Overview

- Cumulative Insurtech VC funding

- Early-Stage and Late-Stage Startups Struggle to Recover

- Global VC funding in insurtech startups

- B2B SaaS Startups Capture 43% of Funding

- TOP 25 investors in global insurtech startups in Seed Rounds

- TOP 25 investors in global insurtech startups in Series A

- TOP 25 investors in global insurtech startups in Series B

- Key Trends: Generative AI, Climate Risks, and Health

Venture capital funding in insurtech startups is stabilizing, driven by breakout-stage startups in Series B and C. Projections indicate it will reach $4.2 bn by the end of 2024, aligning with 2018 and 2023 figures. Funding reached $3.2 bn in the first three quarters, 7% lower than 2023. Despite this, positive trends suggest a rebound by year-end.

Insurtech VC funding in 2024 is projected to be almost on par with last year. Looking back, it peaked in 2021 and then dropped over two thirds. Now we are back to 2018 levels.

Late-stage startups (seeking over $100 mn) face the steepest decline, with nearly 90% lower funding than their 2021 peak. These startups are expected to contribute significantly to the year’s final funding push as they strengthen unit economics for future exits, according to The State of Global Insurtech Report by Dealroom, Mundi Ventures and MAPFRE. Beinsure Media has selected the most important points from the report.

Key Highlights

- Q3 2024 closed with $3.2 bn in insurtech investment, down 7% from 2023. Despite this, funding trends indicate a likely rebound in the fourth quarter, stabilizing at 2018 levels.

- Breakout-stage companies (Series B and C) are driving this stabilization, nearing pre-pandemic funding levels. Early-stage startups (pre-seed, seed, and Series A) are also contributing, though late-stage startups continue to face funding challenges. These difficulties highlight market caution toward mature, high-valuation firms.

- The U.S. remains the top growth driver, attracting $1.8 bn in investment, followed by Europe with $1.1 bn. Emerging markets like Africa and Latin America lag significantly, securing $32.4 mn and $37.1 mn, respectively.

- B2B SaaS startups dominate, capturing 43% of total funding. These companies include providers of payment solutions, risk management tools, underwriting software, and claims administration platforms. Many are AI-focused or expanding portfolios with new AI-based offerings.

The U.S. leads in insurtech funding, followed by Europe, with investments of $1.8 bn and $1.1 bn, respectively. Both regions maintain positive momentum (see Top 50 Global InsurTech Startup Investors).

After the uncertainty of previous years, the global insurtech market is now showing signs of further stabilization. While the frenzy has cooled, weʼre seeing a positive rebound in the early-growth / breakout stages, particularly with Series B funding picking up.

Javier Santiso, CEO and General Manager, Mundi Ventures

The late-stage market remains significantly constrained, with a freeze in growth and IPO phases. Insurtech startups are now gearing up for potential IPOs in 2025 or 2026, setting profitable models and waiting for more favorable market conditions. This cautious environment is shifting investor focus towards proven business models with solid unit economics.

Cumulative Insurtech VC funding

Early-Stage and Late-Stage Startups Struggle to Recover

Late-stage funding scarcity remains a key challenge, but early-stage startups in pre-seed, seed, or Series A phases also show a 50% decline from their 2021 peak.

Series B and C startups lead funding, expected to reach $2.4 bn by 2024’s close. These levels mirror pre-pandemic trends, signaling market stabilization.

Insurtech Challengers (1.0) have adjusted to shifting tech and insurance market dynamics, addressing key industry challenges. Their stock performance has grown steadily over the past two years.

Global VC funding in insurtech startups

With $3.2B raised in 2024, insurtech shows strong investor confidence, despite a 7% dip from last year, slightly underperforming the market but still outpacing fintech.

What we are seeing worldwide is a slowdown in the economy since 2022, which is directly impacting investment in insurtech venture capital, some geographies more than others. US and Europe, for example, are back on track and showing an optimistic performance.

