Fire and explosion incidents cause the most expensive insurance claims in the marine industry, while at a time of rising exposures and inflation, cargo damage is the most frequent cause of loss, according to Allianz Global Corporate & Specialty (AGCS).

The marine and cargo insurer analyzed more than 240,000 marine insurance claims worldwide between January 2020 and December 2025, worth approximately €9.2bn in value, and has identified a number of claims and risk trends that are driving major loss activity in the sector.

Inflation is another key concern for marine insurers and their policyholders as recent increases in the values of ships and cargos mean losses and repairs are becoming more expensive when things go wrong (see Aviation, Marine & Cargo Global Insurance Market Forecasts).

- Fire, collision and sinking, and damaged cargo are the top causes of marine insurance losses by value, according to Allianz Global Corporate & Specialty’s analysis of more than 240,000 claims worth €9.2bn in value.

- Inflation is compounding existing trends driving higher claims severity. Soaring prices for steel and spare parts and rising labor costs are impacting hull repair and machinery breakdown claims.

- Supply chain issues continue to impact claims, as does climate change through extreme weather events and new exposures linked to the net-zero transition.

The number of fires on board large vessels has increased significantly in recent years, with a string of incidents involving cargo, which can easily lead to the total loss of a vessel or environmental damage.

The shipping sector is also having to deal with many other challenges including a growing number of disruptive scenarios, supply chain issues, inflation, time-pressured crew members and employees, increasing losses and damages from extreme weather events, implementing new low-carbon technology and fuels, as well as Russia’s invasion of Ukraine (see Lloyd’s and Insurers Support to EU & UK Govt on Ship Insurance Ban for Russian Oil).

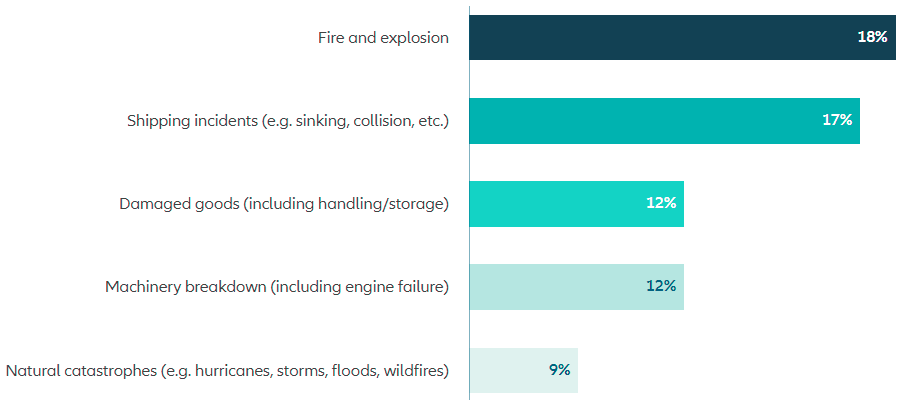

Fires accounted for 18% of the value of marine claims analyzed (equivalent to around €1.65bn) compared with 13% for a five-year period ending July 2018.

A contributing factor to this increase of fire risk on board vessels is often mis-declared/non-declaration (of) dangerous cargos, while a recent increase in engine room fires may reveal some underlying risk around crew competencies.

The potential dangers that the transportation of lithium-ion batteries on vessels pose only add to these concerns, with AGCS having already seen a number of incidents.

Inflation driving up the values of vessels, cargo and repairs in a time of growing exposures

With many countries seeing rates at or around 10%, inflation is compounding existing trends driving higher claims severity. The rising prices of steel, spare parts and labor are all factors in the increasing cost of hull repair and machinery breakdown claims.

The value of both vessels and cargo has been increasing at a time of growing exposures associated with bigger ships, the largest of which can carry 20,000 containers at one time.

The combined value of the global merchant fleet increased 26% to $1.2trn in 2021 while the average value of container shipments has also been rising with more high-value goods such as electronics and pharmaceuticals.

It is not unusual to see one container valued at $50mn or more for high-value pharmaceuticals.

Damaged goods, including cargo, is the top cause of marine insurance claims by frequency, and the third largest by value, the AGCS analysis shows.

