread to wealthier nations, suggesting that key global supply routes may become increasingly insecure.

Nature-Related Risks

Data shows a rising trend in property insurance purchases to cover natural perils. Increasingly frequent extreme weather events, earthquakes, and volcanic eruptions pose significant risks to production facilities and transport routes, leading to potential disruptions.

Technology Risks

Digitalization enhances supply chain efficiency but also introduces systemic vulnerabilities. These emerging risks demand continuous updates to hardware, software, and protocols, along with well-trained personnel to ensure the security and functionality of systems.

Infrastructure Risks

Supply chains heavily rely on robust infrastructure, including energy, water, power, and health systems. During disasters or pandemics, health infrastructure becomes particularly crucial. However, the G20 reports a significant gap between infrastructure investment needs and actual spending, potentially weakening supply chain resilience.

Economic Risks

Economic factors influence investments in supply chain infrastructure, and in turn, supply chain constraints can impact economic performance. The Federal Reserve Bank of New York’s Global Supply Chain Pressure Index tracks these dynamics, indicating that any disruptions in already stressed supply chains could have serious consequences for businesses.

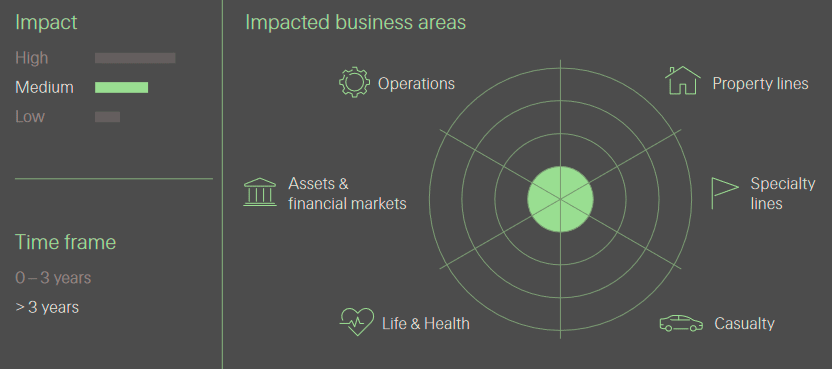

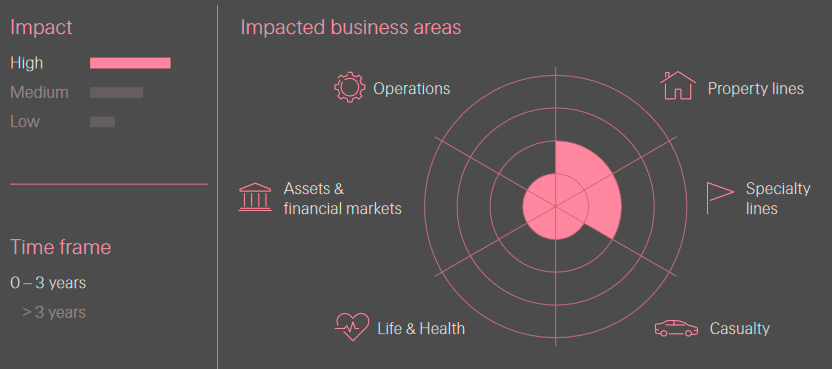

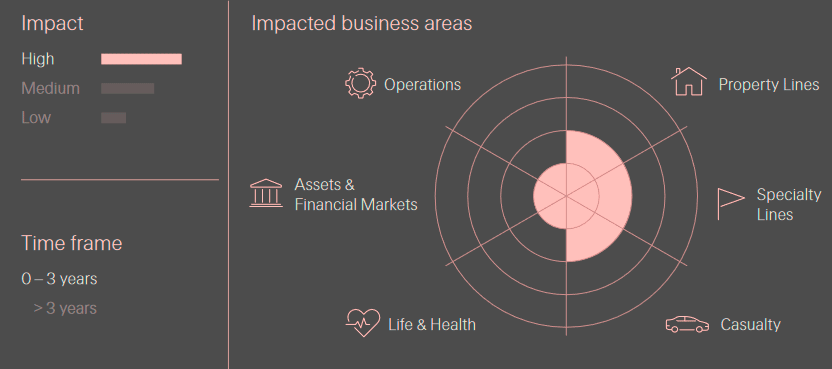

Big Tech: A Dependency Risk

Potential Impacts of Big Tech Dependency

- Service Disruptions: A shutdown or disruption of services from a major Big Tech provider could interrupt the operations of businesses across all sectors. This could trigger various insurance policies. Insurers themselves might also face operational challenges, and financial services could see impacts on their investments.

