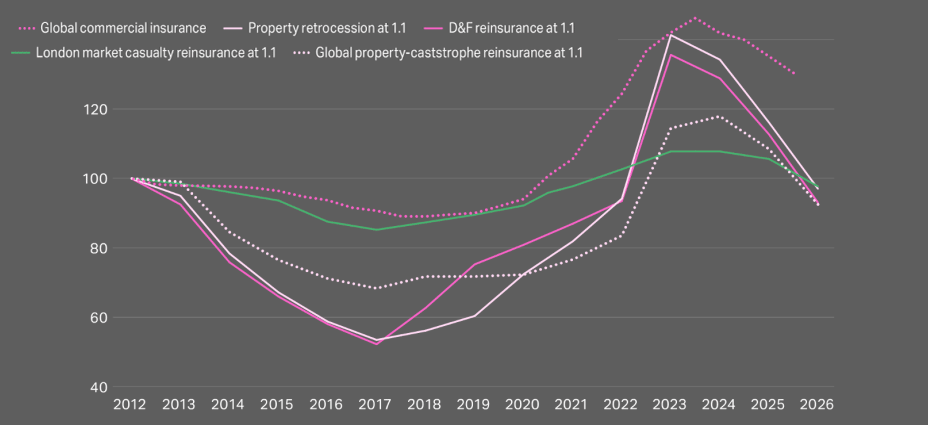

At the January 2026 renewals, reinsurance broker Howden Re estimates that risk-adjusted pricing for property catastrophe treaty business fell by 14.7%.

That marks the biggest year-on-year decline since 2014. Property retrocession pricing dropped even further, down 16.5%.

In its 2026 renewal report, Howden Re said most segments of the market recorded price declines at 1/1. Pricing levels now sit roughly where they were four years ago, although attachments remain higher and terms tighter. So cheaper, yes, but not loose.

According to the broker, market performance stayed strong through 2025. Insurers and reinsurers generated returns above their cost of capital, even after the Los Angeles wildfires, one of the largest insured loss events on record.

Buyers benefited from abundant supply and aggressive competition. That combination created room for broader coverage at discounted pricing. We think that explains why negotiations moved so quickly.

Howden Re also published its latest pricing index covering primary insurance, reinsurance, and retrocession. The picture is consistent. Direct and facultative business saw the steepest risk-adjusted drop, with rates-on-line down 17.5%.

Retrocession followed at 16.5%. Global property catastrophe treaties declined 14.7%. London market casualty excess-of-loss softened too, though less dramatically, down around 5%–10%.

Looking specifically at global property catastrophe reinsurance, Howden Re said another year of elevated catastrophe activity didn’t stop the slide.

Even with record wildfire losses in California, programmes renewed with sizeable rate cuts and modestly improved terms. Average risk-adjusted rates-on-line fell 14.7%, accelerating from the 8% decline seen in 2025.

Risk-adjusted price reductions recorded at the January 1, 2026 reinsurance renewals

In the US, cedents benefited from strong supply as reinsurers stayed willing to deploy capital at margins they still found attractive. Programme-wide reductions generally landed between 10% and 20% on a risk-adjusted basis. Capital was there. Appetite followed.

Europe told a similar story, though driven by different forces. Low loss activity, excess capital, and reinsurers defending top-line volume shaped outcomes.

Average programme rate decreases also clustered between 10% and 20%. Defensive behaviour, but still soft.

Asia-Pacific remained competitive. Cedents built on mid-single-digit reductions from 2025 and leaned into abundant capacity. For loss-free non-proportional programmes, risk-adjusted pricing typically fell by 10%–20%. No drama, just steady pressure.

Howden Re’s estimates diverge somewhat from those published by Guy Carpenter & Co. Guy Carpenter’s indices show global property catastrophe rates down 12% at Jan. 1, 2026.

The US and Asia-Pacific posted 12% declines, while Europe saw the steepest drop at 15%. Different lenses. Same direction.

Retrocession looks even looser. Howden Re said capacity at the January 2026 renewal comfortably exceeded demand, even as conditions grew more balanced. Buyers explored as much as $800 mn of additional limit. Supply held firm.

That supply came from retained earnings built over several profitable years, new market entrants, and steady ILS inflows. Losses stayed manageable.

The Los Angeles wildfires hit only a small number of programmes, with impacts softened by expected subrogation recoveries. According to Beinsure analysts, that containment helped unlock further price pressure.

Howden Re estimates risk-adjusted retrocession pricing fell between 12.5% and 21%. Outcomes varied widely, depending on attachment points, coverage breadth, and underwriting results.

Terms barely moved. Retrocessionaires showed little interest in expanding cover to non-natural perils such as SRCC or terrorism.

Casualty renewals told a different, messier story. Improved supply dynamics shaped January outcomes, especially in the US. Pricing leaned heavily on performance, set against persistent long-tail loss development, reserve uncertainty, and sustained demand for protection.

The broker also pointed to the growing role of casualty ILS and sidecars in US renewals. That theme keeps building.

The casualty ILS market gained momentum through 2025, with several second-half transactions hinting at a path toward rapid expansion, according to Willis Re. Whether that growth stays controlled is another question hanging in the air.