Overview

Insurtech funding in Latin America hit a historic low of $26 mn in the first half of 2024, a 78% drop from the same period in 2023, according to Digital Insurance LATAM, representing a 2% growth compared to the previous year. From July 2023 to June 2024, total funding reached $43 mn, the lowest on record.

According to McKinsey, the insurance sector in Latin America is a fertile ground for accelerated growth and innovations in business models. Additionally, the consultancy states that it is the fastest-growing region globally in the insurance sector.

As of now, there are 498 insurtechs in Latin America. They are estimated to represent 7% of the global insurtech ecosystem but currently account for less than 1% of total funding

Despite limited funding, the insurtech ecosystem in Latin America remains resilient. The mortality rate among startups dropped from 13% to 10%, with Argentina showing a 6% improvement, according to Global InsurTech Funding report.

Initiatives like the Pacific Insurtech Alliance and other associations aim to co-create the future of insurance, connecting innovative startups with traditional stakeholders, including major insurers in Latin America.

Key Highlights: State of Insurtech in Latin America

- H1 2024 insurtech funding reached a historic low of $26 mn., a 78% decline compared to H1 2023.

- Startup Mortality Rate decreased from 13% to 10%. Argentina showed significant improvement with a 6% rebound.

- Ecosystem Expansion grew by 6%, now totaling 498 startups. Organic growth reached over 16% in the past year with 77 new ventures.

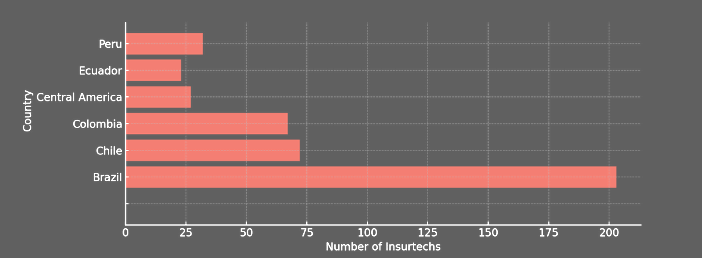

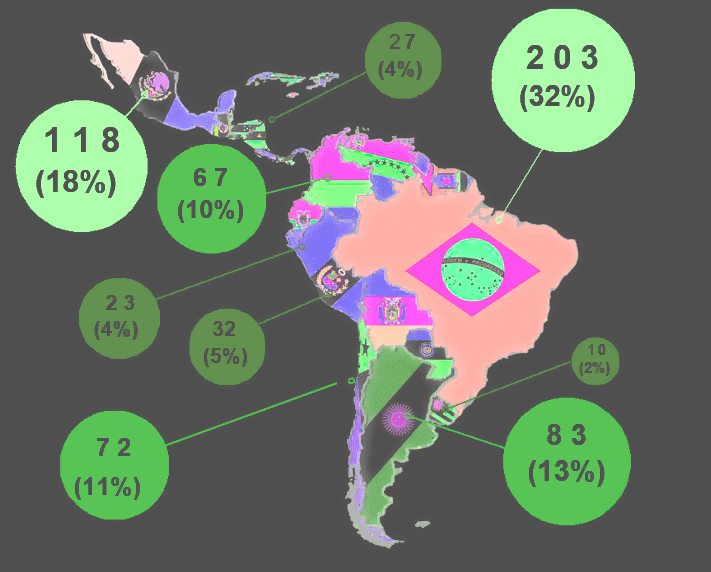

- Brazil leads with 203 startups, Chile follows with 72 startups, and Colombia with 67.

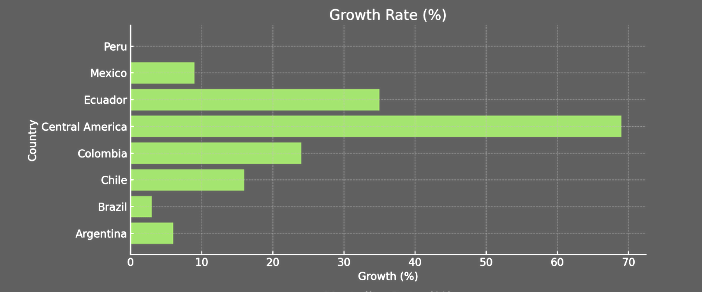

- Central America saw 69% growth, Ecuador (35%), Colombia (24%), and Peru (23%).

- 53% of insurtechs focus on distribution (a 6% decline from 2020).

