Overview

The U.S. property and casualty insurance industry achieved its best underwriting performance in over 15 years in 2025. After 2 years of weak results, the industry has turned a corner, according to Swiss Re Insitute Report about US Property & Casualty outlook.

Strong premium growth and slowing claims cost inflation contributed to a combined ratio of 94%. Higher investment yields also provided a boost.

The P&C insurance industry’s return on equity (ROE) reached 14%, with full-year forecasts projecting an ROE of 9.5% in 2024 and 10% in 2025, along with premium growth of 8% and 5%, respectively.

Personal lines continue to drive growth and profitability improvements, while competition is reemerging in personal auto. However, growth in commercial lines, including property, is slowing (see TOP 100 Property & Casualty Insurance Companies in the U.S.).

- Outlook for 2024 remains favorable after strong underwriting results and rising investment returns contributed to 14% ROE

- Forecast industry ROE of 9.5% in 2024 and 10% in 2025

- Premium growth estimate at 8% for 2024 and 5% for 2025

- Personal lines remain the growth driver this year; commercial lines are slowing, with property lines seeing a notable deceleration.

- Higher reinvestment yields resulted in a much-improved investment result in 2024 compared to a year ago.

Swiss Re anticipate higher industry ROE as personal lines’ margins improve.

We maintain our forecast of 9.5% ROE for 2024 and 10% for 2025, close to the industry’s cost of capital of 10-11% and increase from 3.4% in 2023. Q1-Q2 2024 results confirmed this positive trend, with ROE reaching 14%

This momentum is supported by strong premium growth, easing inflation, and improved investment returns. In 2024, net premiums earned increased by 12% year-over-year, while net claims remained flat.

We expect this favorable gap between premiums and claims to continue through 2024. Additionally, Q2 2024 recurring investment yields were about one-third higher than the previous year.

Despite this optimistic outlook, risks remain. Social inflation could weaken favorable reserve development, an economic downturn could impact premium growth, and persistent inflation could further pressure claims costs, all potentially reducing industry ROE, but P&C insurers face several key risks and trends.

U.S. P&C insurance sector outlook

| Metric | 2023 | 2024 | 2025 |

| Premiums, Change | 10.1% | 8.0% | 5.0% |

| Combined Ratio | 102.3% | 98.5% | 98.5% |

| Underwriting Result | -3.1% | 1.5% | 1.5% |

| Investment Yield | 3.5% | 3.7% | 4.1% |

| Return on Equity | 3.4% | 9.5% | 10.0% |

Fitch Ratings notes that the U.S. P&C market is positioned for a return to underwriting profitability and significant capital returns for the full year, although results may not match levels due to uncertainties related to natural catastrophe exposures and loss reserve developments.

P&C insurance earnings will materially improve in 2024 amid recovery in personal lines results and only modest deterioration in commercial lines

The market faces challenges in sustaining commercial lines pricing to keep pace with ongoing loss-cost inflation and heightened litigation risks in several segments.

