Fitch Ratings expects consolidation in the German life insurance sector to pick up speed in 2026, driven by closed-book acquisitions.

The life insurance market for consolidators is maturing, in Fitch’s view, and more than EUR100bn of life liabilities now sit in closed books that could come to market.

The motivation to offload legacy portfolios is straightforward. Administrative costs keep climbing, IT migration included, while policy counts shrink.

Selling closed books lets life insurers redirect attention to new business and, just as important, release capital that would otherwise stay tied up.

For run-off specialists, scale changes the economics. Acquiring closed books supports volume growth and underpins already strong financial results. These transactions don’t move quietly, though.

Regulators scrutinize them closely, with a sharp focus on policyholder treatment and governance standards.

Even with that oversight, Fitch sees momentum building. Zurich Insurance Group is evaluating options for a potential sale of its closed German life portfolio.

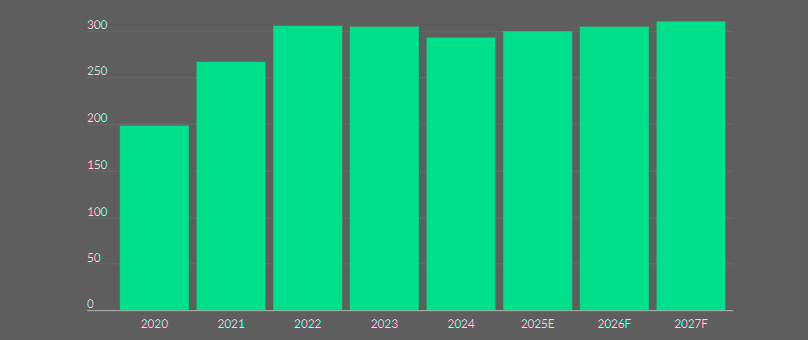

Aggregated Solvency II ratio stable at 300%

With total assets near EUR20 bn, Fitch estimates that overall closed-book transactions in Germany could reach as much as EUR25 bn next year.

That would rank as the second-largest annual total since Germany’s first run-off deals in 2014. Activity has never been evenly distributed. The prior peak, EUR49 bn in 2018, stemmed almost entirely from Viridium Group acquiring the closed life portfolio of Generali Deutschland.

Viridium and Frankfurter Leben remain the two largest domestic consolidators. Fitch also sees room for greater participation from Athora, a Bermuda-based group with a growing European footprint.

Athora already operates at scale in the Netherlands and is expanding in the UK, pending regulatory approval of its acquisition of Pension Insurance Corporation.

In 2025, Fitch assigned first-time Insurer Financial Strength ratings to Viridium at A+ and Frankfurter Leben at BBB+. Both carry Stable outlooks.

Fitch expects run-off specialists to keep capital strength intact over the medium term, supported by steady operating capital generation. That expectation feeds into Fitch’s neutral sector outlook for German life insurance in 2026.

Germany’s weak economic conditions in recent years have weighed on demand for life savings products. A sharper downturn could push lapse rates higher and force some insurers to crystallize losses on fixed-income portfolios.

Fitch views that scenario as unlikely, given historically low lapse behavior in the German market.

Premium income should stabilize in 2026 after rising about 5% in 2025. That growth came largely from single premiums, up roughly 20%, which Fitch expects to flatten next year.

New annual-premium business is forecast to increase by around 2% in 2026, with room for stronger growth if economic uncertainty fades.

Capitalization remains the anchor. Fitch expects German life insurers, consolidators included, to hold Solvency II ratios close to 300% on average at end-2025 and end-2026. Higher market interest rates relative to guaranteed rates continue to support that position.

This outlook already factors in the additional mathematical reserve, the Zinszusatzreserve, embedded in legacy books.

Most insurers should see modest declines in that reserve through end-2026, as the reference rate holds steady at 1.57%.