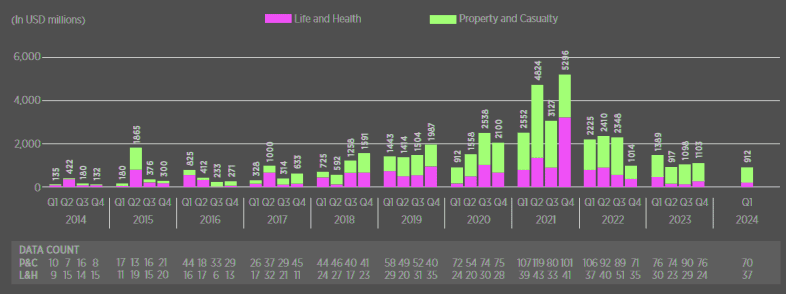

Global InsurTech funding fell to USD912.25 million in Q1’2024, the lowest since Q1’2020. The industry saw no quarterly USD100 million+ mega-round deals for the first time since Q3’2017. Property & Casualty InsurTechs raised USD605.58 million in Q1’2024, a low not seen since Q3’2018. Early-stage InsurTech funding increased 26.5% quarter on quarter, countering the broader InsurTech funding picture.

According to Gallagher Re InsurTech reports, over a quarter of Q1’2024 deals went to AI-centered InsurTechs. Half of Q1’2024 deals went to distribution-focused InsurTechs. The majority of tech investments from (re)insurers were early-stage. Quarterly global InsurTech funding fell to the lowest level since Q1’2020, decreasing 17.3% quarter on quarter.

Global InsurTech funding dipped below USD1B in Q1’2024, falling from USD1.103B in Q4’2023 to USD912.25M in Q1’2024. The decrease was largely attributable to an absence of USD100M+ mega-round InsurTech deals for the first time since Q3’2017.

In the first quarter of 2024, InsurTech deal activity rose by 7% from the previous quarter, with transactions increasing from 100 to 107 (see Top-Performing Insurance and InsurTech Stocks). This growth continues a trend noted in earlier reports, where interest in the sector remains strong, although the average investment per deal is decreasing.

Global InsurTech funding

The average deal size experienced a significant reduction of 30.6%, decreasing from USD 14.14 million in the fourth quarter of 2023 to USD 9.81 million in the first quarter of 2024.

This marks the first time since the third quarter of 2017 that the average global InsurTech deal size has fallen below USD 10 million, according to Global Landscape of Insurance Digital Transformation.

P&C InsurTech funding also declined, dropping 22.5% to USD 605.58 million in the first quarter of 2024, the lowest since the third quarter of 2018.

The average deal size in this category reached its lowest point since the first quarter of 2018 at USD 10.09 million, and the total number of deals decreased to 70, a reduction of six deals from the previous quarter.

This decrease primarily resulted from fewer transactions in the categories of lead generation, brokerage, and managing general agents (MGA).

Funding for Life & Health (L&H) InsurTech remained relatively stable, decreasing only slightly by 4.7% to USD 306.67 million.

Annual InsurTech funding volume and transaction count

InsurTech by the Numbers

The number of deals in this sector increased dramatically by 54.2%, rising from 24 in the last quarter of 2023 to 37 in the first quarter of 2024.

Despite the increase in the number of transactions, the average deal size in L&H InsurTech fell by 39.38% to USD 9.29 million.

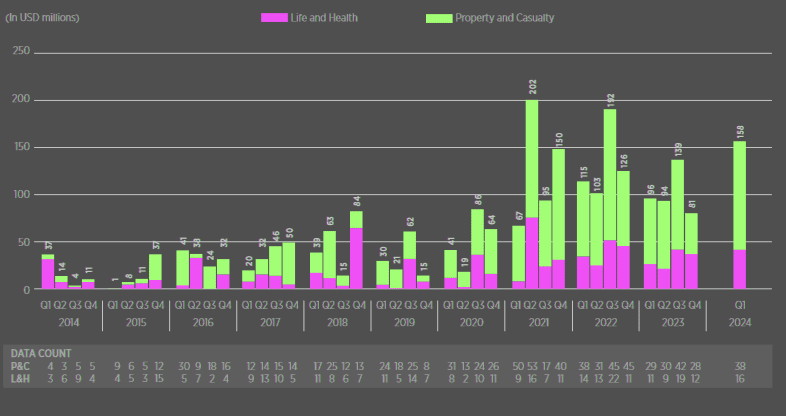

Funding for early-stage InsurTech surged by 26.5% from the fourth quarter of 2023 to the first quarter of 2024, reaching a total of USD 280 million.

