Overview

- Insurtech funding rounds reached extreme levels

- The hype and anticipation around AI

- InsurTech funding picked up in 2025 after three weak years

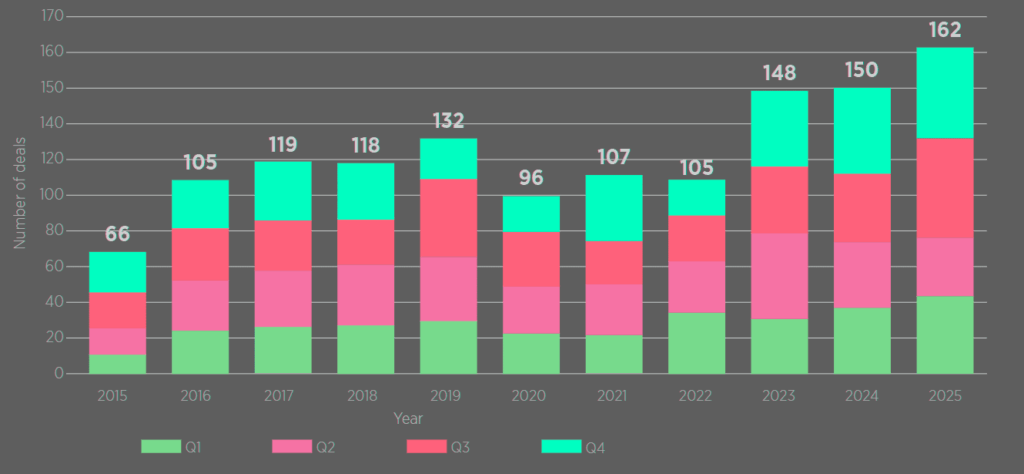

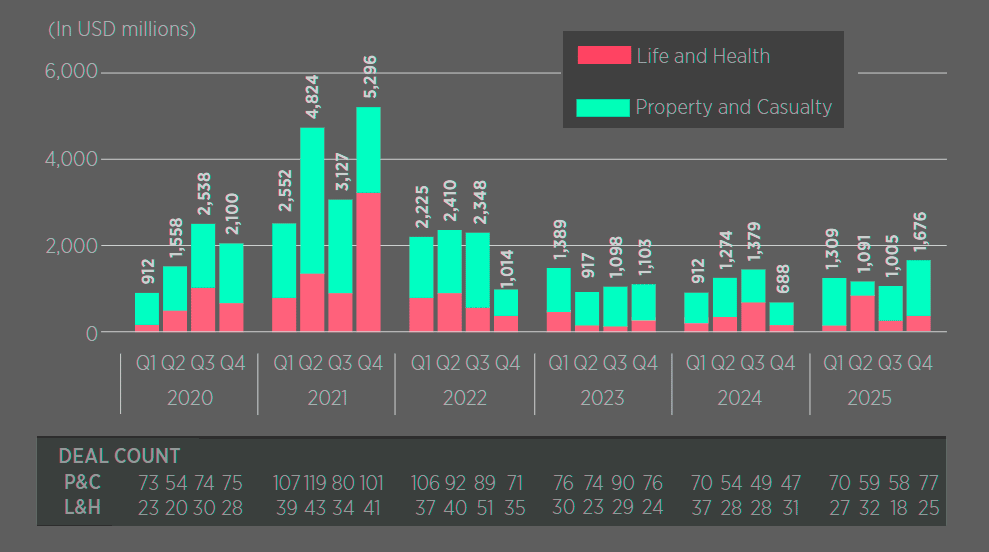

- Quarterly InsurTech Funding Volume – All Stages

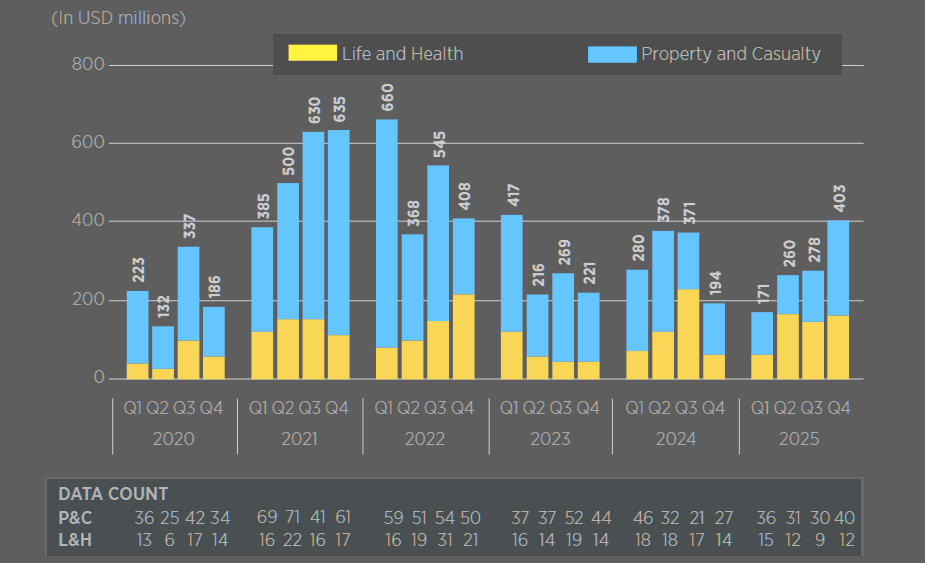

- Quarterly InsurTech Funding Volume – Early Stage

- InsurTech by the Numbers

- Total InsurTech Funding Volume and Transaction Count

- AI-focused InsurTechs drew most of the capital

AI has pushed this period into a golden age for technology. The pace is unusual. Few innovations have drawn capital and reached users so fast, and fewer still have improved both new computing tools and the older systems around them.

Estimates suggest big tech companies put more than $1 tn into data centers and related infrastructure in 2025, with AI as the clear target. Optimism around the technology does not look thin.

2025 became the biggest year for AI so far, inside insurance and far beyond it. Competition among consumer-facing platforms such as DeepSeek, ChatGPT, and Gemini intensified, and valuations across AI firms climbed to fresh highs, according to Gallagher Re’s Report for Q4’2025.

Key Highlights

- AI entered a defining growth phase in 2025, with more than $1 trn invested by big tech into data centers and related infrastructure, making it one of the fastest-scaled technology waves in history.

- InsurTech startups funding rebounded strongly in 2025, rising 19.5% year over year to $5.1 bn, marking the first annual increase since 2021 and signaling renewed investor confidence.

- AI-focused InsurTechs attracted the majority of capital, securing roughly two-thirds of total annual funding and dominating Q4 2025 with nearly 78% of all quarterly investment.

- The US strengthened its leadership in insurance technology, increasing its share of global InsurTech deals to 55.74%, while Silicon Valley nearly doubled its share of activity.