Personal P&C insurance to drive growth

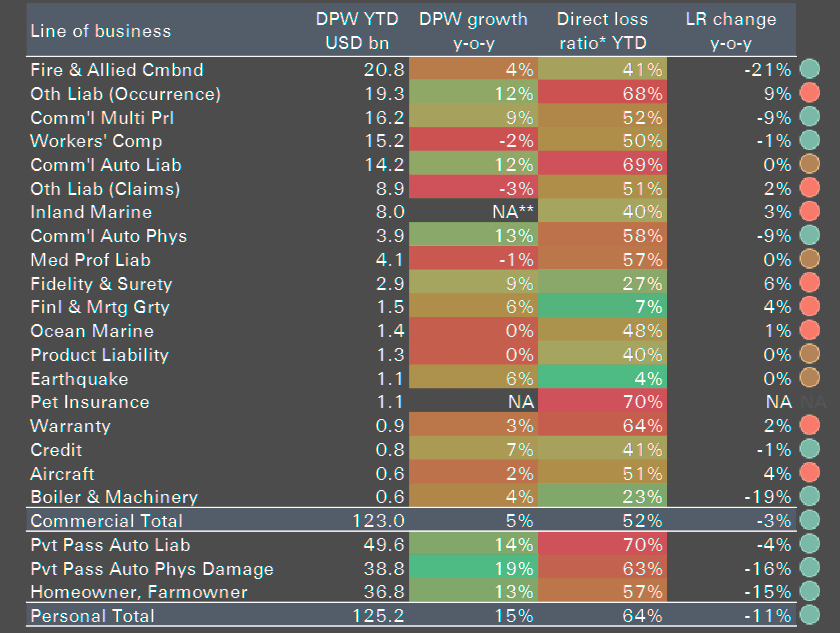

Personal lines to drive growth again, as commercial lines slow. We forecast P&C direct premiums written (DPW) growth of 8% in 2024 and 5% in 2025, after a close-to 10% annual gain between 2021 and 2023.

Industry growth remained at 10% in 1Q24, with personal lines premiums up 15% and commercial lines up just 5%.

We see upside risk to our growth forecast.

- Personal auto rate increases exceeded 6% in each of the 18 months through May 2024. In contrast, commercial lines growth has weakened as rate increases subside.

- Fire & Allied premium growth slowed rapidly to just 4% yoy in 1Q24 after 14% growth in 4Q23 – the slowest growth rate in over five years.

- Premiums for Other Liability Claims-Made policies – a statutory line that includes E&O, D&O, and Cyber Liability – shrank for the 7th consecutive quarter.

- Strong Commercial Auto Liability growth and a rebound in Other Liability-Occurrence premiums provided an offset.

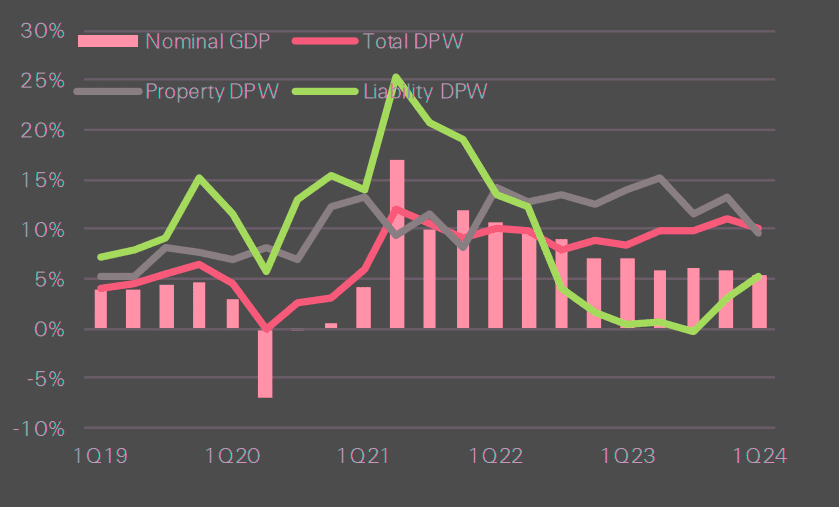

- Growth is heavily influenced by the underwriting cycle but supported by exposure growth: we forecast that US real GDP, a broad exposure proxy, will grow by 2.2% in 2024 and 1.9% in 2025.

