Lemonade, a leading insurtech company, has announced its financial results for the second quarter of 2024.

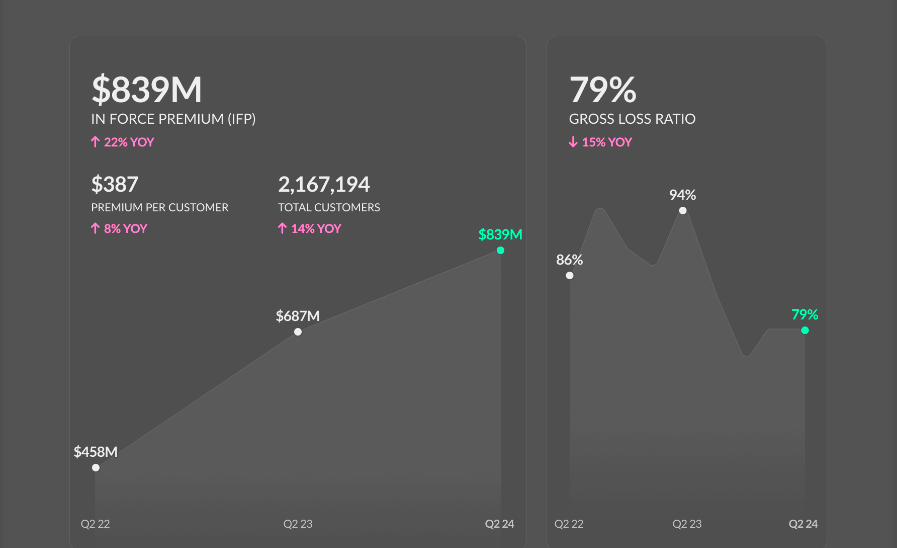

In Force Premium (IFP), which represents the aggregate annualized premium for customers at the period’s end date, increased by 22% to $838.8 mn compared to the second quarter of 2023.

The company also saw a 14% increase in its customer count, reaching 2,167,194 customers. Premium per customer rose to $387, up 8% from the same period last year.

Annual Dollar Retention (ADR), a metric indicating the percentage of IFP retained over a twelve-month period, increased by one percentage point to 88%.

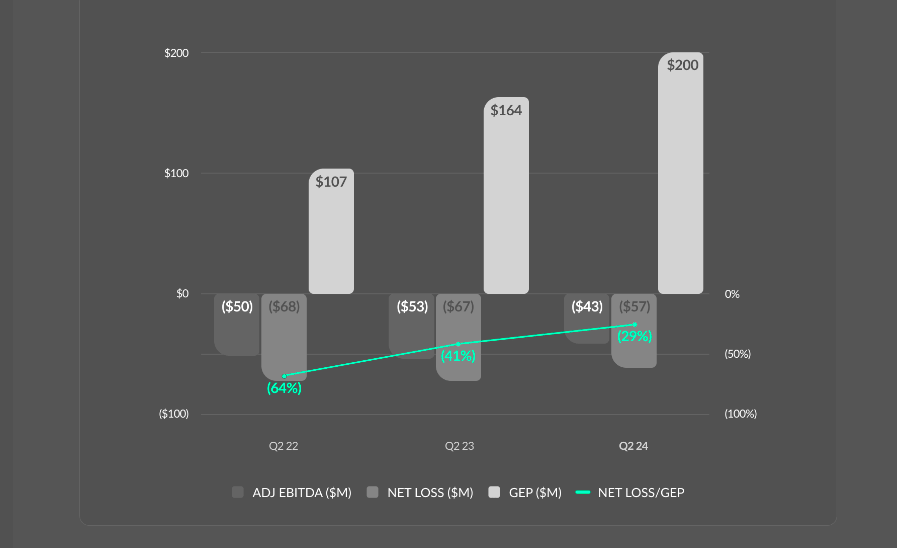

Gross earned premium for the quarter amounted to $199.9 mn, reflecting a 22% increase from the previous year, driven by higher IFP earned during the quarter.

Revenue for the second quarter was $122 mn, up 17% from the second quarter of 2023, primarily due to the increase in gross earned premium and net investment income.

Gross profit saw a substantial increase of 155%, reaching $30.8 mn, mainly due to higher earned premium and an improved loss ratio. Adjusted gross profit, a non-GAAP metric, also rose by 101% to $33.4 mn.

