Overview

The insurance industry has long struggled with issues of transparency, access, and operational efficiency. Blockchain technology offers potential solutions by providing a more open and adaptable system. Dan Roberts, co-founder and CEO of Nayms, highlights the industry’s flaws, particularly regarding opaque capital practices.

Roberts shared on a recent Cointelegraph X Spaces that insurance firms often fail to ensure transparent capital usage. He referenced a $4 bn fraud case where even large insurers couldn’t verify if adequate capital was available for claims, ultimately leading to financial collapse.

Blockchain technology addresses this problem by enabling capital verification. Beyond this, it supports real-time price discovery, improved liquidity, and operational efficiency. Roberts also introduced the concept of insurance as a liquid, tradable asset. Nayms aims to create liquidity depth in the insurance market and increase capacity for coverage of digital assets.

How Insurance Operates

Property and casualty insurance revolves around risk transfer. Insurers transfer risk to other layers, forming a diversified pool that reduces risk correlation. When homeowners purchase insurance to protect against natural disasters, the insurer absorbs the risk.

However, insurers also seek protection through reinsurance, and reinsurers may further transfer risk through retrocession. Capital markets eventually absorb much of this risk via insurance-linked securities (ILS).

Roberts explained that ILS can fully collateralize events like natural disasters. For example, a $100 mn potential loss would be backed by $100 mn of collateral for immediate payout.

This setup bypasses lengthy payout chains. It allows capital markets to back catastrophe events, which are largely uncorrelated with interest rate fluctuations and traditional market risks.

Scaling the Insurance Market with Nayms

Nayms provides a reinsurance layer to support digital asset insurers. By enabling reinsurance, it increases issuable limits and total coverable risk. Roberts emphasized that Nayms does not act as a primary insurer. Instead, it supports capacity for primary insurers offering niche products like decentralized finance DeFi insurance.

For instance, when users transact on a decentralized exchange (DEX) or bridge, they may purchase DeFi insurance from a primary insurer.

Nayms supports this process by offering micro-insurance options for specific transactions, such as a three-minute bridge risk. This approach allows users to pay only for the required coverage period rather than an entire year, increasing affordability and efficiency.

Scaling has been a persistent challenge for insurers. Many struggle to offload risk into reinsurance markets due to perceived risks. Nayms aims to attract capital markets to back portfolios of digital asset insurers. This strategy broadens insurance capacity and offers capital markets access to diversified, uncorrelated yields.

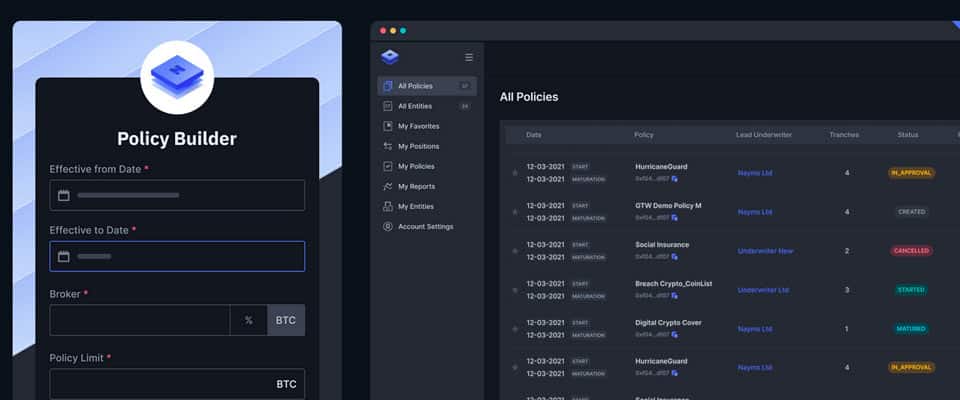

Tokenizing Insurance Participation

Nayms tokenizes participation agreements, embedding legal and regulatory obligations into tokens. This process allows investors to track and trade their insurance program exposures. Roberts described it as a shift away from the costly, months-long processes involving multiple parties.

The firm also launched the NAYM token to deepen market liquidity. Token holders gain governance rights, enabling them to influence how capital is allocated to insurance programs. Token holders can vote to support new coverage types or direct capital toward high-yielding programs.

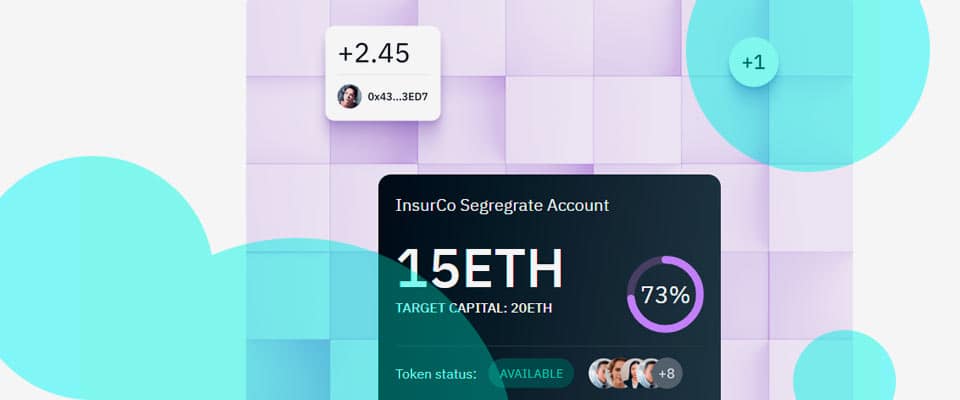

The Nayms Liquidity Facility (NLF) provides users with an entry point into insurance risk ventures. Users deposit stable assets into the NLF and receive NAYM tokens in return. These assets are then invested in insurance risk ventures, with profits shared in a governance pool. This model democratizes access to insurance, allowing broader market participation.

Expanding to New Chains and Markets

Nayms operates on Ethereum and Base but is exploring Layer-2 solutions and proof-of-concept initiatives with other chains. This strategy allows insurance programs to scale without requiring users to bridge assets between chains. By supporting sub-pools on various chains, Nayms can expand capacity for existing insurance programs.

The company also plans to launch its own reinsurance product, facilitating fundraising and streamlining coverage for primary insurers. Partnerships with collateral providers, including stablecoin providers and other yield-bearing assets, are part of this expansion effort.

Roberts stressed that Nayms aims to establish regulatory clarity for collateral-backed insurance products. This approach could pave the way for stablecoins, tokenized funds, and other collateral sources to be used in insurance products. He stated that Nayms seeks to create new use cases for these assets within the insurance sector.