- Algorithmic Risks: Errors or biases in algorithms provided by Big Tech could result in professional indemnity, product liability, or employment practices liability claims. The draft European Product Liability directive categorizes software as a product, raising potential product liability exposure.

- Data and Privacy Risks: Increased integration of data into open-source AI or social media platforms poses risks of privacy breaches, intellectual property violations, and duty claims. This could elevate exposures in cyber, D&O, and professional indemnity insurance.

- Regulatory Scrutiny: Intensified scrutiny and tougher regulations around Big Tech’s ethical standards and societal influence may lead to an uptick in D&O claims.

- Safety and Liability Concerns: Overreliance on digital platforms can lead to lapses in critical safety functions, increasing the likelihood of accidents. This could affect liability insurance lines, including motor, general liability, professional indemnity, and workers’ compensation. Companies behind these platforms might also face liability for users’ mental and physical harm caused by platform overuse.

With the growing reliance on cloud services provided by a small number of Big Tech companies, the global economy and society are increasingly exposed to dependency risks.

These firms offer a wide range of services, including search engines, browsers, smartphones, social media, e-commerce, software, hardware, operating systems, cloud services, and generative AI. These services are becoming more interconnected, amplifying the risk.

While major cloud service providers have built multiple layers of redundancy by geographically and physically separating infrastructure centers, the threat of a prolonged shutdown due to human error, natural disasters, or cyberattacks remains significant. Such an event could disrupt services across various industries, including public sector operations, with widespread consequences.

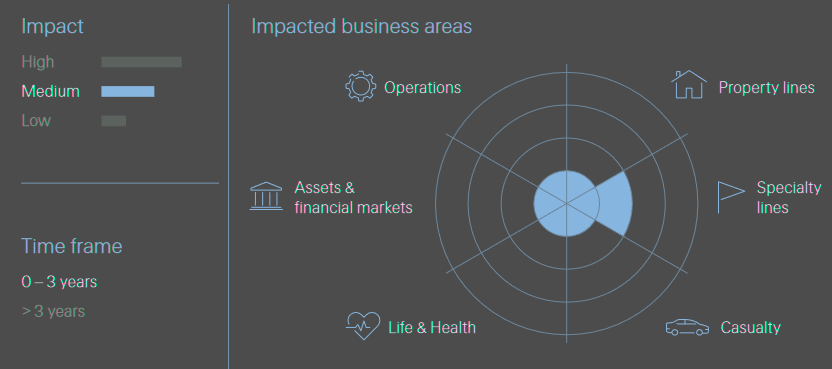

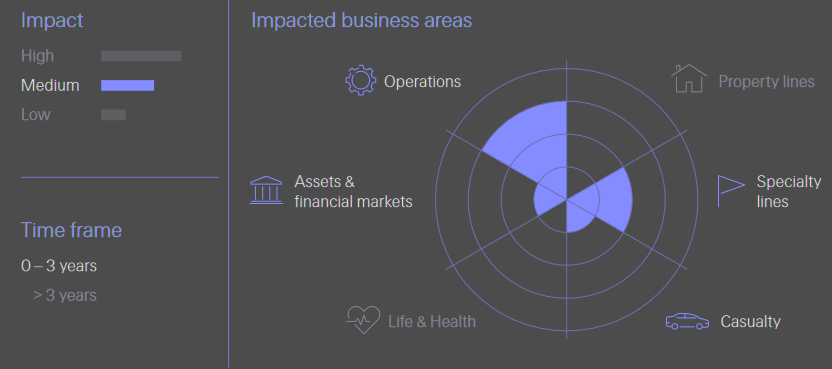

Democratizing Financial Information Through Social Media

Social media has become deeply integrated into daily life, offering various benefits but also posing risks to financial markets and the insurance sector.

Social Media and Financial Markets

Platforms like X (formerly Twitter), LinkedIn, and Reddit have democratized access to financial information. This allows individuals, regardless of expertise, to access real-time financial data and exchange ideas with ease.

The combination of social media and online stock trading has increased retail investor participation by simplifying the process of accessing information and executing trades.

Educational resources on these platforms have also lowered entry barriers for new investors. According to recent reports, 34% of retail investors have altered their investments based on information obtained from social media, and nearly 97% of institutional investors use social media professionally, with 30% reporting that it directly impacts their investment decisions.

However, social media can also spread misinformation, such as in “pump and dump” schemes, which manipulate markets and investor behavior. The rapid spread of false information can lead to short-term market volatility and significant financial losses.

Potential Impacts

- Market Volatility: The fast-paced spread of information can result in irrational investment decisions, asset losses, and market instability, potentially affecting insurers’ profitability.