Leire Jiménez, Chief Innovation Officer, MAPFRE

However, Asia and Latin America are struggling to raise, the latter with funding at historic lows. Still, the Latin American ecosystem is resilient, and entrepreneurs continue to seek new formulas, models, and businesses to revitalize the sector.

The region has great potential, more so at a time when the insurance gap is gradually shrinking due to the large volume of opportunities in it. Collaborative spaces and public-private partnerships are key to stabilize the market and drive it forward.

Global VC funding by industry in 2024

VC funding growth by Industry, 2024

Late stage is the main cause of funding decrease in insurtech. Early and breakout stage have fared better but are still down ~50% from peak.

Early-stage is back to 2017, down 50%+ from peak

Breakout stage is up from last year and almost back to pre-pandemic level

Late-stage has fallen dramatically

U.S. and Europe Dominate Investment

The U.S. leads in insurtech funding, followed by Europe, with investments of $1.8 bn and $1.1 bn, respectively. Both regions maintain positive momentum.

In contrast, emerging markets like Latin America struggle, securing $37.1 mn, a historical low. However, narrowing insurance penetration gaps and internal investment rounds signal optimism for future growth in the region.

VC funding in insurtech by region in 2024

Share of insurtech VC funding by region

Challenger insurtechs have gained valuable insights from past experiences, and the market is signalling their potential to deliver significant value to the industry.

Challenger insurtechs secured substantial early-stage funding, but in recent years, they have faced significant challenges and steep learning curves, which have driven important lessons for the broader insurtech ecosystem:

- The “growth at all costs” strategy has proven unsuitable for the insurance industry. Insurance requires precise risk assessment and pricing, making aggressive growth difficult to sustain.

- The rising cost of capital and interest rates have not only reduced investment in ventures but have also constrained the insurance capacity that traditional insurers and reinsurers are willing to underwrite.

- Insurtech IPOs have underperformed compared to other industries, with investor excitement peaking in 2021. This enthusiasm led insurtechs to scale rapidly, akin to SaaS companies, resulting in the creation of unprofitable insurance books.

B2B SaaS Startups Capture 43% of Funding

B2B SaaS startups dominate, securing 43% of total funding—the highest on record. These include providers of software, pricing tools, risk management solutions, underwriting technology, and reinsurance systems. Many leverage AI or expand portfolios with AI-driven solutions.

The life and health insurance segment (L&H) now matches property and casualty insurance funding at 50%, marking a three-year first. L&H growth is driven by health insurance, while P&C benefits from increased climate risk and business insurance demand.

B2B SaaS share of insurtech VC funding

TOP 25 investors in global insurtech startups in Seed Rounds

| № | Investor | Insurtech Rounds 2023-2024 | Insurtech Rounds 2019-2024 | % Insurtech deals 2019-2024 |

