Fitch Ratings assigns a neutral 2026 outlook to the Latin American insurance sector across its rated markets. One exception stands out.

Mexico moves to a deteriorating outlook, driven by recent tax reforms that Fitch expects will weigh on sector performance.

The broader regional view rests on a steadier macro backdrop. Fitch points to moderating inflation and easing interest rates, trends that should support earnings and improve solvency metrics.

External shocks still loom, as they always do in the region, but Fitch doesn’t expect them to derail operational progress in a material way. At least not yet, Beinsure says.

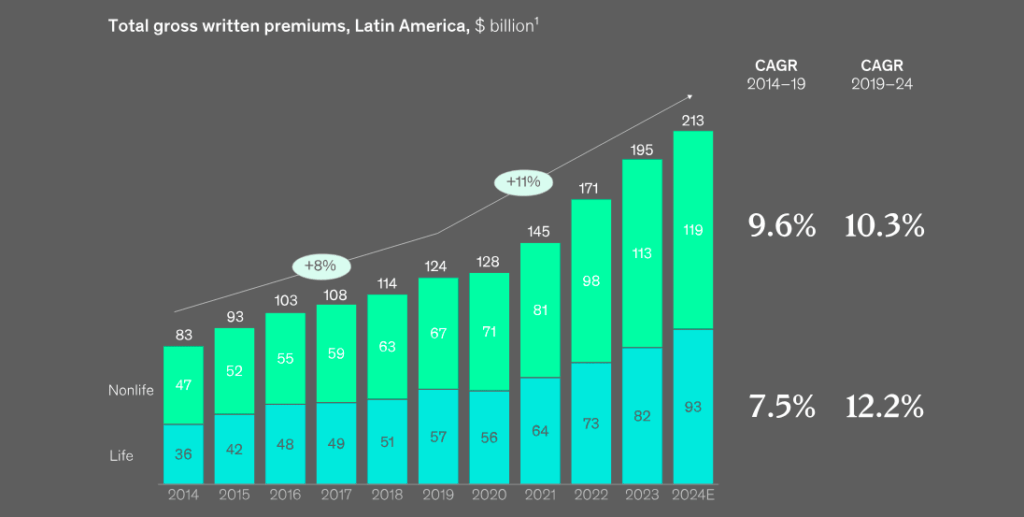

The Latin American (LatAm) insurance market shows solid growth, projected to exceed $180 bn in premiums by 2025, driven by rising middle class, digitalization, and increased awareness, despite macroeconomic challenges like inflation and currency volatility.

Key trends include strong expansion in non-life (health, motor, property), improving profitability (though volatile by country), and strategic shifts toward digital sales, with a generally “neutral” outlook for 2025 from Fitch Ratings, anticipating stable capital and moderate economic recovery.

Premium growth and financial results should remain moderate through late 2025 and into 2026. Health, motor, and property insurance are major growth areas, with health expected to reach over $130 bn by 2030.

The agency ties that forecast to stabilization in core indicators such as GDP growth, inflation, and rates.

LatAm insurance market premiums

Growth is being driven by nonlife insurance segments, especially property and casualty (P&C). According to Beinsure, home and auto insurance have increased significantly, driven by rising policy prices in auto contracts between 2022 and 2023, though growth in these segments may decelerate as this repricing phase slows. That may deliver stronger growth to the life segment – a shift we began to see during 2025.

At the same time, insurers will need to absorb new regulatory frameworks scheduled to take effect in 2026. That transition won’t be free.

Higher demands around review, control, and systems are likely to strain operating efficiency, especially for smaller players.

Regulation keeps shaping the trajectory. Fitch flags the interest rate cycle, the speed of structural reforms, and each market’s exposure to external shocks as decisive variables. Inflation hasn’t vanished, price competition keeps tightening, and medical costs keep climbing.

Together, those forces squeeze technical margins, most visibly in auto and health, and chip away at profitability and capital buffers.

Political risk stays high. Elections are approaching in Chile, Peru, Colombia, and Brazil. Structural reforms continue in Panama and Colombia.

These shifts could reshape demand, alter product design, and force changes in risk management. Capitalization and earnings sit downstream from all of it.

Fitch also expects competition to intensify as fiscal reforms filter through. Pricing pressure should increase. Acquisition costs likely rise. Insurers will respond by reworking products and pushing harder on segmentation. Digital build-out won’t be optional.

According to Beinsure, faster digital adoption looks less like a growth bet and more like a survival tool in a region facing tighter margins and heavier regulatory lift.