M&A activity in the European financial afn insurance services industry rebounded in the first half of 2025 after a slow, according to EY’s analysis. However, the activity remains subdued.

The number of publicly disclosed financial services deals across Europe rose by 38% compared to the previous six months, yet it declined by 3% year-on-year.

The total M&A value decreased from €23.8bn to €17.1bn in H1 2025, despite three deals exceeding €1bn each. A potential large deal in Spain could significantly increase deal value in the second half of this year.

European banks, insurers, and asset managers disclosed 367 deals between January and July 2025, compared to 380 in H1 2023 and 265 in H2 2023.

European firms acquiring targets from other markets rose from 24 to 32 in H1 2024, but the total disclosed value fell from €1.9bn to €1bn.

M&A activity across Europe’s financial markets

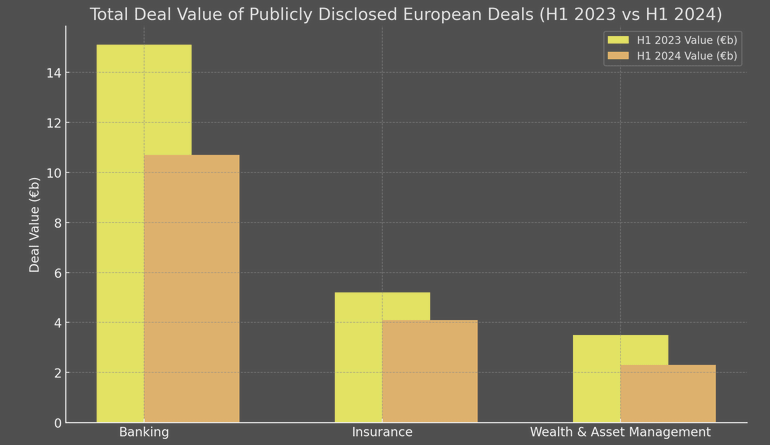

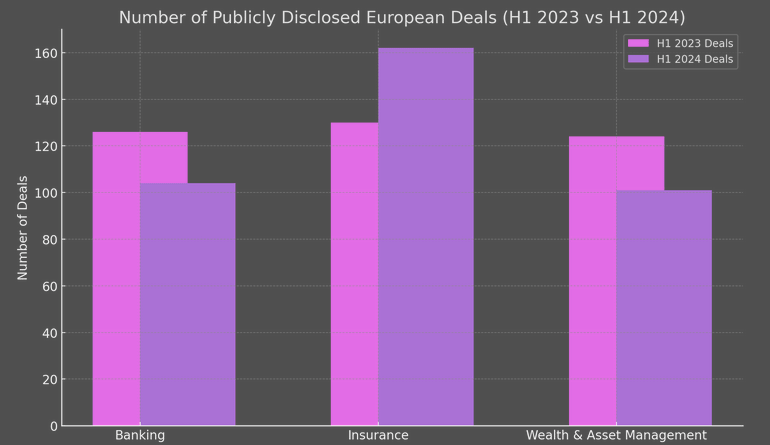

- The number of publicly disclosed European banking deals fell from 126 o 104 deals in H1 2024, and the sector reported a fall in deal value, from €15.1b to €10.7b in H1 2024.

- The number of publicly disclosed European insurance companies deals increased from 130 to 162 in H1 2024, but the overall disclosed deal value decreased from €5.2b to €4.1b in H1 2024.

- The number of publicly disclosed European wealth and asset managementdeals fell from 124 deals to 101 deals in H1 2024, resulting in a year-on-year fall in value, from €3.5b to €2.3b in H1 2024.

M&A Deal Value and Number of European Deals

Non-European firms acquiring European targets increased from 41 to 52 in H1 2024, though the total disclosed deal value dropped from €3.2bn to €1.4bn.

Europe’s macroeconomic environment, marked by high interest rates, inflation, and geopolitical risks, continues to challenge firms and affect deal activity

Benoit Gérard, EMEIA Financial Services Strategy and Transactions Leader at EY

Nonetheless, the first half of this year showed improvement over the previous six months.

He analized the importance of a long-term perspective, noting that as Europe’s economies recover and market confidence rises with expected interest rate decreases, optimism is gradually increasing.

2024 M&A Activity Trends

This analysis highlights the cautious optimism in the European financial and insurance sectors, with potential for increased M&A activity contingent on economic conditions and market confidence.

- Overall M&A Activity:

- Increase: After a slow second half of 2023, M&A activity in European financial services picked up in H1 2024.

- Moderate Growth: Despite the increase in activity, the overall number of deals and total value remain subdued.

- Banking Sector:

- Decrease in Deals: The number of deals fell from 126 in H1 2023 to 104 in H1 2024.

- Decrease in Value: Total deal value dropped from €15.1bn to €10.7bn.

- Insurance Sector:

- Increase in Deals: The number of deals rose from 130 in H1 2023 to 162 in H1 2024.

- Decrease in Value: Total deal value fell from €5.2bn to €4.1bn.

- Wealth & Asset Management Sector:

- Decrease in Deals: The number of deals fell from 124 in H1 2023 to 101 in H1 2024.

- Decrease in Value: Total deal value decreased from €3.5bn to €2.3bn.

If economic conditions improve as anticipated, M&A activity in Europe’s financial markets should rise in the second half of the year as firms pursue growth and scale, and private equity disposals are gradually released.

by Yana Keller

by Yana Keller