Overview

The U.S. property and casualty insurance market is set for a return to underwriting profitability and significant improvements in return on capital for the full 2024 year. However, results may not match first-quarter levels due to uncertainty about natural catastrophe exposures and loss reserve experience, according to Fitch Ratings Report.

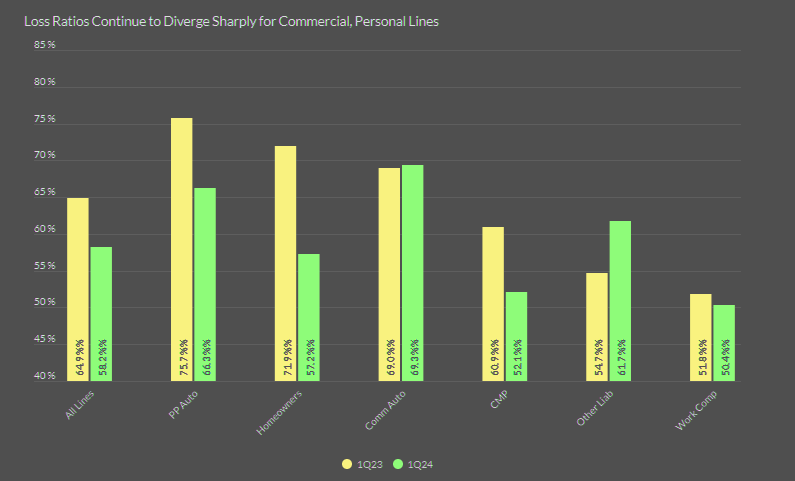

In the interim reporting period, there’s a clear disparity in underwriting performance between personal and commercial lines, as evidenced by the direct loss ratios. The personal auto sector continues to grapple with escalating loss severity, impacting incurred losses.

U.S. P&C insurers achieved a strong statutory underwriting profit year-over-year in the first quarter of 2024, driven by lower winter storm losses and a recovery in personal auto results.

The market faces significant challenges in maintaining commercial lines pricing to meet ongoing loss-cost inflation and increased litigation risks in several segments.

Favorable pricing conditions in the first quarter of 2024 supported strong growth in net written and earned premiums, at 10% and 11%, respectively.

The P&C Idustry Underwriting Results

The P&C industry underwriting combined ratio (CR) improved by over eight points year-over-year to 94% in the first quarter of 2024, marking the best first-quarter underwriting result since 2007.

Favorable prior period reserve development was higher in the first quarter of 2024, representing 3.3% of earned premiums compared to 1.9% in the prior year quarter.

Fitch’s sector outlook for U.S. personal lines insurance recently moved to Improving, while the sector outlook for U.S. commercial lines insurance remains Neutral.

For 2024, the U.S. P&C insurance sector holds a neutral outlook across both commercial and personal lines, expecting stable or better results, especially with the anticipated recovery in personal auto and steady performance in commercial lines.

Notwithstanding a robust 9% increase in earned premiums for 9M2023, the sector’s overall performance was impacted by weak auto insurance and higher-than-average catastrophe lossesю

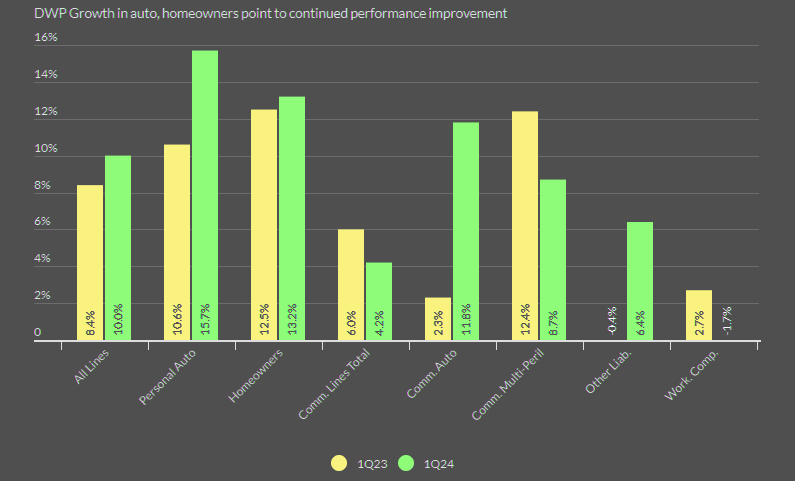

P&C Insurance Growth in Direct Written Premium

Operating income rose 300% year-over-year in the first quarter of 2024. The annualized operating return on surplus (ROS) increased to 10.2% from 2.4% in the first quarter of 2023.