- Despite a 10% disappearance rate among insurtechs, the ecosystem grows by +6%, reaching 498 insurtechs.

Insurtech market in Latin America overview

Annual growth has risen to 6%, but there may still be “zombies” among the 498 insurtechs. The annual mortality rate dropped to 10%, with 49 insurtechs disappearing over the past year (see Top-Performing Insurance and InsurTech Stocks).

Organic growth stands at 16%, with 77 new or pivoted insurtechs in the last year. Investment has plummeted to $26 mn, a 78% decrease compared to the first half of 2023.

Over the past year, only $43 mn was invested, the lowest annual amount in history, despite 6% growth. Insurtechs in Latin America are in high demand, driven by significant entrepreneurial energy. International expansion continues to grow at 11%, with a 14% internationalization rate.

Insurtech ecosystem in LatAm growth rate

Latin American countries attract foreign insurtechs, especially Mexico, Colombia, and Peru, with an attraction index of 24%, up 35% in one year. About 53% of insurtechs focus on digital distribution, including full-stack insurtechs, while 47% collaborate with (re)insurers and intermediaries (see Global Landscape of Insurance Digital Transformation).

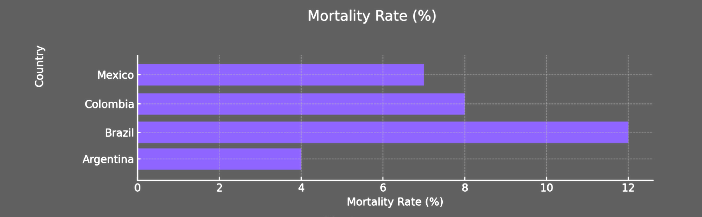

In Argentina, the ecosystem grew by 6%, with the mortality rate dropping from 15% to 4%, showing reactivated entrepreneurship.

Brazil, despite a 12% mortality rate, recorded 3% growth, reaching 203 insurtechs. Chile’s ecosystem grew by 16%, reaching 72 insurtechs, with a high internationalization rate of 30%.

Colombia’s ecosystem expanded by 24%, now hosting 67 insurtechs, thanks to a low mortality rate of 8% and strong ecosystem collaboration. Colombia is becoming a regional hub, with 43% of its insurtechs being foreign.

Central America, with 27 insurtechs and 69% growth, is emerging as a new innovation hub. Its proximity to AIM enhances its development. Ecuador’s new ecosystem, with 23 insurtechs, benefits from its proximity to active markets like Peru and Colombia, sustaining a 35% growth rate and a 48% attraction rate.

Mexico has a 7% mortality rate among local companies, slowing its growth to 9%, but it remains an attractive market with a 31% attraction index. Peru, with 32 insurtechs, has record attraction rates of 63% and internationalization rates of 42%, making it the most open country in the region.

Mortality rate for insurtech startups

The annual mortality rate for insurtech startups in Latin America is 10%, with 49 closures in the past year.

92% were locally-based startups, highlighting the critical role of multilatinas in business survival.

Brazil has the highest mortality rate at 12%, while Argentina and Colombia improved to 4% and 7%, respectively.

Insurtech ecosystem in LatAm mortality rate

Venture capital in the insurtech ecosystem

Despite the downturn in venture capital, the insurtech ecosystem in the region grew by 6%, now totaling 498 startups. Considering a 10% mortality rate, organic growth reached over 16% in the past year, with 77 new ventures.

Brazil leads with 203 startups, followed by Chile with 72, and Colombia with 67.

The Pacific region shows the highest growth: Central America (69%), Ecuador (35%), Colombia (24%), and Peru (23%).

Number of insurtechs in various countries

Digital insurance was the first wave. Companies in the sector overcome risk aversion and traditional processes and channels to embrace digital platforms and offer their services online.

Insurtechs played a decisive role in this transition, targeting the sector’s weaknesses—meeting customer needs in a few clicks and saving them from paper forms, complex bureaucratic procedures, and trips to offices.

Customer experience standards have been raised, and specific improvements in efficiency and sustainability have been achieved.

However, there is still potential for growth. It is important to mention that Latin America has experienced several cases where Insurtechs and insurers have successfully gained value from the first wave of Insurtech.

Insurtech geography and international expansion

The ecosystem grows by +6% annually, reaching 498 insurtechs. Considering a mortality rate of 10%, the “gross” growth is +16%.