The most common claims are physical damage, typically from poor handling, storage and packing. However, recent years have also seen a number of high-value theft and temperature variation claims – the latter can particularly impact pharmaceuticals. Theft is the third most frequent cause of claims with criminals targeting consumer electronics and high-value commodities such as copper.

Cargo is typically stolen from ports, warehouses or during transits. The recent boom in container shipping has also affected cargo claims with a global shortage having resulted in substandard and damaged containers being brought back into use resulting in losses.

The risk of theft and damage to high-value cargos needs to be addressed with additional risk mitigation measures, such as GPS trackers and sensors that provide real-time monitoring on position, temperature, moisture shock, and light and door openings, for example.

At the same time cargo interests need to keep a close eye on insured values. Clients may need to adjust their insurance and policy limits, or risk being underinsured – we have already seen claims for high value container cargos where the cargo interest was underinsured by as much as $20mn.

Risk trends in marine insurance

A number of risk trends in the analysis that are likely to impact loss activity in the marine sector – both today and in the future:

- Sources of disruption continue to increase: Recent years have seen a number of maritime incidents, natural catastrophes, cyber-attacks and the Covid-19 pandemic cause major delays to shipping and ports. Further disruption has also been caused by congestion, labor shortages and constrained container capacity. There are also greater concentrations of cargo risk on board large container vessels and in major ports, so any incident has the potential to simultaneously affect large volumes of cargo and companies.

- Commercial pressures are already a contributing factor in many losses that have resulted from poor decision-making. With the pressure on vessels and crew currently high, the reality is that some may be tempted to ignore issues or take shortcuts, which could result in losses.

- Climate change is increasingly affecting marine claims: Natural catastrophes is already the fifth biggest cause of marine insurance claims, by frequency and severity according to AGCS analysis. Extreme weather was a contributing factor in at least 25% of the 54 total vessel losses reported in 2021 alone, while drought in Europe during 2022 again caused major disruption to shipping on the Rhine. In the US, it dropped inland waterways around the Mississippi River to levels not seen for decades, impacting global transportation of crops such as grain.

- A more sustainable, greener approach in shipping sector is needed, but comes with risks: Efforts to decarbonize the shipping industry, which is a major contributor to global greenhouse gas emissions (GHGs) will also impact claims going forward. Reducing GHGs requires the shipping industry to develop more sustainable forms of propulsion and vessel design and use alternative fuels. As much as the introduction of new technology and working practices is needed to move to a low-carbon world, it can result in unexpected consequences – insurers have already seen a number of machinery breakdown and contaminated fuel claims related to the introduction of low sulfur fuel oil in recent years as part of the move to cut sulfur oxide emissions. Machinery breakdown is already the fourth largest cause of claims by frequency and value.

- Impact of Russia’s invasion of Ukraine: The shipping industry has been affected with the loss of life and vessels in the Black Sea, trapped vessels in blocked Ukrainian harbors and the growing burden of sanctions. Although the signing of the ‘Black Sea Grain’ Initiative in July 2022 enabled some vessels trapped in ports to move out of the conflict zone others remain. The full value of these trapped vessels is unclear, but industry reports have estimated it could be as much as $1bn. Under some marine hull and cargo insurance policies an insured party may be able to claim for a total loss after a specific time has passed since the vessel/cargo became blocked or trapped.

Top causes of claims by value in marine insurance

Based on analysis of 244,451 insurance claims between January 1, 2017, and December 31, 2021, worth approximately €9.2bn in value. “Other” causes of loss account for 32% of the value of all claims. Claims total includes the share of other insurers in addition to AGCS.

Fire is the top cause of claims by value, as Li-ion batteries add a new loss dimension

Fire and explosion has overtaken sinking and collision as the number one cause of marine insurance losses by value over the past five years according to AGCS analysis of more than 240,000 industry claims with an approximate value of €9.2bn. Fires accounted for 18% of the value of marine claims analyzed (equivalent to around €1.65bn) during the period ending December 31, 2021, compared with 13% for a five-year period ending July 2018.

The number of fires on board large vessels has increased significantly in recent years, with a string of incidents involving cargo, which are difficult to extinguish and can easily lead to the total loss of a vessel, tragic loss of life and environmental damage.

