Overview

The U.S. private flood insurance market has grown rapidly in recent years with generally favorable underwriting performance but remains a small segment relative to the overall property and casualty insurance industry, Fitch Ratings says.

In the US, flood insurance historically had low participation, with most policies purchased to meet mortgage requirements in high-risk areas, predominantly through the National Flood Insurance Program (NFIP).

The report, US Private Flood Insurance: Trends and Insights, notes that growth in the private flood insurance market has been driven by improved technology and analytics, changes in federal flood insurance policies, and new legislative measures, according to Fitch Ratings’ report.

Key highlights of the US Private Flood Insurance Market in 2025

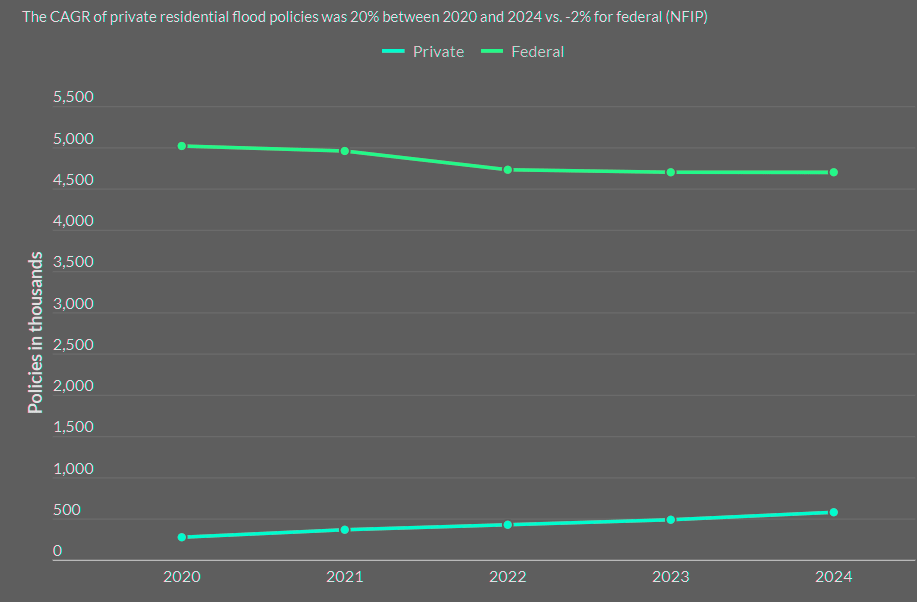

- The US private flood insurance market has expanded steadily, with private residential policies growing at a 20% annual rate from 2020 to 2024. Underwriting results have been favourable, with loss ratios for residential flood below 50% in all but one year over the past five.

- Flood remains one of the costliest risks for US homeowners, yet underinsurance persists. Only about 4% of homeowners carry flood insurance, and insured losses from major events remain far below economic losses. For example, Texas flooding in 2025 caused estimated losses of $18 bn–$22 bn, most of which were uninsured.

- The National Flood Insurance Program (NFIP) continues to dominate the market, especially in high-risk zones where mortgage requirements mandate coverage. However, frequent short-term extensions by Congress and low coverage limits ($250,000 for homes) limit its effectiveness.

- Advances in flood risk analytics, mapping, and technology, along with regulatory and policy changes—including risk-based NFIP pricing—have made private flood insurance more attractive to insurers and consumers, driving gradual market expansion.

- The global reinsurance market and capital market investors have increasingly supported both the private flood market and NFIP. Since 2018, NFIP has secured over $3 bn in reinsurance through catastrophe bonds and traditional placements, while reinsurers and Lloyd’s syndicates have provided expertise and capital to private carriers.

The US private flood insurance market is gaining traction in 2025 as flood-related economic losses continue to far outpace insured losses. Traditional reliance on FEMA’s National Flood Insurance Program (NFIP) has left many homeowners vulnerable, given that standard home policies exclude flood damage, Beinsure noted.

Recent improvements in flood risk analytics, mapping, and technology – combined with federal policy adjustments – have fueled private.

This growth assists homeowners who previously lacked adequate coverage despite living in risky areas. Insurance Information Institute data show that only around 20 percent of at-risk homes hold flood insurance, and a significant proportion of flood claims come from outside officially designated high-risk zones.

Gap between economic and insured flood losses

Flood risk is one of the most costly perils facing homeowners in the U.S. but remains broadly underinsured. The private flood insurance market continues to grow as a complement to the National Flood Insurance Program, offering solutions that can narrow the flood insurance gap.

The gap between economic and insured flood losses remains wide. Economic losses of $18 bn to $22 bn are expected from the tragic flooding in Texas, according to AccuWeather estimates, with insured losses expected to be substantially lower, Beinsure noted.

Only 4% of U.S. homeowners have flood insurance.

Private residential flood policies in force (PIF) grew at a compound annual rate of 20% between 2020 and 2024, compared to a -2% rate for federal flood policies.

The US private flood insurance market is expanding, addressing the nation’s substantial gap between economic and insured losses from flood events, which remain largely underinsured despite being among the costliest risks for homeowners.

In 2024, approximately $0.5 bn in private residential flood premium was written, along with $750 mn in private commercial flood business.

