S&P Global Ratings says expanding private markets are creating tighter links between banks, insurers, and alternative asset managers across Europe. The credit ratings and risk analysis provider said those links increase financial system interconnectedness, even though direct exposures still look manageable.

The report, Private Market Nexus Increases Interconnectedness Among European Financial Institutions, was published on 11 June 2026. Direct exposure to private debt among European banks and insurers continues to rise.

The agency still views those exposures as relatively modest compared with the size of institutional balance sheets.

European private markets have grown fast enough to narrow the gap with North America. Private capital markets in North America have traditionally been larger and less dependent on bank financing.

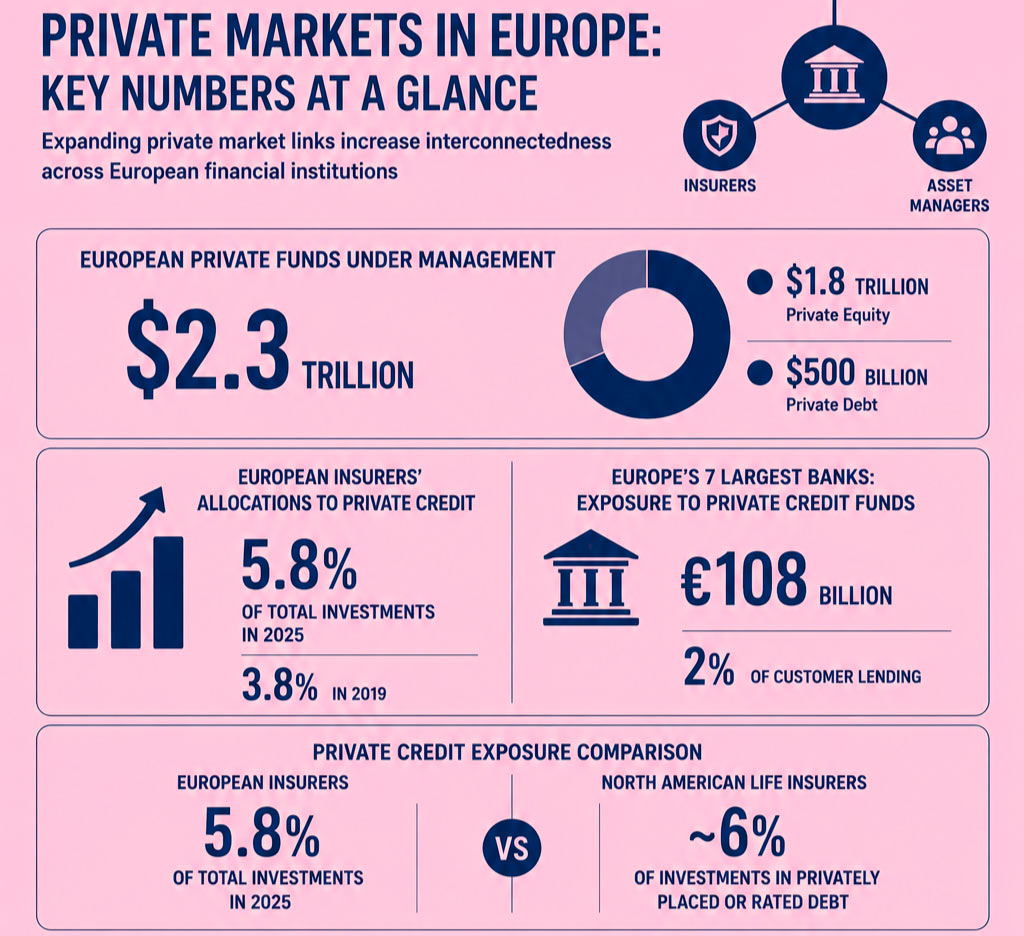

S&P estimates private funds focused on Europe now oversee about $2.3 tn in assets, including roughly $1.8 tn in private equity and $500 bn in private debt.

Andrey Nikolaev, credit analyst at S&P Global Ratings, said European private credit funds are gradually moving beyond mid-market lending into more credit classes. He said those funds are also deepening relationships with banks, creating new risk channels between traditional finance and alternative investment managers.

“European private credit funds are gradually expanding their lending activities from mid-market entities to more credit classes, while strengthening their relationships with banks. This indicates a wave of financial disintermediation and creates a private market nexus of interconnected risks and dependencies for European banks, insurance companies, and alternative investment managers,” Nikolaev said.

S&P said transparency around private credit remains limited, but available information suggests current risks remain manageable.

Bank exposure appears concentrated in a relatively small group of major institutions rather than spread evenly across the European banking sector.

The agency estimates drawn exposure to private credit funds among Europe’s seven largest banks at about €108 bn. That equals roughly 2% of customer lending. S&P said these exposures are generally secured, diversified, and backed by moderate loan-to-value ratios.

European insurers have also increased allocations to private credit. Based on regulatory data, S&P said insurers’ private credit allocations rose to 5.8% of total investments in 2025, compared with 3.8% in 2019.

Even after that increase, European insurer exposure remains below levels seen among North American life insurers. Privately placed or rated debt accounts for about 6% of investments at North American life companies, according to the report.

Current direct exposure levels suggest a private credit downturn would have a limited effect on ratings for large European banks and insurers. That assessment reflects the modest scale of direct holdings and the balance-sheet strength of major institutions.

S&P still sees reasons for closer monitoring beyond direct exposure figures. The wider network of relationships forming inside private markets creates dependencies between banks, insurers, and private finance firms.

Some banks now work with private credit managers to originate and distribute loans, creating more contact points between regulated institutions and less transparent capital providers.

Those relationships matter during stress because exposures do not always appear as simple balance-sheet holdings. Risk can sit in financing lines, loan distribution, fund relationships, collateral values, liquidity needs, and investor behaviour. The more private markets grow, the more those channels matter.

S&P also warned that weaker disclosure standards across private markets could magnify risks during market stress. Limited public reporting, less visible pricing, and the absence of public credit ratings can make exposures harder to assess.

That opacity could increase contagion risk if investors, banks, or insurers lose confidence at the same time. In a stressed market, uncertainty over asset quality can matter almost as much as losses themselves.

According to Beinsure analysts, the S&P report points to a practical supervisory issue rather than an immediate capital threat. European banks and insurers do not appear heavily exposed to private credit on a direct basis, but their relationships with private funds are becoming more complex.

The risk sits in connections, disclosure gaps, and valuation uncertainty when markets turn.