Premium growth and loss ratios by line of business

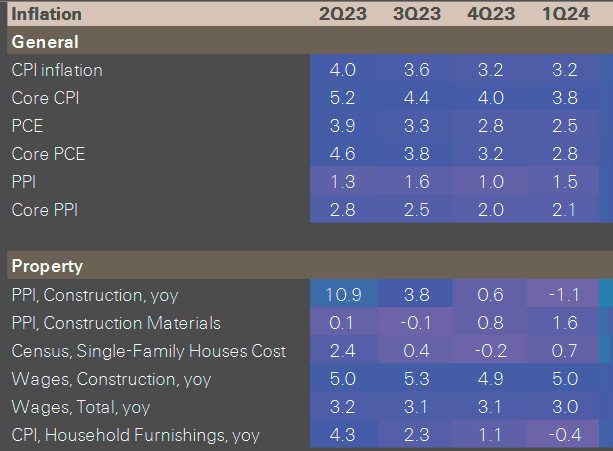

Despite improvement in insurance property lines after a light cat quarter, the overall industry loss ratio was broadly in line with the prior year, indicating a potentially difficult result if cats are in line with historical averages, according to P&C Insurance Pricing Trends. Property lines face pressure from the rising costs of materials, components and wages. We forecast construction costs to increase 9% in 2023 and 11% in 2024.

Higher underwriting profits in 2025

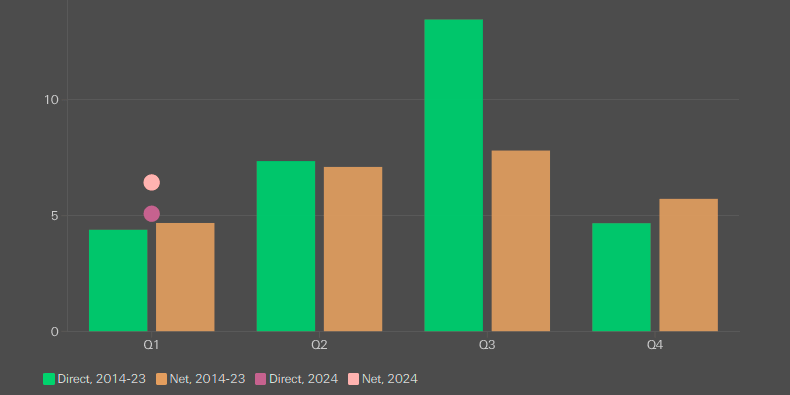

Swiss Re Institute forecast an industry net combined ratio of 98.5% in 2024 and 2025, much improved from 102% in 2023. The 1Q24 combined ratio of 94% was an 8 ppt improvement on a year earlier, driven by strong underlying results and aided by a lighter catastrophe loss burden.

Natural catastrophes added 5.1 ppts to the 1Q24 loss ratio (down from 7.2 ppts in the prior year).

Despite the strong 2024 performance – equivalent to a combined ratio of roughly 96% when normalized for an annual average catastrophe load – we maintain our combined ratio estimate because we are still in the early stages of what is forecast to be an active Atlantic hurricane season.

The second and third quarters typically generate most catastrophe losses on a direct and net basis, and preliminary reports suggest that 2Q24 was well above the previous 10-year average.

Catastrophe losses as a percentage of earned premiums on a direct and net basis

A high number of severe convective storms – including 11 events with >USD 1 billion in economic losses – and 1 000 tornadoes in the year through early June, continue to pressure claims costs.

Underwriting results are expected to improve

Underwriting results are expected to improve through 2024 as US headline CPI inflation declines to 3.1% in 2024 and further to 2.5% in 2025. This, combined with ongoing rate increases, should lead to premiums outpacing claims costs. Personal lines have been a significant positive factor.

In 2023, the loss ratio in personal lines was 17 percentage points higher than in commercial lines, but by 1Q24, the gap narrowed to 12 percentage points.

Homeowners’ insurance saw a 15 percentage point improvement in loss ratios in 1Q24 compared to the previous year. Premiums are now catching up with the increased replacement costs of homes, driven by a surge in construction costs since 2020.

