The Contractual Service Margin (CSM), part of IFRS 17, gives users clearer information on insurers’ expected profits. Fitch Ratings states that this change makes insurance accounting more useful.

IFRS 17, effective from 1 January 2023, improves on IFRS 4 by showing unearned profits through the CSM, offering a clearer view of profitability.

The CSM sits within an insurer’s liabilities. It reflects future profits not yet earned over the contract period. It removes any immediate gains at inception and is released gradually through the income statement as services are provided (see how International Financial Reporting Standards 17 Reshapes Insurance Accounting).

This leads to a more consistent and transparent profit profile than IFRS 4 allowed.

The CSM adds a new layer of detail. It reveals information previously unavailable under IFRS 4. When shown at a product or business line level, it helps spot areas of strength or risk.

For example, a product priced with certain assumptions may later need changes if conditions shift. This can lower the expected profit and affect CSM release.

However, most firms only report CSM at a broad level. As a result, CSM’s full value as a forward-looking metric remains underused.

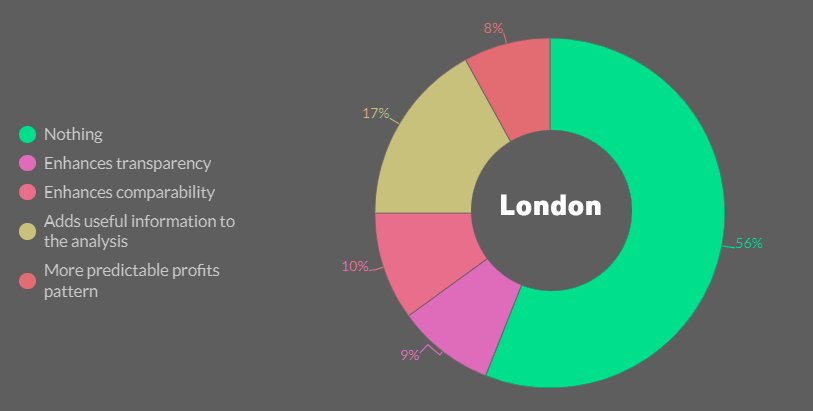

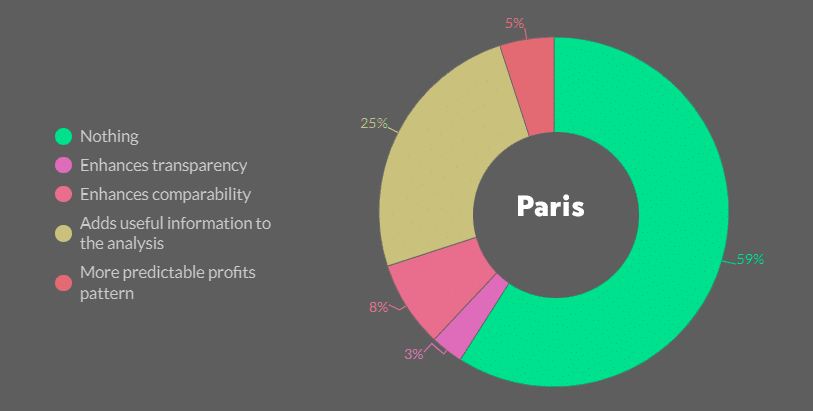

What Do You Like the Most About IFRS 17?

Fitch believes IFRS 17 helps improve how users assess insurers’ profitability, even though the switch from IFRS 4 has not been simple.

The CSM helps users spot both risks and opportunities across portfolios. By spreading future profits over time, IFRS 17 aligns reported figures more closely with actual performance.

Achieving full comparability between insurers will take time. Companies use different models and make different disclosure choices.

Still, the industry is moving toward more uniform reporting, and progress should continue over the next reporting periods.

Although IFRS 17 is in place, many insurers still rely on familiar metrics like Solvency II premium growth and traditional combined ratios. These habits reflect years of working under IFRS 4. As leadership changes, reliance on old methods may decline. This could raise IFRS 17’s role in future decision-making.

While IFRS 17 does not change insurers’ credit strength or basic economics, it does show more clearly how profits are earned or deferred over time.

These insights may highlight strengths or reveal pressure points in profit timing.

Polls at Fitch’s Insurance Insights conferences in London and Paris last month show hesitation. When asked about the most useful part of IFRS 17, over half of each audience expressed doubts.

Much of this may come from the disruption caused by the shift to a new system. As stakeholders grow more familiar with IFRS 17, its benefits should become more widely accepted.