- AI is becoming central to insurance strategy, especially in Life, Accident, and Health, where InsurTechs are helping carriers improve product development, efficiency, and long-term competitiveness.

Specifically, we will explore the transformative impact of AI on the life, accident & health (LAH) class of business.

We look at InsurTechs collaborating with incumbent carriers to enhance the development of insurance products, as well as examining those innovative businesses offering their own standalone solutions in the LAH space.

Dr. Andrew Johnston, Global Head of InsurTech, Gallagher Re

The report also tracks InsurTech market performance in Q4 2025 and across the full year. Funding rebounded in 2025, with total investment rising 19.5% year over year to $5.08 bn. It was the first annual increase since 2021.

Part of that rebound came from a sharp Q4 jump. Global InsurTech funding rose 66.8%, climbing from $1.01 bn in Q3 2025 to $1.68 bn in Q4 2025. P&C drove much of the increase, with funding up 90.5% quarter over quarter to $1.31 bn. L&H also moved higher, rising 14.9% to $361.52 mn.

The market also widened. More than 100 InsurTechs raised funding, the first time deal count crossed that level since Q1 2024. Total deals increased 34.2% quarter over quarter to 102, while average deal size rose 20.0% to $18.84 mn in Q4 2025.

Insurtech funding rounds reached extreme levels

OpenAI, for example, raised $40 bn in April 2025 at a $300 bn valuation. More important, though, AI has moved into the center of corporate strategy. Few management teams now discuss growth, investment, or operating plans without it somewhere in the frame.

Insurance has followed the same path. The industry has poured bn into AI through internal projects, partnerships with AI firms, and direct investments in AI companies, including businesses that identify as InsurTechs.