| 1 | Plug and Play | 6 | 54 | <25% |

| 2 | Anthemis Group | 3 | 46 | 25-50% |

| 3 | Insurtech Gateway | 7 | 34 | 50%+ |

| 4 | 500 Global | 1 | 24 | <25% |

| 5 | Global Founders Capital | 1 | 22 | <25% |

| 6 | Greenlight Reinsurance | 5 | 20 | 50%+ |

| 7 | Markd | 17 | 20 | 50%+ |

| 8 | Foundation Capital | 5 | 20 | <25% |

| 9 | Antler | 4 | 18 | <25% |

| 10 | Bpifrance | 5 | 18 | <25% |

| 11 | Clocktower Technology Ventures | 3 | 17 | <25% |

| 12 | Portage Ventures | 4 | 15 | <25% |

| 13 | SixThirty Ventures | 3 | 15 | <25% |

| 14 | BrokerTech Ventures | 3 | 13 | 50%+ |

| 15 | Susa Ventures | 0 | 13 | <25% |

| 16 | Core Innovation Capital | 2 | 13 | <25% |

| 17 | Seedcamp | 2 | 13 | <25% |

| 18 | Andreessen Horowitz | 5 | 12 | <25% |

| 19 | Partech | 1 | 12 | <25% |

| 20 | Fin Capital | 5 | 11 | <25% |

| 21 | Liquid 2 Ventures | 2 | 11 | <25% |

| 22 | Astorya vc | 3 | 11 | 50%+ |

| 23 | MetaProp | 3 | 10 | <25% |

| 24 | AV8 Ventures | 3 | 10 | <25% |

| 25 | Elaia Partners | 3 | 10 | <25% |

TOP 25 investors in global insurtech startups in Series A

| № | Investor | Insurtech Rounds 2023-2024 | Insurtech Rounds 2019-2024 | % Insurtech deals 2019-2024 |

| 1 | MS&AD Ventures | 5 | 35 | 25-50% |

| 2 | MassMutual Ventures | 6 | 25 | <25% |

| 3 | Munich Re Ventures | 7 | 24 | 25-50% |

| 4 | IA Capital Group | 5 | 23 | 25-50% |

| 5 | MTech Capital | 4 | 21 | 50%+ |

| 6 | American Family Ventures | 4 | 20 | 25-50% |

| 7 | Lightspeed Venture Partners | 4 | 20 | <25% |

| 8 | Greycroft Partners | 1 | 19 | <25% |

| 9 | ManchesterStory | 5 | 18 | 25-50% |

| 10 | Nationwide Ventures | 5 | 16 | 50%+ |

| 11 | Eurazeo | 5 | 16 | <25% |

| 12 | Crosslink Capital | 4 | 16 | <25% |

| 13 | Octopus Ventures | 3 | 16 | <25% |

| 14 | Eos Venture Partners | 4 | 15 | 50%+ |

| 15 | QED Investors | 2 | 15 | <25% |

| 16 | CommerzVentures | 1 | 15 | 25-50% |

| 17 | Khosla Ventures | 1 | 15 | <25% |

| 18 | Flourish Ventures | 2 | 13 | <25% |

| 19 | Founders Fund | 2 | 13 | <25% |

| 20 | Maverick Ventures | 4 | 12 | <25% |

| 21 | Intact Ventures | 3 | 12 | 25-50% |

| 22 | Sequoia Capital | 2 | 12 | <25% |

| 23 | True Ventures | 2 | 11 | <25% |

| 24 | GreatPoint Ventures | 2 | 10 | <25% |

| 25 | AXA Venture Partners | 2 | 10 | <25% |

TOP 25 investors in global insurtech startups in Series B

| № | Investor | Insurtech Rounds 2023-2024 | Insurtech Rounds 2019-2024 | % Insurtech deals 2019-2024 |