A contributing factor is often mis-declared or non-declaration of dangerous cargos, while the International Union of Marine Insurance (IUMI) recently noted an increase in engine room fires which may reveal some underlying risk including crew competencies and modern technologies.

Another notable recent trend has been the threat posed by Li-ion batteries in electric vehicles or cargo that is not stored, handled or transported correctly. Highly inflammable, they have been implicated in a number of car carrier and container ship fires in recent years. A battery fire was reported to have been a contributing factor in the March 2022 sinking of ro-ro carrier Felicity Ace in the Atlantic Ocean, along with its cargo of 4,000 vehicles. In June 2020, a fire on the car carrier Höegh Xiamen in Florida was attributed to a failure to properly disconnect and secure vehicle batteries.

Li-ion batteries have also caused fires in shipping containers, often where shipments have been mis-declared as mobile phone accessories or spare parts. In January 2020, a fire on the container ship Cosco Pacific was attributed to the combustion of a Li-ion battery cargo which was not properly declared. In 2022, the US Coast Guard [5] issued a safety alert about the risk posed by Li-ion batteries following two separate container fires.

Li-ion battery and electric vehicle fires burn more ferociously, are difficult to extinguish, and are capable of spontaneously reigniting hours or even days after they have been put out. Most ships lack the suitable fire protection, firefighting capabilities, and detection systems to tackle these fires at sea, which has been made more difficult by the dramatic increase in ship size.

Given the difficulties involved in extinguishing battery fires at sea companies’ primary focus should be on loss prevention. Measures to consider include ensuring staff/crew receive adequate training and access to appropriate firefighting equipment, improving early detection systems and developing hazard control and emergency plans.

Shipping losses may have more than halved over the past decade (54 total losses (over 100 GT) at the end of 2021 compared to 127 at the end of 2012, according to the AGCS Safety & Shipping Review 2022) but fires on board vessels remain among the biggest safety issues for the industry.

The potential dangers that the transportation of lithium-ion batteries pose if they are not stored or handled correctly only add to these concerns, and we have already seen a number of incidents.

Inflation and exposure growth drive claims severity

With many countries seeing rates at or around 10%, soaring inflation is compounding existing trends driving higher claims severity, including larger vessels and environmental, social and governance (ESG) factors. Higher steel prices, the higher cost of spare parts, and rising labor costs are all impacting the cost of hull repair and machinery breakdown claims.

Incidents such as fires, collisions and groundings are among the top causes of marine insurance claims by value, with a number of costly incidents in recent years.

Accidents involving large container ships and car carriers are particularly expensive, reflecting the accumulation of cargo exposures and challenges in emergency response and salvage. In many cases, a small incident, such as a fire in mis-declared cargo or errors in stability calculations have resulted in a total loss.

In particular higher salvage and wreck removal costs are associated with larger vessels, which require specialist equipment and rely on a limited number of ports of refuge. The ultra-large container ship Ever Given took almost a week to free having blocked the Suez Canal in 2021, while its sister ship the Ever Forward took a month to re-float after it ran aground a year later in Chesapeake Bay in the US. Both incidents were declared General Average, a complex process whereby cargo interests and vessel owners share losses and the costs of salvage.

Salvage costs have also been rising in response to heightened ESG and sustainability concerns, which favor lengthy and expensive wreck removal.

The capsizing of the car carrier Golden Ray in the US in 2019 was one of the costliest shipping incidents in modern times, costing over $1bn, with salvage and wreck removal costs having exceeded $800mn to date.

The wreck removal of the Costa Concordia cruise ship off Italy between 2012 and 2014 cost in the region of $1.3bn while the wreck removal of the Rena, which sank in 2011 off New Zealand cost an estimated $450m. The Rena clean-up operation was not declared complete until April 2016.

Inflation is also adding to the problem of rising values at risk. The value of both vessels and cargos has been increasing at a time of growing exposures associated with larger vessels, which can carry over 20,000 containers at a time.

The surge in demand for shipping has seen the value of vessels increase significantly in recent years. According to Clarkson Research Services, the combined value of the global merchant fleet increased 26% to $1.2trn in 2021, while IUMI also noted that the overall value of insured vessels rose significantly in 2021, driven primarily by the large increase in container ship prices which were up more than 35%, with dry bulk and general cargo vessel values also seeing increases.

