The U.S. private flood insurance market has grown quickly in recent years, showing favorable underwriting results, but it remains a small part of the property/casualty industry, Fitch Ratings reports. Despite this growth, only 4% of U.S. homeowners have flood insurance.

The gap between economic and insured flood losses remains significant. AccuWeather estimates economic losses from the recent flooding in Texas at $18–22 bn, while insured losses are expected to be much lower.

Fitch expects the private market to keep expanding gradually, supported by better flood mapping technology, improved analytics, regulatory changes, and the use of risk-based pricing in National Flood Insurance Program (NFIP) policies.

Private Residential Flood vs. National Flood Insurance Program

Private residential direct premiums written (DPW) have grown much faster than federal flood programs, though private market share remains much smaller.

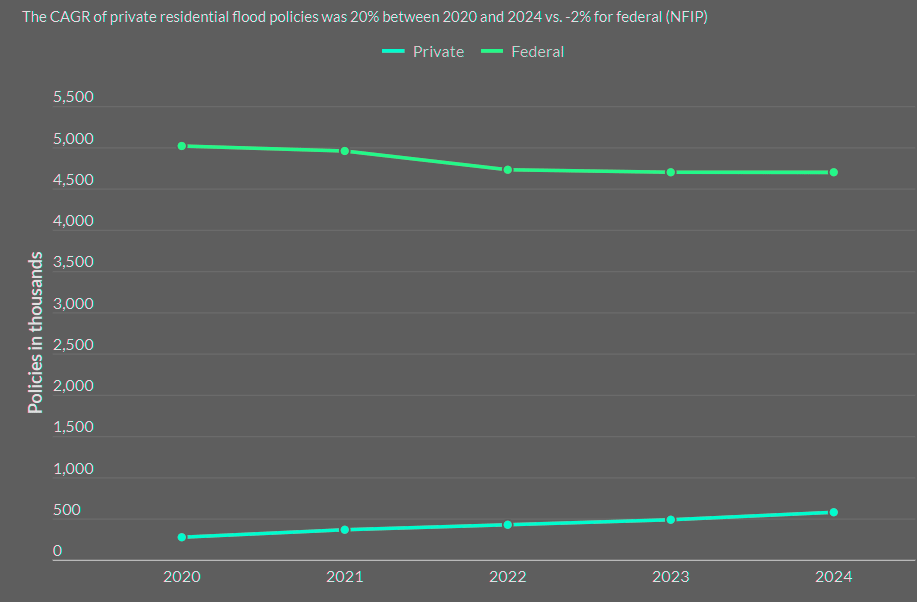

The number of private residential flood policies nearly doubled from 277,000 in 2020 to about 569,000 in 2024, while premium revenue rose by 240% to $0.5 bn.

Still, private flood remains small compared to other lines, as homeowners DPW totaled $170 bn in 2024. Therefore, even large economic flood losses are expected to have only a limited effect on overall industry loss results in 2025.

Private flood underwriting results have been strong in recent years. Over the past five years, the direct case incurred loss ratio on residential flood stayed below 50% in all but one year, and the average direct combined ratio was 60.4% from 2018-2024.

The only recent underwriting loss was in 2017, driven by Hurricane Harvey.

Fitch believes most underwriting exposure for U.S. private flood insurance is supported by the global reinsurance market and Lloyds of London syndicates.

These markets have increasingly gained exposure to U.S. flood risk over the past decade, through both support the primary flood business and the NFIP’s reinsurance program.