The shift brings optimism and unease at the same time. Companies worry about falling behind, even becoming obsolete. They also see a shot, at last, that AI delivers the returns and efficiency gains the market expected from InsurTech over the past 15 years.

Global InsurTech Funding Overview

| Metric | 2024 | 2025 | Change |

| Total Funding | $4.25 bn | $5.1 bn | +19.5% |

| Deal Count | 344 | 366 | +6.4% |

| Avg Deal Size | $13.85 mn | $15.79 mn | 14% |

| Mega-round Funding | $930 mn | $1.43 bn | +53.2% |

The hype and anticipation around AI

The hype and anticipation around AI has also driven spectacular gains on the financial markets, largely driven by 10 or so firms that are pioneers of the latest and greatest AI offerings. What drives the accelerated AI adoption in the insurance industry?

Data companies, chip providers, data storage, intelligent search and digital distribution firms have coalesced to create the foundations of a whole new AI industry. Nevertheless, we should also be realistic about the potential pitfalls.

The incredibly high stock-market valuations of AI companies do seem to have run far ahead of what they are generating in revenue – at least for now.

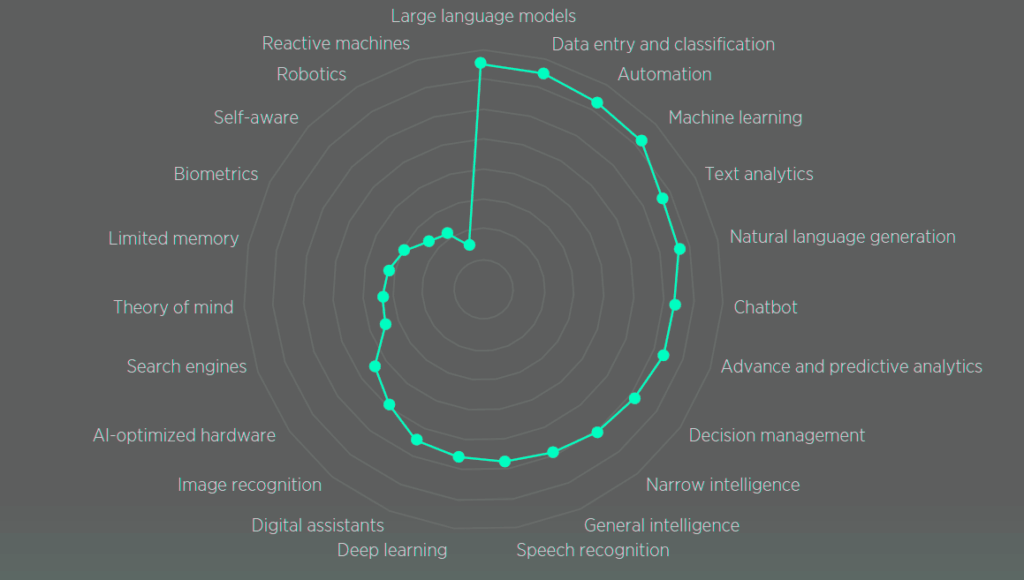

Spread Map of Most Applicable AI Technologies

As with most speculations, only time will tell. We do know that AI is here to stay; what we do not yet know is the extent to which hype can be separated from reality. InsurTech shifts from disruption hype to durable insurance tech models. We also do not know which features and functions of AI will go the distance, and which will be discarded.

As of October 2025, 6 bn individuals worldwide were internet users, which amounted to 73.2% of the global population.

It has been so transformational to human society that it would be both impossible, and disingenuous, to attempt to put a financial value on “the internet”. It would be like trying to quantify the value of a transport system by number of tickets sold, instead of the world that it facilitates.

One of the many lessons we can take from previous hype cycles is to separate, define and clearly understand offerings at a product, company and industry-wide level.

Only then can we appreciate where the long-term value will come from, and not be deterred in the short term if AI doesn’t deliver on some of the wilder science-fiction promises over the next 18 months. We know the history of the internet from 2000-2025.

Perhaps in another 25 years’ time, AI will be driving every digital process and interaction that we have. Perhaps it will redefine communication and distribution throughout our daily lives. Viewed from that perspective, the short-term stock prices of individual businesses or brands matter less.

The financial markets follow, and investments from the wider society begin

In among the noise, development does occur, and winners are created – infrastructure and tools are rolled out and used in industry.