The average value of container shipments has also been increasing with inflation and an increase in the shipping of high value goods like electronics and pharmaceuticals.

We see more high value goods being shipped by container, while the average cost of goods rises with inflation. It is not unusual to see one container valued at $50mn or more for high value cargos like pharmaceuticals.

These high value cargos need additional risk mitigation measures, such as GPS trackers and sensors that provide real time monitoring on temperature, moisture shock, and light and door openings, for example.

At the same time cargo interests need to keep a close eye on insured values. Clients may need to adjust their insurance and policy limits, or risk being underinsured – we have already seen claims for high value container cargos where the cargo interest was underinsured by as much as $20mn.

Cargo insurance claims continue to rise

Damaged goods, including cargo handling and storage, is the top cause of marine insurance claims by frequency, and the third largest by value over the past five years, according to the AGCS analysis. The most common claims continue to be physical damage to cargo, typically from poor cargo handling, storage and packing. But recent years have also seen a number of high-value theft and temperature variation claims. Interestingly, crime and theft are the third most frequent cause of marine insurance claims during the same time period.

Criminal gangs are targeting consumer electronics and high-value commodities like copper. Cargos are typically stolen from ports, warehouses or during transit, falling victim to armed robbery or fake handling agents.

Latin America is a hot spot for cargo theft, although there have also been large claims in Europe. In 2020, criminals using insider knowledge stole a cargo of mobile phones valued at €3mn from Schiphol, just one of three major thefts at the Netherlands-based airport that year.

The insurance market has also paid some large temperature variation and fire claims involving pharmaceutical shipments.

Cargo values have risen noticeably in the past year. We recently saw a truck fire loss involving a cargo valued at $73mn from just one transportation. This is a concerning trend for marine underwriters.

The recent boom in container shipping, which puts cargo handling and port turn-around under pressure, has also affected cargo claims. A global shortage of shipping containers has resulted in substandard and damaged containers being bought back into use, while a deterioration in the economic environment and the higher cost of living could have implications for future theft and civil unrest claims.

Supply chain exposures and disruption continue to impact

Recent years have highlighted large supply chain disruption exposures in the shipping industry, as a number of maritime incidents, natural catastrophes, cyber-attacks and the Covid-19 pandemic have caused major delays to shipping and ports. Further disruption has also been caused by congestion, labor shortages and constrained container capacity.

The trend for larger ships is also helping increase supply chain exposures. Larger vessels, while more efficient, require port infrastructure and logistical support that is more complex and specialist than traditional shipping.

There are also greater concentrations of cargo risk on board large container vessels and in major ports, so any incident has the potential to simultaneously affect large volumes of cargo and companies. Ports are also increasingly reliant on technology, where an outage or cyber-attack could effectively close a port. Commercial pressures are already a contributing factor in many losses that resulted from poor decision-making.

The pressure on vessels and crew is currently very high. The reality is that some may be tempted to ignore issues or take shortcuts, which could result in future losses.

Risk managers must take these factors into account and take a more risk managed approach to the shipping aspect of supply chains. In the past, companies have not paid enough attention to cargo risks and exposure accumulation.

Companies need to start treating cargo risks more like property assets, tracking and monitoring exposures, and taking a more proactive approach to protecting them.

In addition to improving the transparency of cargo exposures, companies should challenge freight forwarders on the risks, such as the quality of the vessel, loading and operation. They can also seek help from insurers who can provide risk improvement advice on ways to prevent cargo damage losses and reduce accumulations.

Events over the past year have demonstrated just how fragile and interconnected global supply chains are, and the critical role played by the shipping industry. It is essential that companies understand their accumulations and consider ways in which they can minimize exposure to major events.

Climate-risks contribute to claims

Climate change will increasingly affect marine insurance claims, with more extreme weather events and with new exposures linked to the transition to net-zero.

Natural catastrophes were already the fifth biggest cause of marine insurance claims, by frequency and severity for the five-year period ending December 2021.

Extreme weather and natural hazards have contributed to a number of large losses in the past, with the loss of vessels and damage to cargos – extreme weather was a contributing factor in at least 25% of the total vessel losses reported in 2021 alone.

