Aon reported Q3 2025 net income attributable to shareholders of $458 mn, up from $343 mn a year earlier, driven by organic growth and revenue gains across all business units.

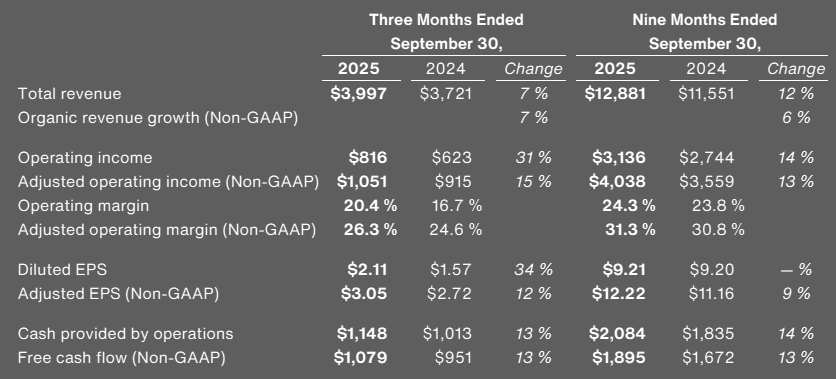

Total revenue climbed 7% to $4 bn, reflecting both organic expansion and favorable foreign currency moves. Each of Aon’s major segments posted growth, extending the company’s recent streak of consistent quarterly gains.

The commercial risk solutions segment grew 7% organically, boosted by double-digit property and casualty growth in the United States and stronger middle-market demand. The reinsurance business saw revenue rise 8%, powered by new business and steady client retention.

Health solutions revenue increased 6%, supported by solid performance in the core benefits line and favorable market dynamics. The wealth solutions segment rose 5%, helped by ongoing regulatory consulting projects and expansion in investment advisory services.

CEO Greg Case said Aon continues to invest aggressively in data analytics and capital strategy.

Our Aon United strategy, accelerated through our 3×3 Plan, is delivering strong results. We are attracting top talent in high-growth areas, scaling our data analytics across our core Risk Capital and Human Capital businesses, expanding in the middle market and unlocking new sources of capital

Greg Case president and CEO

“We are executing with discipline and increasing the value we deliver to our clients – winning in existing markets, creating demand in emerging areas and innovating unique capital solutions,” said Greg Case.”

“Our strong capital position, fueled by robust cash generation and disciplined portfolio management, enables us to execute our capital allocation model – balancing high-return investment for future growth and capital return to shareholders,” Case added.

“We remain confident in achieving our full-year 2025 financial targets and are well positioned to deliver sustainable growth in 2026 and beyond.”

Operating expenses reached $3.2 bn, up 3% year over year, tied to higher costs linked to organic growth.

We think Aon’s quarter shows the payoff from its focused scaling strategy – disciplined cost control, tech-driven advisory strength, and deeper traction in mid-market segments where competition keeps heating up.

Aon plc posted a sharp jump in third-quarter earnings, with net income attributable to shareholders up 34% to $2.11 per diluted share, compared with $1.57 a year earlier. Adjusted EPS increased 12% to $3.05 from $2.72, supported by broad-based organic growth across both its Risk and Human Capital segments.

Total revenue rose 7% year over year to $4 bn, reflecting 7% organic growth and a 1% boost from favorable foreign currency translation, partly offset by a 1% drag from acquisitions and divestitures.

Risk Capital revenue climbed $170 mn, or 7%, to $2.5 bn, while Human Capital revenue rose $106 mn, or 8%, to $1.5 bn.

Operating expenses increased 3% to $3.2 bn, primarily reflecting costs tied to organic expansion and currency effects.

Those increases were partially offset by lower spending from the Accelerating Aon United initiative, $35 mn in restructuring savings, and reduced integration costs tied to the NFP acquisition. Risk Capital expenses rose 8% to $1.9 bn, while Human Capital expenses fell 2% to $1.1 bn.

Aon reported an effective tax rate of 21.3%, up from 20.9% a year earlier. The adjusted tax rate stood at 19.2% versus 18.0%, driven by shifts in income geography and fewer discrete tax benefits.

Weighted average diluted shares declined to 216.7 mn, down from 218.4 mn last year, after Aon repurchased 0.7 mn shares for about $250 mn during the quarter.

The company still had $1.6 bn remaining under its share repurchase authorization as of September 30, 2025.

Currency movements had minimal effect on results. Aon said if exchange rates stay stable, the full-year EPS impact should remain negligible.

For the 9 months of 2025, operating cash flow climbed 14% to $2.1 bn, thanks to higher adjusted operating income and lower NFP-related transaction costs.

Free cash flow rose 13% to $1.9 bn, reflecting stronger operational performance and only modest capital spending increases.

The quarter underscores Aon’s steady operating rhythm – disciplined cost control, double-digit EPS growth, and a capital allocation strategy still leaning heavily toward buybacks over M&A. Investors seem to like that balance, even in a tight global risk market.