There is then the inevitable slowdown (often a crash) when investors realize that a price correction is incoming (as individual companies release their financials).

But over time, the seeds sewn in these early phases set the path for long-term impact and ultimately success. AI in reinsurance is no different – we should just be honest about what is going on without taking our eye off the long-term prize.

AI is squarely the focus of most of the contemporary InsurTech world

In Q3 report, we showed that approximately three-quarters of all funding is now going into InsurTech businesses that associate themselves with the AI label (whether they are AI-powered themselves, or are providing AI tools to others).

We do not see this trend slowing down. In fact, we see AI becoming so integrated into InsurTech over time that the two may well become effectively synonymous – in much the same way as we could already argue that “InsurTech” is itself a meaningless label, because all insurers are technology businesses now.

So it might seem strange that InsurTech investing has experienced a period of comparative stability while interest in the broader AI sector has soared. Generative AI attracts increased venture capital funding in 2025.

AI vs Non-AI Investment Share

| Category | Funding Share | Deal Share |

| AI-focused InsurTechs | 66% | 62% |

| Non-AI InsurTechs | 34% | 38% |

The extent to which the two are correlated remains to be tested. But as we noted in our prior report, for the past three years, almost every single quarter of InsurTech funding has fallen within a 10% swing of the mean average: approximately $1.1 bn. This consistency is quite remarkable in the context of the aforementioned excitement over AI.

A changing of the guard among InsurTech investors

There has been a notable shift in the InsurTech investor community. During 2025, (re)insurers made more private technology investments into InsurTechs than in any other year on record.

This suggests that (re) insurers are not only more comfortable investing, but also that they see InsurTechs as a route forward in their own strategies.

Private Technology Investments by (Re)Insurers

InsurTech funding picked up in 2025 after three weak years

Total investment rose 19.5% year on year to $5.1 bn, the first annual gain since 2021. Q4 drove part of the shift. Global InsurTech funding jumped 66.8%, rising from $1.01 bn in Q3 2025 to $1.68 bn in Q4 2025.

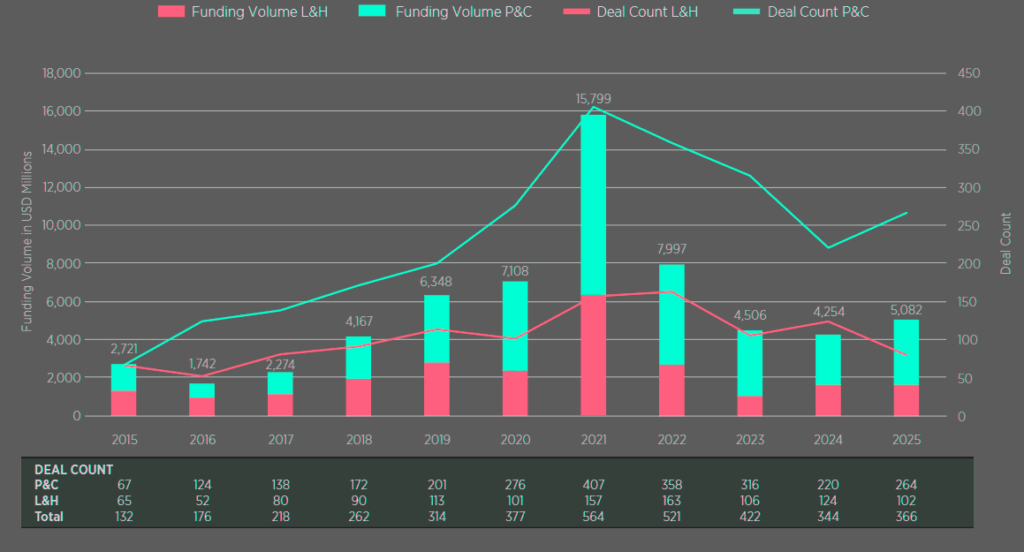

Insurance Segment Performance

| Segment | Funding | YoY Change |

| P&C | $3.49 bn | +34.9% |

| Life, Accident & Health (LAH) | $1.59 bn | -4.6% |

P&C posted the sharper recovery

Funding in that segment rose 34.9% from 2024’s trough to $3.49 bn in 2025. L&H moved the other way, with funding slipping modestly over the year.