Higher yields led to a 32% year-over-year increase in investment income, which included a one-time $2.1 billion dividend from Liberty Mutual affiliates.

Net income grew to $40 billion from $9 billion, influenced by $14 billion in realized gains from the National Indemnity Company’s sale of Apple Inc. stock.

Sharp price supports personal lines insurance

Sharp price increases will continue to support personal lines underwriting improvement through 2024, as reflected in direct written premiums (DWP) growth of 16% in personal auto and 13% in homeowners relative to 1Q23.

Commercial lines DWP growth slowed to 4% for the quarter. Workers’ insurance compensation growth turned negative in the quarter, and segments with greater claims challenges, including commercial auto and other liability, reported higher YoY premium growth.

P&C Insurance Industry Statutory Performance Highlights

| Performance, USD in bn | 2024 | 2023 | Change |

|---|---|---|---|

| Loss Ratio | 68.8% | 76.4% | -7.6% |

| Expense Ratio | 24.9% | 25.4% | -0.5% |

| Dividend Ratio | 0.3% | 0.4% | 0.0% |

| Combined Ratio | 94.0% | 102.2% | -8.2% |

| Return on Surplus | 10.2% | 2.4% | 7.8% |

| Net Written Premiums | 226.60 | 206.5 | 9.7% |

| Underwriting Gain Excl Policy Divs | 9.5 | (8.0) | -219.1% |

| Investment Income | 20.4 | 15.4 | 32.2% |

| Realized Investment Gains | 14.1 | 2.2 | 536.5% |

| Operating Income | 26.2 | 6.3 | 316.1% |

| Net Income | 40.3 | 8.5 | 373.4% |

| Policyholders’ Surplus | 1,065.9 | 1,007.0 | 5.9% |

Performance improvement in 2024 will be driven by personal lines results, thanks to significant recent pricing actions and a reduction in high loss severity trends. Commercial lines underwriting results are expected to remain profitable, with a slight deterioration in the loss ratio.

Weakness in the commercial auto and liability-occurrence insurance business has been offset by strong workers’ compensation results.

In the first quarter of 2024, the direct loss ratio in private passenger automobiles decreased by nine points, with the biggest improvement in physical damage coverage. The homeowners’ loss ratio also dropped by 13 points

P&C Insurance Loss Ratios

Persistently high inflation and slowing economic growth raises potential for an unfavorable shift in loss reserve adequacy that clouds the earnings picture, led by commercial auto and other liability product lines.

The accuracy of insurers’ loss projections for claims severity tied to inflation and litigation risks in commercial auto and other liability business will determine if the P&C industry will reach its 19 consecutive year streak of favorable calendar-year loss reserve development in 2024.

FAQ

The U.S. P&C insurance market is expected to return to underwriting profitability with improvements in return on capital throughout 2024. However, uncertainties around natural catastrophe exposures and loss reserve experience could impact overall results.

Personal and commercial lines showed a disparity in performance, with personal auto facing rising loss severity, while commercial lines maintained profitability. The direct loss ratio improved in both segments, with personal auto seeing recovery and commercial lines remaining steady.

Lower winter storm losses and improved personal auto results contributed to the strong underwriting profit in the first quarter. The industry’s combined ratio improved to 94%, the best result since 2007.

The sector saw favorable pricing conditions in the first quarter, leading to strong growth in net written premiums, with personal auto and homeowners growing by 16% and 13%, respectively. Commercial lines growth slowed to 4%, and workers’ compensation saw negative growth.

Operating income surged by 300%, and the return on surplus increased to 10.2%. Investment income grew by 32%, and net income rose significantly due to realized gains from the sale of Apple Inc. stock by the National Indemnity Company.

Challenges include maintaining pricing for commercial lines to offset loss-cost inflation and litigation risks. Additionally, there is potential risk of loss reserve adequacy issues, particularly in commercial auto and liability lines, due to inflation and economic uncertainty.

Personal lines are expected to continue benefiting from recent pricing actions, leading to underwriting improvements. Commercial lines are projected to stay profitable, though a slight deterioration in loss ratios is expected due to claims challenges in certain segments like commercial auto and liability.

………………………..

AUTHORS: James Auden – Managing Director at Fitch Ratings, Laura Kaster, CFA – Senior Director of North and South American Financial Institutions, Fitch Ratings