| 1 | Mundi Ventures | 10 | 37 | 50%+ |

| 2 | Aquiline Capital Partners | 3 | 16 | 25-50% |

| 3 | Brewer Lane Ventures | 4 | 15 | 50%+ |

| 4 | Insight Partners | 3 | 15 | <25% |

| 5 | Bessemer Venture Partners | 4 | 14 | <25% |

| 6 | SCOR | 2 | 12 | 50%+ |

| 7 | SoftBank | 0 | 12 | <25% |

| 8 | Cathay Innovation | 0 | 12 | <25% |

| 9 | Valor Equity Partners | 3 | 10 | 50%+ |

| 10 | Mubadala Capital | 2 | 10 | <25% |

| 11 | Tencent | 2 | 10 | <25% |

| 12 | Ribbit Capital | 1 | 10 | <25% |

| 13 | Viola Fintech | 0 | 10 | 25-50% |

| 14 | Vertex Holdings | 0 | 10 | <25% |

| 15 | Norwest Venture Partners | 1 | 9 | <25% |

| 16 | New Enterprise Associates | 2 | 9 | <25% |

| 17 | FinTLV | 2 | 9 | 50%+ |

| 18 | Liberty Mutual Strategic Ventures | 2 | 9 | 25-50% |

| 19 | PruVen Capital | 2 | 9 | 25-50% |

| 20 | Coatue Management | 0 | 9 | <25% |

| 21 | Propel Venture Partners | 0 | 9 | <25% |

| 22 | Avanta Ventures | 4 | 8 | 25-50% |

| 23 | Bain Capital Ventures | 2 | 8 | <25% |

| 24 | Menlo Ventures | 1 | 8 | <25% |

| 25 | Tiger Global | 0 | 8 | <25% |

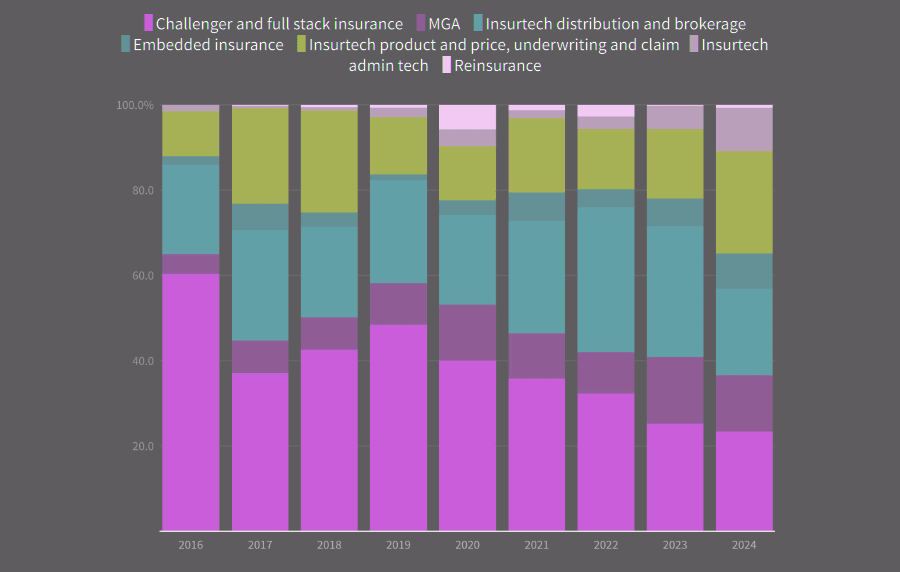

Share of VC funding by insurance value chain

Key insurtech function (product and price, underwriting and claim) attracted the most of the funding in 2024 for the first time, while challengers and MGAs are at a minimum in recent years.

- Challenger and Full-stack insurance. Challenger, full stack & MGA share of funding lowest ever in 2024.

- Insurtech distribution and brokerage. Distribution and embedded insurance is still attracting significant funding, but less than the last three years.

- Insurtech product and price, underwriting and claim. Key insurtech function (product and price, underwriting and claim) attracted the most funding in 2024 for the first time ever.

- Insurtech admin tech. Admin tech platforms have attracted a few big rounds.

L&H attracted 50% of VC funding in 2024, on par with P&C for the first time after three years, driven by Health insurance. Commercial insurance & Climate risk attracted the most in P&C.

Share of VC funding P&C vs L&H

Climate Risk Intelligence & Management is on track for its second most active year ever. Most of the funding has gone to Earth Observation, Parametric Insurance, Climate Risk Financial Modeling and Weather Forecasting & Monitoring (see How Will Generative AI Change the Cyber Insurance?).

VC funding in Climate Risk Intelligence & Management

Key Trends: Generative AI, Climate Risks, and Health

GenAI intersects insurance in multiple ways. GenAI is starting to optimize insurance processes, but on the other hand, insurers must contribute to societal awareness and education by taking preventive measures to reduce the risks to which individuals and companies are exposed. Climate risk intelligence has received considerable and stable funding since 2021.