Across both segments, investors kept backing standalone technology firms over businesses selling themselves as tech-enabled brokers and MGAs. The tilt wasn’t subtle (see Top Insurance Claims Management Software Platforms).

Q4 2025 InsurTech funding snapshot

| Metric | Value |

| Total Funding | $1.7 bn |

| Deals | 102 |

| Avg Deal Size | $18.8 mn |

| AI Share | 77.9% |

| Early-stage Funding | $403 mn |

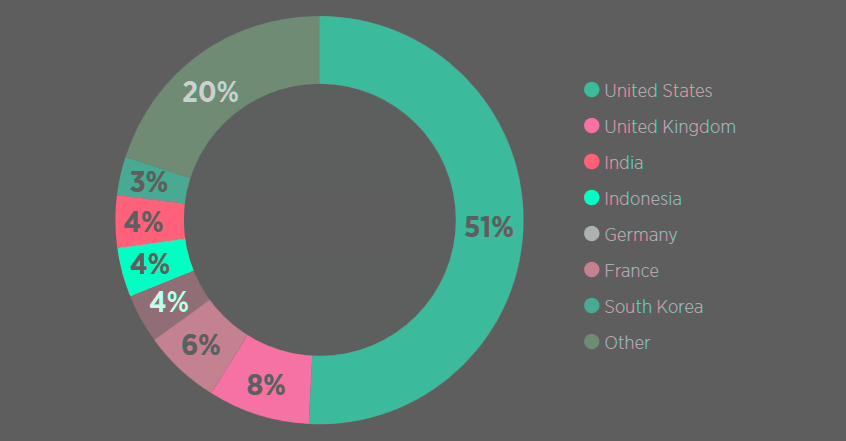

The United States widened its lead in insurance technology

Its share of global InsurTech deals increased by 5.16 percentage points between 2024 and 2025, the largest gain recorded by any country. AI also pulled in a huge slice of capital.

Roughly two-thirds of annual InsurTech funding went to AI-focused companies, with more than $3.3 bn raised across almost 230 deals, according to Beinsure analysts.

Global InsurTech funding rose from $4.25 bn in 2024 to $5.08 bn in 2025. The market’s annual increase leaned heavily on a sharp rise in $100 mn-plus mega-rounds.

Those deals increased from six to 11 over the year, lifting mega-round funding 53.2% from $930 mn to $1.43 bn. Deal count also edged higher, up 6.4% from 344 in 2024 to 366 in 2025.

That gain looks modest on paper, still it broke the steady slide seen since the 2021 peak. Average deal size rose 14% to $15.79 mn.

Quarterly InsurTech Funding Volume – All Stages

Early-stage InsurTech moved against the broader market

Funding fell 9.1% year on year from $1.22 bn in 2024 to $1.11 bn in 2025. Deal count also dipped, from 193 to 185. Even so, the average early-stage round rose 12.1% to $6.6 mn in 2025, which points to steady demand for younger firms that did secure backing (see How AI Agents Speed Up the First Step in Insurance Claims).

The number of active InsurTech investors also increased for the first time since 2021, climbing from 788 in 2024 to 852 in 2025.

Q4 2025 delivered the strongest quarter since Q3 2022, when funding reached $2.35 bn.

- P&C led the quarter’s surge, with funding up 90.5% quarter on quarter to $1.31 bn.

- L&H also advanced, rising 14.9% to $361.52 mn.

Quarterly InsurTech Funding Volume – Early Stage

More than 100 InsurTechs raised capital in a quarter for the first time since Q1 2024. Total deal count increased 34.2% quarter on quarter to 102, and average deal size climbed 20% to $18.84 mn.

Five companies accounted for $662.81 mn in Q4 mega-rounds. CyberCube raised $180 mn in growth equity. ICEYE secured $174.81 mn in a Series E round. Creditas brought in $108 mn in Series G funding. Federato raised $100 mn in Series D funding, and Nirvana matched that with its own $100 mn Series D. Big tickets, no doubt, shaped the quarter.