This growth spanned both Property & Casualty (P&C) and Life & Health (L&H) sectors, which saw increases of 16.8% and 66.9% respectively (see How InsurTech Can Optimize Pet Insurance Industry?).

Quarterly InsurTech Funding Volume — All Stages

Quarterly InsurTech Funding Volume — Early-stage Incubation

The average deal size for early-stage InsurTech also rose from USD 4.43 million in the last quarter of 2023 to USD 4.83 million in the first quarter of 2024. The number of deals increased from 58 in the fourth quarter of 2023 to 64 in the subsequent quarter, largely due to a rise in Seed/Angel investments from 36 to 45.

AI-focused InsurTechs commanded 28% of the deal flow in the first quarter of 2024, emphasizing the importance of artificial intelligence in the sector.

These AI-centric companies secured USD 316.06 million in funding. Notably, the largest deal of the quarter was a USD 73 million Series B funding round for Hyperexponential, an AI-driven pricing platform.

Quarterly InsurTech Transactions by Target Country

Quarterly InsurTech Transactions by Investment Stage

Out of 30 AI-focused deals, 16 involved early-stage companies, which secured higher average deal sizes of USD 6.06 million, compared to USD 3.81 million for their non-AI counterparts. Despite this, the overall average deal size for AI-centered InsurTechs was only marginally higher at USD 10.53 million than the overall average for the quarter.

InsurTech deals went to distribution-focused startups

The use of AI in distribution and sales is the particular focus of our Q1 report, so it is notable that 54 of the 107 Q1’2024 InsurTech deals went to distribution-focused InsurTechs. These companies raised a collective USD528.22 million in Q1’2024.

The average deal size (USD9.78 million) among this group was nearly equal to the overall average InsurTech deal size.

11 of the deals went to InsurTechs focused on embedded or white-label insurance distribution. This group included the second-largest deal of the quarter – a USD54M Series C deal to ELEMENT, a P&C-focused embedded insurer. 32 of the 54 companies are intermediaries that sell insurance. Just 5 of the 54 distribution-focused InsurTechs are AI-centered.

The use of data in AI

The single biggest issue is the quality of the data – most available data is either poor quality, can lead to biased outcomes, or is just incorrect. For example, approximately 80% of available text on the internet is voluntarily inputted/created, so the potential for error seems high.

The majority of tech investments from (re)insurers were early-stage

Q1’2024 saw 37 tech investments from (re)insurers. 54.1% of these investments were directed toward US-based companies. Early-stage investments comprised the majority (62.2%) of investments.

Investment from accelerators, incubators, business-plan competitions, and economic development entities are excluded.

As such, there are some deals that might constitute a raise in other circumstances that we do not consider in our data.

The numbers and data we do present should be considered a minimum benchmark – e.g. this quarter at least USD912.25M was raised. This is the same consistent set of metrics that we have used since our first publication in April 2017.

Role of AI in the insurance industry

The insurance industry has seen varying degrees of success with technological integration. While some efforts have achieved significant progress, others are ongoing. To date, the global investment in InsurTech totals around $55 billion. The value of this investment varies depending on perspective.

Consumers have generally appreciated the gradual digital transformation within the industry, even though operational costs for insurers and reinsurers have not decreased. Nevertheless, these technological advancements have enhanced processes.

Ignoring technological advancements is not a feasible option. Despite the costs, maintaining industry relevance is crucial, and embracing technology through InsurTech is essential, not optional.

The industry continues to derive value from technology investments, and it is expected that a pivotal moment will eventually validate these efforts.

The 2023 InsurTech reports note a shift from uncontrolled growth to a new phase focusing on profitability, which should further support the industry’s technological transformation.

As analytics have always maintained, technology in isolation (from a concrete use case) is effectively meaningless.