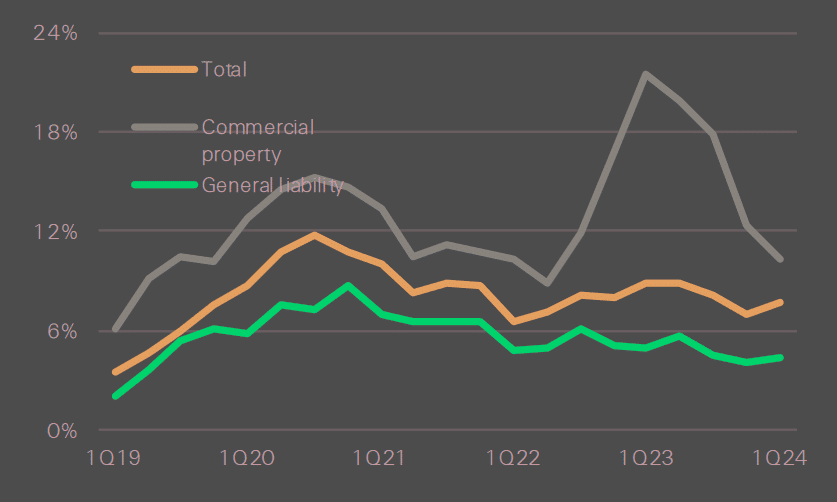

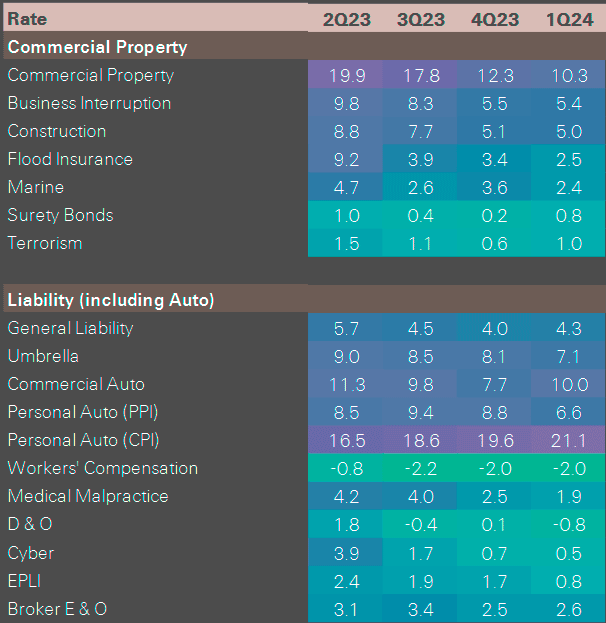

Commercial rate changes

We expect property lines claims costs (excluding catastrophe events) to decelerate as construction prices rise by 0.2% in 2024 and 2.5% in 2025, after increasing by about one-third between 2021 and 2023.