The “Pacific” region drives the continent with Peru (+23%), Colombia (+24%), Ecuador (+35%), and Central America (+69%).

In the past year, 77 new insurtechs emerged in LATAM, while 49 shut down.

Argentina saw a 6% increase, with a lower mortality rate of 4%. Brazil grew by 3%, reaching 203 insurtechs, with 47 closures, and now includes 4 neoinsurers.

Chile experienced robust growth of 16%, with new local players like MueveSeguro, ProteusCargo, and Yapp.

Colombia maintained a steady growth of 24%, attracting foreign insurtechs such as Airbag, Ole, and Dacadoo. Peru grew by 23%, now with 32 insurtechs, though still without partnerships.

Ecuador showed strong dynamism with a 35% increase, and Central America led with a 63% rise. Mexico, growing by 9%, has become a hub attracting insurtechs from both Latin America and Europe, including Qantev.

International expansion grew by 11% in the first half of 2024, with an internationalization index of 13.4%.

Multilatina insurtech startups, operating in multiple countries, represent 13% of the market.

Peru (42%) and Chile (30%) drive this expansion due to business scalability, while Brazil exports very few insurtechs (<1%) due to unique market dynamics.

About 53% of insurtechs in the region focus on distribution, a 6% decline from 2020. Despite this, distribution remains dominant, though the ecosystem is exploring other business models.

LatAm insurtechs’ specializations

Most distributors specialize in personal lines like auto and home insurance, with Broker and Managing General Agent (MGA) models comprising 42%.

Enablers increased by 6 percentage points over the past four years, now making up 47% of the Latin American insurtech ecosystem.

Latin American entrepreneurs remain committed to fostering new startups despite limited investment. The region is resilient and attractive to both local and international investors.

2024 began with almost no funding in the insurtech sector.

Investments totaled only $26 million, marking a 78% drop compared to the first half of 2023. Over the past 12 months, total investments barely reached $43 million, a historic low.

Can the ecosystem grow without funding? Intuitively, the answer seems to be ‘no’. Yet, a paradoxical 6% growth has been observed.

For the rest of 2024, projections indicate a 62% reduction in investment compared to the previous year.

The total estimated investment in insurtech stands at $1.196 billion, with Brazil (61%) and Chile (23%) being the main contributors.

Despite the low volume, Brazil accounts for 47% of total investment in 2024, while Mexico represents 27%. Chile has not seen significant new funding.

The largest investments of the year:

- Loovi ($9 million): Exited the Brazilian sandbox, neoinsurer for auto insurance.

- Welbe ($7 million): Series A funding for this Mexican healthcare platform managing occupational health and organizational well-being.

- Sostengo ($4.8 million): The first insurtech in Central America, offering a fully digital auto insurance solution, originated in El Salvador.

- Osigu ($1.7 million): Platform for managing the health insurance ecosystem in Latin America.

- BlueCyber ($1.5 million): Simplified cyber insurance for SMEs, focusing on Brazil, using an MGA model.

- Lina ($1.5 million): Brazilian provider of technology for data exchange and services in Open Insurance.

The mobility ecosystem leads the insurtech sector with 201 companies, representing 40% of the total. Within this ecosystem, distribution is dominant, making up 69%, while enablers constitute 31%.

Investment in this ecosystem has been substantial, attracting 36% of the total investment over the past decade, amounting to $435 mn.

This funding primarily supports mobility neoinsurers, who need significant initial capital.

Neoinsurers hold a relevant position at 7%, with examples like Momento in Mexico and Pier in Brazil. Brokers constitute 38%, including Compara in Chile and Acto in Mexico. Telematics is notable, representing 9%, with companies like Jooycar and Cobli.

Fraud detection, despite its high cost of about 10% of the premium, accounts for only 4% of the ecosystem (Shift, Autoinspector). A new trend in Latin America is transportation insurance, with insurtechs like Zuru, ProtegeTuCarga, and Vertech leading the way.

We clarify that we do not have the ambition to issue a value judgment on the quality of the contribution to the transformation of the insurance sector, but rather to try to objectively define what an insurtech is based on its own definition.

Defining insurtechs also means playing the role of the “gorilla at the door of the nightclub”, and unfortunately, this intrinsic score mentioned previously excludes some companies or ventures that define themselves as Insurtechs.

……………….

AUTHOR: Hugues Bertin – CEO and Founder of Digital Insurance LATAM, Carlos Cendra – Scouting & Investment Lead at MAPFRE Open Innovation