It is a way to do something – whether to speed a process up, or reduce manual entry of something else, the fact remains that technology is a how, not a what. If we were to ask Jeff Bezos about Amazon, he would probably tell us it’s a fast, cheap, convenient way to get goods to your doorstep – not that it is cloud-based, and powered by tech.

AI is challenging this view of technology

Artificial Intelligence is challenging this view of technology. Existing commercial AIs come to life when they have been trained on a data set, or a data model, and as a result they generally have a business focus embedded into the nuts and bolts of the technology itself.

This form of AI can never really exist “in isolation” – it is born with a targeted function.

2023 felt like a pivotal year, in which AI began to be taken seriously among mainstream business audiences for the first time – not just because of its growing prevalence, but also because of the tangible results it was producing.

This has included specific use-cases in traditional (re)insurance processes – claims fraud detection, for example.

The data challenge for (re)insurers

All forms of artificial intelligence (AI) inherently carry biases from their creators, a challenge that extends even to advanced self-aware or theory of mind AIs.

This issue is particularly pronounced in self-learning AI systems, where the training data chosen by creators or users amplifies existing biases. It is crucial to scrutinize the data used to train these algorithms and their models diligently.

Without such scrutiny, AI models may become increasingly narrow, merely echoing societal biases—a challenge recognized by major players like Google.

In February 2024, Google’s CEO, Sundar Pichai, acknowledged that their AI product, Gemini, had demonstrated bias and offended users.

The expansion of AI tools raises significant ethical and regulatory issues, particularly in the insurance sector. Although it is not our role to dictate AI regulations, many insurance bodies are beginning to restrict AI’s use until there is a clearer understanding of the data training these models.

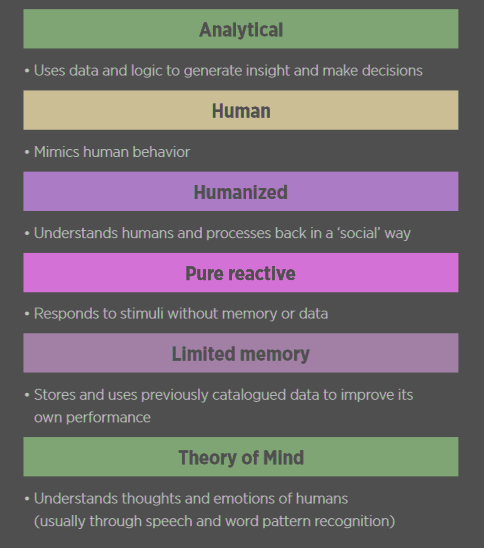

Types of AI output

Some insurers have even opted out of using AI for this reason. InsurTech companies that use AI stand to greatly assist the industry in navigating these complexities.

The term “AI” is often used loosely, leading to confusion and challenges in technology adoption and company differentiation within the industry.

Generative AI – where the money is

To begin with, we should acknowledge that one AI product in particular has captured the imagination of the public – and the wallets of investors – in recent months. This is generative AI, a growing subfield of artificial intelligence that uses computer algorithms to generate outputs that resemble human-created content, such as text, images, graphics, music and computer code.

Generative AI models learn the patterns and structure of their input training data, and then generate new data that has similar characteristics.

Investors are increasingly drawn to the artificial intelligence sector. Goldman Sachs reports that investments in AI companies and tools have reached approximately $200 billion. In particular, 2023 marked a significant year for generative AI, attracting $21.8 billion in less than a year.