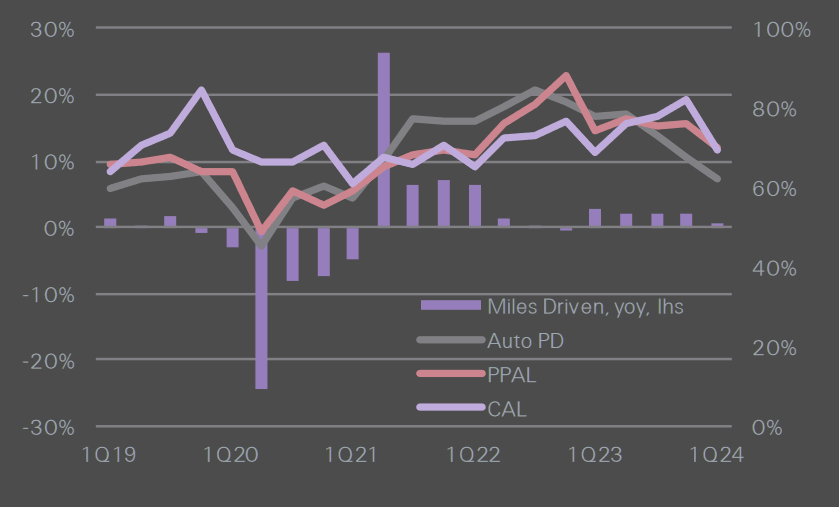

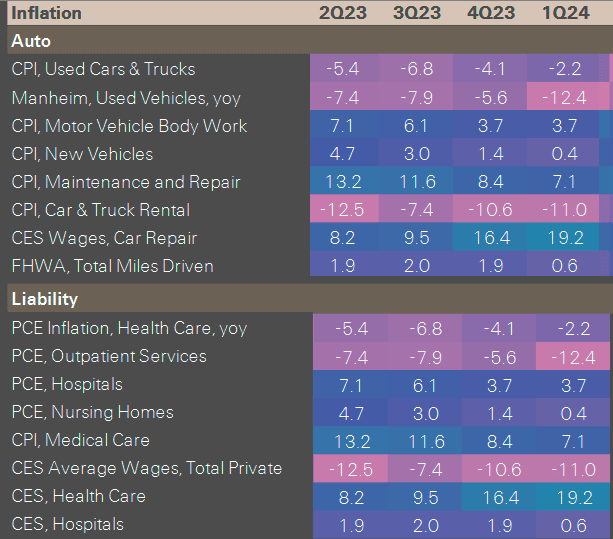

Disinflation is also expected to improve personal auto margins. In May’s US CPI data, used car prices dropped by 9.3%, while repair costs increased by 9.5%, aligning with pre-pandemic levels. This divergence is leading insurers to total a higher share of vehicles.

Exposure and P&C insurance premium growth

Liability lines, however, will see less benefit from economic disinflation due to the nature of claims and increased exposure to social inflation factors. Although commercial lines may face margin pressures after a period of favorable underwriting results, they remain strong for now.

Personal auto rushes back to competition

Price gains in personal auto insurance have started to decelerate as more carriers reach rate adequacy and competition for new business picks up. The motor vehicle insurance CPI measure quoted in headlines was up 20.3% y-o-y in May after peaking at 22.6% in April.

We believe this figure remains an over-estimate but expect deceleration to continue. Based on data from the largest public P&C comparative raters, insurers are pursuing growth.

Between 4Q23 and 1Q24 auto insurance ad spend more than doubled, and by one estimate is projected to increase another 60-70% sequentially in 2Q24 despite 2Q historically being a seasonally down quarter.

Miles driven and Motor loss ratios

This is a rapid bounce back after P&C insurers cut online ad spending by more than half from 2021 to 2023. The return to growth is reflected in the market capitalization of comparative raters, which has more than doubled since October 2023 after falling by nearly two-thirds since 2021.

P&C insurers investment income

Swiss Re continue to expect investment yields to rise to 3.7% in 2024 and 4.1% in 2025. Most of the increase will be driven by recurring investment income. Headline yields of 4% – or 3.5% adjusted – reflect the benefits of higher interest rates across maturities.

We expect reinvestment yields to remain above average yields on maturing securities. In 2025, higher realized capital gains should be an additional tailwind for investment results.

Swiss Re currently forecast the upper bound of the Fed funds rate target range to decrease in two steps during 2024, from 5.5% to 5%, before declining to 4% by the end of 2025. This is our baseline, but we see potential for fewer cuts. “We forecast the 10-year Treasury yield to end 2024 at 4.4% and 2025 at 4.2%”.

P&C Insurance Industry Statistics

FAQ

Strong premium growth, slowing claims cost inflation, and higher investment yields contributed to the industry’s best underwriting performance in over 15 years.

The industry’s ROE is projected to be 9.5% in 2024 and 10% in 2025.

Premium growth is estimated to be 8% in 2024 and 5% in 2025.

Personal lines are the main driver of growth, while commercial lines are slowing down.

Easing inflation has supported strong underwriting results, but persistent inflation could pressure claims costs in the future.

Social inflation, an economic downturn, and persistent inflation are key risks that could impact the industry’s performance.

The second and third quarters are expected to see most catastrophe losses, and 2Q24 has already shown higher-than-average catastrophe events.

Personal auto rate increases exceeded 6% through May 2024, but competition is reemerging as rate increases subside.

Investment yields are expected to rise to 3.7% in 2024 and 4.1% in 2025, driven by recurring investment income.

…………………………

AUTHORS: Thomas Holzheu – Chief Economist Americas Swiss Re Institute, James Finucane – Senior Economist Swiss Re Institute