InsurTech by the Numbers

Quarterly InsurTech Transactions by Target Country

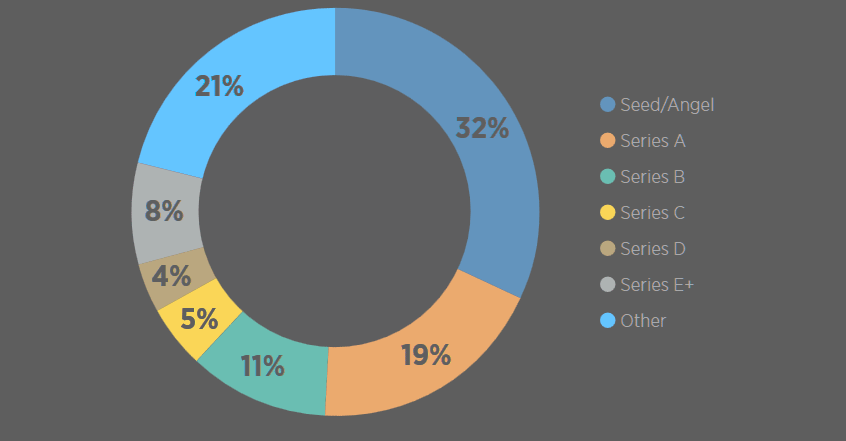

Quarterly InsurTech Transactions by Investment Stage

InsurtTech Funding Geographic Distribution (Deal Share)

| Region | 2024 | 2025 | Change |

| United States | 50.58% | 55.74% | +5.16 pp |

| India | 5.81% | 3.83% | -1.99 pp |

| France | 5.52% | 4.10% | -1.42 pp |

| Germany | 3.20% | 2.19% | -1.01 pp |

Early-stage activity also strengthened late in the year

Funding reached an 11-quarter high, rising from $277.65 mn in Q3 2025 to $403.09 mn in Q4 2025. Both P&C and L&H contributed to that increase.

P&C funding recovered from its 2024 low and finished 2025 at $3.49 bn. Mega-rounds did much of the lifting. Funding from those deals rose from $320 mn in 2024 to $1.06 bn in 2025, while deal count increased 20% to 264.

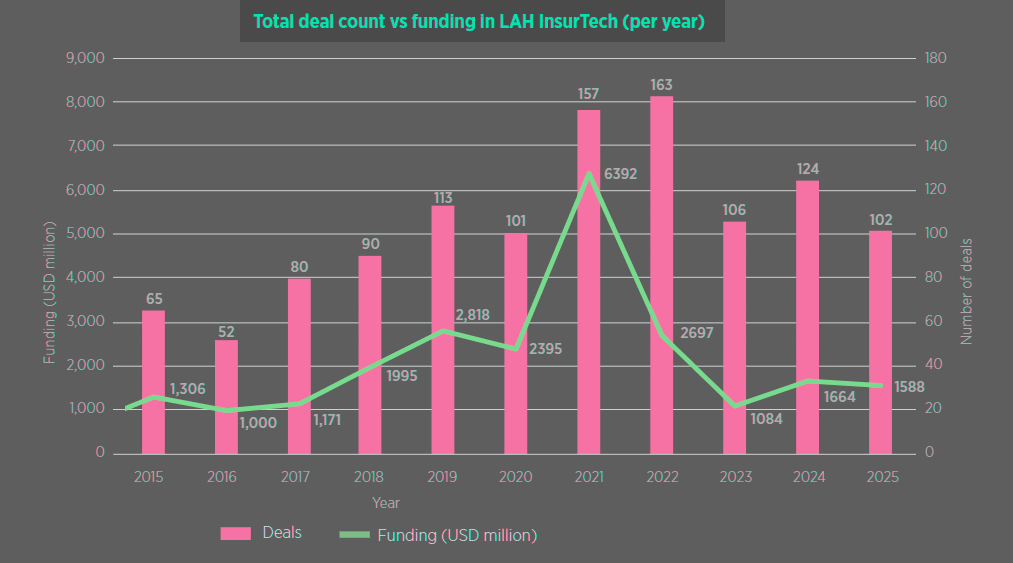

L&H told a different story. Funding fell 4.6% year on year to $1.59 bn, and deal count dropped 17.7% to 102.

Annual Investment into LAH Related InsurTechs

Tech vendors took a larger share of activity across both P&C and L&H

In P&C, 58% of deals went to B2B InsurTechs in 2025, up 12 percentage points from the 2021 funding boom.

Over the same period, the share going to lead generation, broker, and MGA firms fell from 42% in 2024 to 35% in 2025, the lowest level on record.