- Increased Claims: A financial crisis triggered by social media-driven misinformation could lead to more D&O, credit, and surety claims, especially in cases of bank runs or market fallout.

- Cyber Insurance Demand: The financial fallout from misinformation may increase corporate demand for cyber insurance.

- Reputational and Liability Risks: Social media could heighten reputational and commercial liability risks, along with contributing to social inflation.

- Opportunities for Insurers: On the positive side, insurers can leverage social media data to better assess risks, tailor products, and detect fraud. Additionally, social media tools can enhance customer engagement through direct feedback channels.

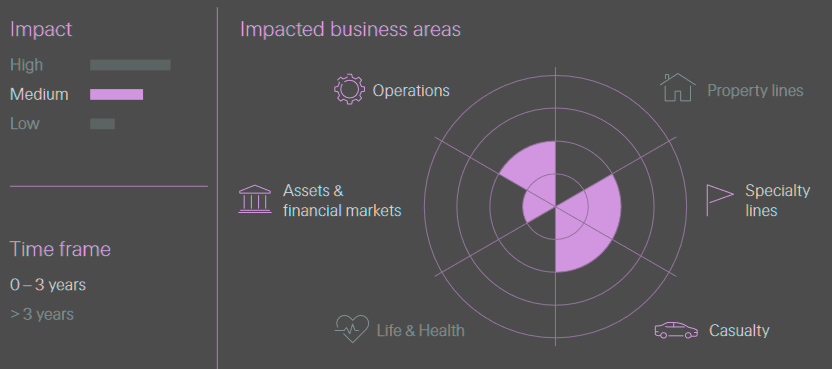

Beyond Broken Infrastructure: The Cascading Effects of Natural Catastrophes

Natural catastrophes such as floods, wildfires, and severe storms frequently cause significant property damage, resulting in large economic and insurance losses.

The less visible but equally critical impacts are the cascading effects on essential societal systems, such as energy, water, and transport infrastructure.

These underlying systems, when disrupted by natural disasters, can trigger further widespread consequences that go beyond the initial damage, affecting both the economy and public safety. Understanding these interconnected risks is crucial for building resilience against future events.

Potential Impacts of Cascading Effects from Natural Catastrophes

- Loss Accumulation: The compounding effects of natural hazards, combined with the interconnected nature of critical infrastructure and supply chains, can lead to significant loss accumulation.

- Insurance Claims: Damage to vital infrastructure like transmission lines and power plants during natural disasters can result in claims under property and business interruption insurance.

- Critical Service Outages: The cascading effects of natural disasters, such as power outages, water contamination, and transport disruptions, can trigger various claims:

- Business Interruption: Costs incurred from business closures, power and water issues.

- Contingent Business Interruption: Impacts on organizations that depend on consistent power supply, such as hospitals, data centers, and security systems.

- Property Damage: Secondary effects like food spoilage due to power outages affecting refrigeration systems.

- Life & Health (L&H) and Liability: Claims related to impacts on medical facilities or water contamination caused by infrastructure failures. Insurers may also experience operational disruptions from these cascading effects.

- Wider Economic Impact: Prolonged and accumulating impacts from natural catastrophes can hinder economic development, increase public sector costs, and potentially slow insurance market growth.

Wildfires’ Toxic Legacy: Water Contamination and Shortages

Wildfires not only cause immediate destruction but also leave behind a toxic legacy, contaminating water supplies and cutting off access to clean water. Ash and debris from fires can pollute water sources, necessitating expensive treatment efforts and potentially leading to water shortages.

The 2018 California wildfires, for example, resulted in tens of billions of dollars in damages, including significant costs for repairing water infrastructure and treatment facilities. Millions of Californians faced concerns over water quality as a result.

Floods can worsen these issues, washing sediment from eroded hillsides into rivers and basins, overwhelming treatment plants, and increasing the risk of disease outbreaks. During the 2023 wildfire in Maui, damage to power lines disabled water pumps, leaving nearly 40,000 residents without water for days.

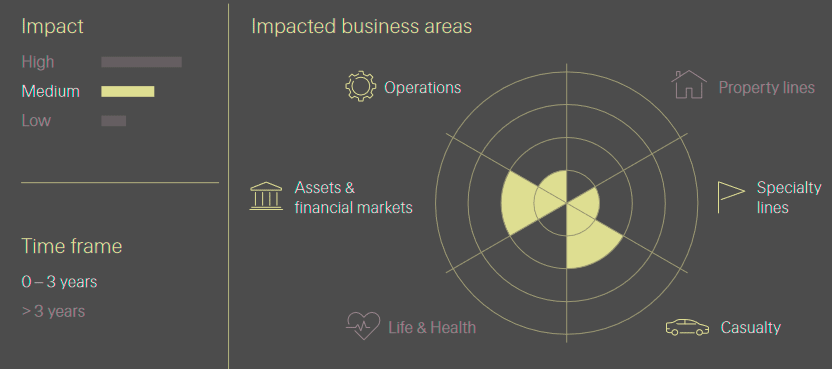

Cyber-Enabled Fraud: A New Era for Organized Crime

Cyber-enabled fraud is transforming organized crime. Criminals now have access to “crime-as-a-service” products available online, allowing them to scale their operations using advanced technology.