In addition, drought in Europe during 2022 again caused major disruption to shipping on the Rhine, preventing many vessels from navigating this critical European shipping route fully loaded. Meanwhile, in the US, many barges were reported to have run aground on the lower Mississippi River as drought dropped inland waterways to levels not seen for decades, impacting one of the most cost-efficient means of getting commodity crops such as grain into the global market.

Weather has also been a factor in a recent increase in the number of containers lost at sea, as heavy seas exert huge forces on large container vessels and container lashings.

According to the World Shipping Council, the annual average number of containers lost at sea has increased 18% over the past 14 years to 1,629 in 2021. The average losses for the two-year period 2020-2021 alone were 3,113 compared to 779 in the previous period.

Efforts to decarbonize the shipping industry will also impact marine claims going forward. With 90% of international trade moved by sea, shipping is currently a major contributor to global greenhouse gas emissions.

The International Maritime Organization (IMO) is working towards a 40% cut in greenhouse gas emissions across the global fleet by 2030, and at least a 50% cut by 2050.

Reducing greenhouse gas emissions will require the shipping industry to develop more sustainable forms of propulsion and vessel design. A key risk factor in the transition will be the adoption of alternative fuels, which could include liquefied natural gas, green hydrogen and methanol, as well as electric- and wind-powered assisted vessels.

The introduction of new technology and working practices can, however, result in new risks or unexpected consequences. Machinery breakdown is already a significant source of marine insurance claims – it is the fourth largest cause by frequency and value over the past five years.

The insurance industry has already seen a number of machinery breakdown and contaminated fuel claims related to the introduction of low sulfur fuel oil under IMO 2020, which was introduced to cut sulfur oxide emissions, as marine fuels and bunkering has become more complex.

The shift to greener energy sources is already giving rise to new claims scenarios. In 2022, drifting bulk carrier Julietta D collided with an offshore wind turbine foundation and transformer station in the Hollandse Kust Zuid windfarm, having previously collided with the tanker Pechora Star after its anchor gave way in a storm.

With 2,500 wind turbines due to be installed on the North Sea before 2030, the risk of a ship to turbine collision is estimated at 1.5 to 2.5 times a year, according to the Maritime Research Institute Netherlands (MARIN).

Ukraine invasion impact

Russia’s invasion of Ukraine has caused widespread disruption to global shipping, exacerbating ongoing supply disruption, port congestion and crew crises caused by the Covid-19 pandemic.

The industry has been affected on multiple fronts with the loss of life and vessels in the Black Sea, disruption to trade with Russia and Ukraine, trapped vessels and the growing burden of sanctions.

At the start of the conflict in February 2022, approximately 2,000 seafarers were stranded aboard vessels in Ukranian ports. Trapped crews faced the constant threat of attacks with little access to food or medical supplies, with a number being tragically killed. More than 100 ships were still trapped in Ukrainian ports as of May, many without crew.

There have been some positive developments with the signing of the ‘Black Sea Grain Initiative’, which has enabled a large volume of grain and fertilizer to be shipped out from key ports in Ukraine.

As a result of this initiative some vessels trapped in these ports have also moved out of the conflict zone but tankers and other vessels not carrying grain or fertilizer did not benefit.

Depending on policy terms and conditions, ‘blocking and trapping’ coverage can be included in some marine hull and cargo insurance policies.

Under this clause an insured party may be able to claim for a total loss after a specific time (generally 180 days for cargo and 12 months for hull) has passed since the vessel/cargo became blocked or trapped. From an AGCS perspective, we have already seen claims for cargo losses but are yet to see claims from trapped hulls, as many will not materialise until during the first quarter of 2023.

Abandoned vessels and vessels laid up without any crew onboard will see further deterioration in their condition with the costs associated with recommissioning them rising the longer they remain trapped. In some cases the growing recommissioning and repair costs may lead to a constructive total loss.

Commodities like sunflower oils which remain onboard any trapped vessels will suffer continued degradation leading to reduction in salvable quantity and value. Ultimately, the longer any vessels and cargos are trapped, the more difficult and expensive the salvage solutions will be.

………………………..

AUTHORS: Régis Broudin – Global Head of Marine Claims at AGCS, Captain Rahul Khanna – Global Head of Marine Risk Consulting at AGCS