Total operating expenses, excluding net loss and loss adjustment expenses, increased by 13% to $106.6 mn, mainly due to higher growth spending for customer acquisition, partially offset by lower employee-related costs.

Our second-quarter results have shown remarkable performance with strong topline growth, stable expenses, and a positive net cash flow (NCF)

Daniel Schreiber, Co-Founder, Chief Executive Officer, and Chairman of our board of directors Lemonade

Net loss for the second quarter was ($57.2) mn, or ($0.81) per share, improving from a net loss of ($67.2) mn, or ($0.97) per share, in the same period last year. Adjusted EBITDA loss improved by 18% to ($43.0) mn, driven by higher revenue.

Lemonade’s cash, cash equivalents, and investments totaled approximately $931 mn as of June 30, 2024. The company reported a net cash flow of $4 mn for the second quarter, a significant improvement from ($51) mn in the second quarter of 2023.

Key Operating Metrics:

- Net Cash Flow: We were NCF positive in Q2 2024 and expect to remain so, except for Q4 2024.

- Top Line: In Force Premium reached $839 mn, growing 22% year over year, while revenue increased by 17%.

- Gross Loss Ratio: Improved to 79%, a notable 15-point improvement year over year. The trailing twelve months (TTM) gross loss ratio was also 79%, 12 points better than the prior year and 4 points better sequentially.

- Gross Profit: Increased by 155% year over year, with the Gross Profit Margin doubling to 25%.

- Operating Expense: Increased by 13% or $12 m year over year, primarily due to a $13 m increase in growth spend, while other operating expenses remained stable.

- Bottom Line: Adjusted EBITDA loss improved by 18% year over year to ($43) mn, and Net Loss improved by 15% to ($57) mn.

Cash Flow Importance

Q2 2024 was NCF positive, and we expect to maintain this status, barring Q4 2024 due to seasonal patterns. Our cash and investments balance, currently at $931 mn, is projected to dip slightly before rising consistently.

Cash flow is critical for several reasons:

- In the insurance industry, cash flow precedes earnings, providing a leading indicator of our model’s benefits and a current picture of our business fundamentals.

- The cash flow statement captures the impact of our growth spend, largely financed by our synthetic agents partner, which is missed in a P&L-centric view.

- NCF is a key metric for us, as we invest in profitable growth to maximize long-term cash flow, which drives enterprise value.

We plan to emphasize cash flow in future periods as we reinvest in profitable, capital-light growth.

Loss Ratio Management:

Despite a surge in natural catastrophe events (“CAT”) in Q2 2024, our gross loss ratio remained stable at 79%. Key strategies to reduce CAT-related volatility include:

- Growing products with lower CAT exposure, such as pet and renters insurance.

- Diversifying geographically, particularly in Europe.

- Using AI-powered LTV models to sell homeowners policies selectively.

- Placing home premium with other carriers in select geographies.

- Non-renewing certain CAT-exposed policies that our AI models would not underwrite today.

Lemonade are encouraged by the following trends:

- Year-over-year, the gross loss ratio improved by 15 points, marking the fourth consecutive quarter of significant improvement.

- TTM gross loss ratio improved by 4 points sequentially and 12 points year over year.

- Gross loss ratio excluding CAT improved by 11 points year over year.

Operating Leverage:

We have achieved impressive operating leverage, with notable growth in our book of business and stable operating expenses:

- Over the past 2 years, the compound annual growth rate (CAGR) of In Force Premium (IFP) at 35% is more than 3 times the CAGR of operating expense at 11%.

- Excluding growth spend, 80% of which is funded by our synthetic agents partners, other operating expenses remained flat.

- In the past year, we grew the book by 22%, while our employee headcount shrank by 9%, leading to a 34% improvement in IFP per headcount.

These achievements highlight our ability to leverage technology for automation and operational efficiency. We expect this dynamic—robust, predictable IFP growth alongside stable expenses—to continue in the coming quarters and years.

Our tech-enabled business model allows us to scale efficiently, unlike traditional models where the value of scale diminishes over time. Our recent performance, marked by improving underwriting and operating leverage, positions us to capitalize on future opportunities as scale amplifies value creation.

by Peter Sonner

by Peter Sonner