This shift has significant consequences, with substantial monetary losses and broader impacts. No one is immune to these risks, as fraudsters increasingly leverage new tools to carry out their activities on a larger scale.

Potential Impacts of Cyber-Enabled Fraud

- Direct Monetary Losses: Operational fraud can result in direct financial losses, such as when criminals hack business emails to manipulate money transfers. Fraudulent claims, like fake emails to healthcare insurers requesting reimbursements for nonexistent treatments, also contribute to these losses.

- Triggered Insurance Covers: Depending on the nature of the fraud, various insurance policies—such as liability or cyber insurance—may be triggered.

- Increased Operational Costs: Significant fraud losses, coupled with the need for investments in preventive security measures, can raise operational costs for insurers. These costs may ultimately be passed on to consumers through higher premiums.

- Reputational Damage: Companies that fail to adequately invest in cyber security may face reputational damage, which can have long-term business consequences.

- Market Volatility: Large-scale financial losses due to fraud can erode trust in financial service providers, potentially leading to market instability.

Organized criminal groups generate profits from various interconnected illegal activities, such as drug, human, and arms trafficking, along with other illicit goods.

Technology facilitates these operations by allowing criminals to connect with each other and reach consumers directly. Cyber-enabled fraud has emerged as a major revenue source, and it no longer requires advanced technical skills.

Criminals can now purchase “crime-as-a-service” products or business models online. Unlike cyber-dependent crimes like hacking or deploying malware, cyber-enabled fraud leverages technology to scale traditional fraud, making it more accessible and profitable.

AI: Unintended Insurance Impacts and Lessons from “Silent Cyber”

The growing adoption of artificial intelligence (AI) may lead to claims across multiple insurance lines. Insurers must proactively understand both the intended and unintended consequences of AI technologies.

This knowledge will be essential in designing products that effectively address the emerging risks associated with AI and in preventing potential coverage gaps similar to those seen with “silent cyber” risks.

Potential Impacts of AI on Insurance

AI-related incidents can affect various lines of insurance, leading to claims across multiple areas:

- Business Interruption: AI system malfunctions that cause operational shutdowns could result in business interruption claims.

- Professional Liability: Claims may arise against professionals for erroneous advice, misinterpretations, or unexplainable decisions made by AI-driven tools, negatively impacting users.

- Product Liability: Manufacturers of AI-enhanced products could face property damage or bodily injury claims due to AI failures or malfunctions, especially if product liability regulations are breached.

- D&O and Liability: Corporate leaders might be held accountable for failing to manage the risks associated with AI-driven processes, resulting in financial losses or reputational damage, potentially triggering D&O and liability claims.

- Employment Practices: AI-driven hiring practices that unintentionally introduce bias could lead to discrimination lawsuits and claims for unfair employment practices.

- Intellectual Property: Copyright violations or patent infringements resulting from the use of AI-generated content or training data could generate claims under liability coverages.

- Healthcare: The increased use of AI in healthcare diagnostics may alter insurance demand, but also create potential gaps in coverage.

- Underwriting and Discrimination: Insurers may see an increase in claims due to erroneous advice or misinterpretations from AI-driven underwriting tools. Additionally, bias introduced by these models could trigger discrimination lawsuits and claims against insurers.

AI has fundamentally changed business operations and is poised to further revolutionize global business practices. Generative AI, which creates text, images, videos, and other outputs, offers numerous advantages but also introduces significant risks. With AI-related incidents rising quickly, C-suite awareness of these dangers is increasing as well.

AI will significantly impact the insurance industry in various ways. It can enhance underwriting, support customer service, automate claims processing, and improve fraud detection through predictive analytics. Despite these advancements, the core function of insurance remains unchanged: providing risk transfer. In this context, insurers will offer protection against the growing range of risks their clients face due to increased AI adoption.

…………..

AUTHORS: Victor Blanco Gonzalez, Vincent Bonny, Constanze Brand, Rainer Egloff, Andreas Felderer, Aliona Gerber, Maryam Kashani, Chuan Lim, Anna Mejlerö, Cathrin Merscher, Vincent Roland, Alexander Weise, Bernd Wilke – Swiss Re