New York households spent an estimated $1,935 on personal auto insurance, the highest figure ever recorded in the state and the fourth-highest level nationwide, according to the outlook from the Insurance Information Institute. Premium growth pushed auto coverage deeper into household budgets.

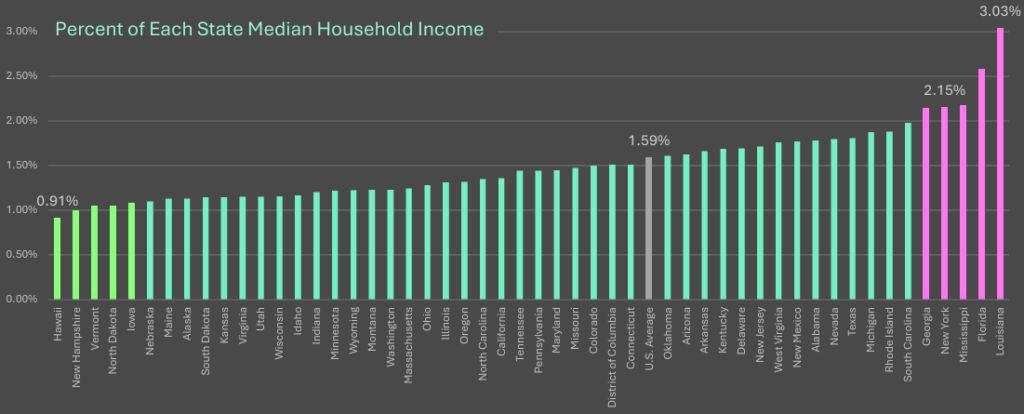

Triple-I data shows New Yorkers devoted 2.23% of median household income to auto insurance. The year before, households paid $1,753 on average, equal to 2.15% of income.

Even then, New York already ranked as the fourth least affordable state for auto insurance when measured against earnings.

According to Beinsure, the affordability gap has widened faster in New York than in most large metro-heavy states.

The Institute’s issues brief compares New York’s spending patterns with national benchmarks and drills into cost pressures behind premium growth.

Four of the state’s six major cost drivers sit near the top nationally, a mix that keeps rates elevated and sticky, acording to US Auto Insurance Rates by States.

Personal Auto Insurance Expenditures

National context sharpens the contrast. U.S. households spent about 1.6% of median income on personal auto insurance. New York households spent 2.15% during the same year, well above the national norm.

According to our data, few states with similar income levels show a gap this wide.

Several reform proposals remain under discussion. These include tighter insurer anti-fraud programs, limits on damages for drivers engaged in unlawful behavior or deemed at fault, adjustments to the serious injury threshold, and broader use of technology in claims and underwriting.

Analysts say changes along these lines could reduce cost pressure over time, though outcomes depend on execution.

New York Personal Auto Insurance Expenditures: U.S. Ranking

- Repair Cost Severity: Third Highest in the U.S.

New York has the third highest auto repair costs in the U.S. On average, repair costs total $7,043 per claim, which is $864 more than the U.S. average of $6,219. This figure represents the median claim payment amount for combined private passenger auto property damage liability and collision claims. - Carrier Expense Index: Third Highest in the U.S.

New York has the third highest carrier expense index for personal auto insurance at 14.9% of losses, compared with the U.S. average of 12.3%. The personal auto insurance expense index measures the share of incurred losses insurers spend to process, investigate, and litigate claims, including litigation expenses. - Injury Claim Severity: Third Highest in the U.S.

New York has the third highest average injury claim severity in the U.S. The average personal auto injury claim is $46,726, more than twice the U.S. average of $28,045. This dollar amount represents the average payment made by insurers per personal auto insurance claim. Bodily injury severity is typically higher in no fault states. - Accident Frequency: Eighth Highest in the U.S.

Personal auto accident frequency in New York is 3.09, the eighth highest in the U.S. The national average is 2.62. This figure represents motor vehicle accident frequency, expressed as the number of property damage liability claims filed per 100 earned car years. A higher number represents higher accident frequency. - Tendency to File Injury Claim: 31st in the U.S.

New York has the 31st highest tendency to file a bodily injury (BI) claim in the U.S. The ratio of bodily injury liability claim frequency to auto property damage (PD) liability claim frequency measures the likelihood an injury claim being filed while accounting for di ering accident rates. The tendency tends to be higher in less a ordable states and lower in no-fault states such as New York. - Underinsured and Uninsured Motorists Costs

New York ranks 29th in the country for the share of underinsured motorists at 13.4%, below the U.S. average of 16.4%. It ranks 44th for the share of uninsured motorists at 8.60%, also below the U.S. average of 12.3%. High rates of uninsured or underinsured motorists can both reflect and contribute to a ordability challenges. The costs of uninsured and underinsured motorists directly add to the overall cost of personal auto insurance in a state.

Michel Léonard, chief economist and data scientist at the Insurance Information Institute, points to structural cost issues rather than pricing tactics.

He says elevated vehicle repair costs, severe injury claims, high claims-handling expenses, and frequent accidents combine to keep premiums climbing. Léonard argues sustained affordability gains require direct action on these underlying costs.

With annual auto insurance nearing $2,000, New York continues to rank among the most expensive states for drivers.

Cost metrics reinforce the picture. New York ranks third-highest nationally for auto repair cost severity. Carrier expense ratios also place third. Injury claim severity ranks third as well. Accident frequency lands eighth.

According to Beinsure, this combination leaves insurers little room to ease pricing without broader legal and operational change.