Venture capital funding for generative AI startups is on track to exceed 2023’s record-breaking levels. In 2024, GenAI startups raised over $40 bn, per S&P Global Market Intelligence data, setting up the year to surpass the $22.7 bn raised in 2023.

With chronic diseases accounting for 70-90+% of healthcare expenses in developed markets, preventive care, early intervention, and better management are gaining increased importance.

Artificial Intelligence has been transforming the world we live in for decades. Generative AI (GenAI) promises to follow the same path, but with a much higher rate of technological development and social and business adoption.

The role of insurance in a society embracing GenAIʼ outlines four plausible scenarios for the year 2029, each highlighting different outcomes based on GenAI’s development, regulation, and adoption. These depict extreme realities, but they are within the realms of possibility. A combination of them will determine how reality is influenced by the evolution of GenAI.

Global Generative AI in Insurance Market size will be worth $5,5 bn by 2032 from its current size of $346.3 mn, and growing at a CAGR of 32.9% through the next decade.

The insurance market is undergoing a remarkable transformation, thanks to the exponential growth of generative artificial intelligence (see How AI Technology Can Help Insurers).

Insurance providers are harnessing the power of artificial intelligence to optimise their operations, improve risk assessment models, and deliver personalised customer experiences.

Generative AI can help navigate the complex regulations of the insurance sector, build up customer data and increase efficiency in some of the industryʼs labour-intensive and time-consuming tasks.

Example use cases:

- Streamlining of sales & distributions with the automation of administrative tasks

- Improvement of underwriting with the collection of data

- Better customer experience with digital human like innovations

- Automation of claims management

The awareness and education of society regarding the responsible and appropriate use of Generative AI is essential in all areas. On those four scenarios, new risks will emerge, while some preexisting risks are exacerbated by the proliferation of GenAI.

Bárbara Fernández Gutiérrez, Deputy Director (Disruptive Innovation) and Head of Insur_Space at MAPFRE

Thus, insurers must take preventive measures to reduce the risks to which individuals and companies are exposed.

In this context, there are some areas of opportunity to pursue for the insurance industry, from new customer relationships and more suitable products, to fraud, cyberprotection, health and mental health, or the responsible use of AI/GenAI.

FAQ: Insurtech Investment Trends and Key Insights

In 2024, product and price, underwriting, and claims attracted the largest funding share for the first time. Distribution and embedded insurance remain significant but have seen declines compared to the last three years. Admin tech platforms secured a few large rounds.

Key players include MS&AD Ventures, MassMutual Ventures, Munich Re Ventures, and Mundi Ventures. Mundi Ventures leads Series B funding globally with 10 rounds and over 50% share of insurtech deals.

Life and health (L&H) insurance captured 50% of funding in 2024, matching property and casualty (P&C) for the first time in three years. Health insurance drove L&H, while climate risks and commercial insurance dominated P&C funding.

This sector is on track for its second most active year, with investments focusing on Earth observation, parametric insurance, climate risk financial modeling, and weather forecasting.

Generative AI (GenAI) optimizes processes such as sales, distribution, underwriting, and claims management. It also enables insurers to handle complex regulations, improve customer experiences, and automate administrative tasks. However, insurers must also address emerging risks and societal education.

Opportunities include tailored products, enhanced fraud prevention, cyber protection, mental health support, and the responsible use of AI. Insurers must also implement measures to mitigate risks associated with GenAI proliferation.

While early-stage and late-stage funding are below their peaks, Series B and C startups are stabilizing the market. The focus on core insurance functions, climate risks, and GenAI suggests steady growth in key segments.

…………………..

QUOTES: Javier Santiso – CEO and General Manager, Mundi Ventures, Leire Jiménez – Chief Innovation Officer at MAPFRE & CEO MAWDY (MAPFRE Worldwide Digital Assistance), Bárbara Fernández Gutiérrez – Deputy Director (Disruptive Innovation) and Head of Insur_Space at MAPFRE

Edited by Oleg Parashchak, Peter Sonner – Beinsure Media