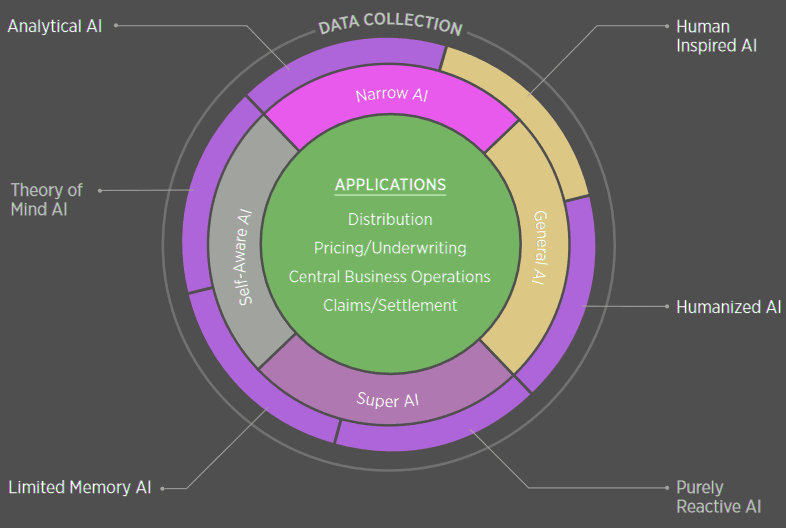

A framework for selecting AI tools

Notable companies such as OpenAI, Inflection AI, Anthropic, Databricks, and recently Aleph Alpha, have secured substantial funding.

A majority of these investments (67%) were directed towards early-stage funding rounds, indicating that the industry is still in its nascent stages.

The primary focus of investments is the development and maintenance of large language models (LLMs), which require considerable financial resources.

Aleph Alpha, a developer of LLMs, secured the largest corporate venture capital-backed deal of 2024, raising $500 million in a Series B round.

In the reinsurance industry, the most effective application of generative LLMs has been in processing unstructured data. These models are adept at extracting and consolidating information from diverse external sources into standardized categories, enabling more efficient data analysis.

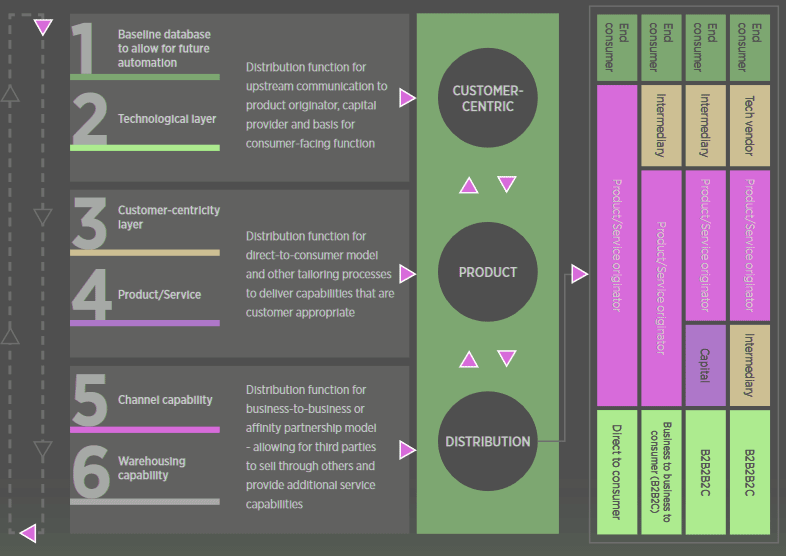

The customer-centric tech distribution model

According to data from Slipcase, one of the insurance industry’s leading information distribution & analytics platform, in 2022 8% of clicks on content tagged as Technology were on items with AI mentioned in the headline.

In 2023, this value shot up to 46%. Almost half all technology clicks in 2023 were AI-related. Slipcase also noted a rise in InsurTech, which went from 2% to 18%.

Historically, the most common means of distribution for (re)insurance products and services is through (re)insurance intermediaries.

Whether it be an agent (representing one or multiple insurers) or a broker (representing a policyholder or a collective of policyholders), these traditional intermediaries serve as a critical link between risk and capital — helping to ensure the correct coverage is provided, at the right price, for the right requirement(s).

Brokers and agents not only offer advice to discuss appropriate coverage, but they are also expert at negotiations.

Consequently, the relationship itself is a very human one (it is extremely difficult to negotiate with technology), and the most appropriate technology in this space supports brokers and agents as humans. Price discovery, instantaneous price comparisons, digital procurements, remote binding and issuing of contracts are all areas where we have seen technology play a huge part in evolving the role of human intermediaries.

…………..

AUTHOR: Dr. Andrew Johnston – Global Head of Gallagher Re, Irina Heckmeier – Global InsurTech Report Data Director Gallagher Re, Freddie Scarratt – Deputy Global Head, InsurTech Gallagher Re, Brea White – Global InsurTech Report Content Coordinator Gallagher Re