In L&H, B2B InsurTechs accounted for 64% of 2025 deals, up one percentage point from 2024. According to our data, investors kept chasing software-first businesses, and they weren’t shy about it.

Total InsurTech Funding Volume and Transaction Count

US-based InsurTechs pulled further ahead in 2025

Their global deal share rose 5.16 percentage points year on year, the largest increase among all countries.

The numbers show a clear shift. US deal share climbed from 50.58% in 2024 to 55.74% in 2025. Activity concentrated more heavily in Silicon Valley, where deal share jumped from 8.72% to 16.12%.

Three years straight now, most InsurTech deals have landed in the United States. According to Beinsure analysts, no other market came close.

Elsewhere, movement stayed limited. Bermuda recorded the only other increase above one percentage point. India posted the steepest drop, with deal share falling 1.99 percentage points, from 5.81% to 3.83%.

Several European markets also slipped. France declined by 1.42 percentage points to 4.10%. Canada and Germany each fell by 1.01 points to 2.19%. Switzerland dropped 0.92 points to 0.82%. The Netherlands fell 0.91 points to 0.55%. The shift feels broad, not isolated.

AI-focused InsurTechs drew most of the capital

In Q4 2025, they accounted for 77.9% of total funding. These companies raised $1.31 bn across 66 deals, with an average ticket of $22.14 mn, slightly above the quarterly average.

Across the full year, AI-driven firms secured $3.35 bn through 227 deals. That equals 66% of total funding and 62% of deal volume. Investors kept writing larger checks here. The pattern held all year.

Life, accident, and health InsurTechs have raised $25.15 bn since 2012. That total spans 1,272 deals, representing 32.6% of all InsurTech transactions over the period. Y Combinator led investors with 105 deals. Plug and Play Ventures followed with 86. Anthemis recorded 64. A tight group, still active.

(Re)insurers stepped up venture activity in 2025

They completed 162 tech investments, the highest annual count on record. Even so, Q4 slowed. Investment count dropped from 51 in Q3 2025 to 35 in Q4 2025.

US-based firms accounted for 16 of those deals. Japan, the United Kingdom, and France also logged multiple transactions.

Mitsui Sumitomo Insurance led corporate venture activity in Q4. It closed nine investments through its venture units. Partnerships also picked up pace late in the year. Certificial worked with Zurich North America. CyberCube partnered with MS Amlin. Salesforce linked with Singlife. ZestyAI teamed with TruStage.

Methodology

What do we consider an “InsurTech investment”?

For analysis in this report, we consider equity funding into private companies only. Funding rounds verified by the end of the quarter are included.

Funding rounds are verified via:

- various federal and state regulatory filings;

- direct confirmation with the firm or investor;

- press release or

- credible media sources.

Investment from accelerators, incubators, business-plan competitions and economic development entities are excluded. As such, there are some deals that might constitute a raise in other circumstances that we do not consider in our data. Consequently, the numbers and data we do present should be considered a minimum benchmark.

FAQ

AI has rapidly attracted massive capital (over $1 trn in 2025) and reached users faster than most past innovations. It is improving both new digital tools and legacy systems simultaneously.

Like the internet, AI is transformative and difficult to value directly. Early hype may not match short-term results, but long-term structural impact is expected to be profound.

Funding rose 19.5% to $5.1 bn, driven by AI-focused investments, mega-rounds, and renewed investor confidence after three weaker years.

Markets are pricing in future potential rather than current earnings, leading to valuations that may exceed near-term financial performance.

AI enables better product development, risk assessment, underwriting, and customer experience, often through partnerships between InsurTechs and traditional insurers

InsurTechs act as innovation drivers – either collaborating with incumbents or offering standalone AI-powered solutions in insurance.

Not entirely, but it will redefine them. AI is becoming central to strategy, and over time, “InsurTech” and “AI-driven insurance” may become indistinguishable

………………

AUTHOR: Dr. Andrew Johnston, Global Head of Gallagher Re

Edited by Peter Sonner, Lead Tech Editor at Beinsure Media, Fact-checked by Oleg Parashchak, CEO Finance Media & Editor-in-Chief at Beinsure (25+ years of professional experience in Rankings, Insurance & Media), Jerry Boone – Co-founder of L’École des Startups