Though natural disasters cycle across seasons and regions in the U.S., it’s often a shocking discovery for property owners how expansive and expensive flood and water damage can be when a major storm devastates their homes, businesses and communities.

That’s because oftentimes insurance doesn’t cover what the policyholder thinks it does — or thinks it should.

Trend of gradual private flood insurance market expansion to continue

Fitch expects the trend of gradual private market expansion to continue, driven by improvements in flood mapping technology and analytics, regulatory developments, and the implementation of risk-based pricing of National Flood Insurance Program (NFIP) policies.

Flood risk is one of the most costly perils facing homeowners in the US but remains broadly underinsured. The private flood insurance market continues to grow alongside the NFIP, offering solutions that reduce the flood insurance gap.

Christopher Grimes, CFA – Senior Director at Fitch Ratings

The market has generally delivered favourable underwriting results, with direct case incurred loss ratios for residential flood below 50% in all but one year over the past five.

Most people who have flood insurance are required to have it, Beinsure noted.

Although many property owners have the option of purchasing flood insurance, it is mandated for government-backed mortgages that sit in areas that the Federal Emergency Management Agency deems highest risk. Many banks require it in high-risk zones, too.

But most private insurance companies don’t carry flood insurance, leaving the National Flood Insurance Program run by FEMA as the primary provider.

Flood insurance underwriting loss

Since private flood data became a separate line item in the Insurance Expense Exhibit (IEE) 9 years ago, the industry experienced just one underwriting loss, in 2017, caused by several landfalling hurricanes, particularly Hurricane Harvey.

In 2017, the direct combined ratio for private flood reached 188.2%, while the net of reinsurance combined ratio was 186.2%. Between 2018 and 2024, the average direct combined ratio was 60.4%.

The Private Flood Supplement has provided additional transparency into the private flood market.

Homeowners in high-risk areas who should have it sometimes decide not to get it. Someone who pays off their mortgage can drop their flood insurance once it’s not required. Or if they purchase a house or mobile home with cash, they may not opt for it at all.

The rest of us are just rolling the dice, even though experts have long warned that flooding can happen just about anywhere because flood damage isn’t just water surging and seeping into the land — it’s also water from banks, as well as mudflow and torrential rains.

NFIP’s reinsurance program

Over the past decade, the global reinsurance market has slowly increased its exposure to US flood risk through support of primary flood business and the NFIP’s reinsurance program.

A bill introduced in the U.S. Senate aims to extend the National Flood Insurance Program (NFIP) through Dec. 31, 2026. This move addresses the 32 short-term extensions the program has faced over the past decade, Beinsure noted.

The most recent extension, enacted in December 2024, is set to expire on March 14 at midnight unless Congress intervenes with new legislation or another short-term extension.

The House of Representatives passed the continuing resolution on March 11, but the Senate had not yet voted on the budget measure at the time of reporting.

Private Residential Flood vs. National Flood Insurance Program

Frequent short-term extensions undermine the NFIP’s ability

Frequent short-term extensions undermine the NFIP’s ability to serve its 4.7 mn policyholders, according to Louisiana Republican Senators Bill Cassidy and John Kennedy, who sponsored the bill.

UK reinsurers and Lloyd’s syndicates have supplied capital, underwriting, and flood modelling expertise, as well as various white-label products to MGAs, program managers, and carriers, supporting growth in recent years.

Munich Re, Swiss Re, and Hiscox have developed turnkey solutions to deliver private flood products and capital for flood programs.

What flood insurance covers

Even if a homeowner does have flood insurance, the coverage may not be enough to make a policyholder whole again.

FEMA’s National Flood Insurance Program only covers up to $250,000 for single-family homes and $100,000 for contents. Renters can get up to $100,000 for contents, and commercial flood insurance will cover up to $500,000.

There are concerns that such flooding coverage limits are not robust enough, especially at a time when climate change is making strong hurricanes even stronger and making storms in general wetter, slower and more prone to intensifying rapidly.

And what typically happens to the people without flood insurance in a major storm is that they can try to recover some money from their standard home insurance but may end up in a fight to determine what damage is or isn’t wind versus rain, or even “wind-driven rain.”

NFIP created a catastrophe reinsurance program

On the federal side, the NFIP created a catastrophe reinsurance program with annual traditional placements from private reinsurers and multi-year capital market transactions to distribute catastrophic US flood risk among global partners.

Since 2018, the NFIP has also sponsored seven catastrophe bond transactions, each with a three-year risk period through the FloodSmart Re vehicle. As of 2025, over $3 bn of reinsurance limit has been secured from capital market participants under the program.

Recent enhancements in US flood modelling and mapping have significantly improved the attractiveness of underwriting private flood products.

Some program functions, such as issuing Flood Mitigation Assistance Grants, would remain authorized, but losing key authorities could significantly impact the NFIP’s remaining activities.

In 2011, the largest carrier participating in the NFIP’s write-your-own program withdrew, citing administrative burdens from repeated short-term authorizations and lapses.

Private insurers handle the program’s policies through the WYO program.

Efforts to obtain comments from the Federal Emergency Management Agency (FEMA) and the Coalition for Sustainable Flood Insurance were unsuccessful.

Amid ongoing uncertainty and rising rates, several states are exploring alternatives to the NFIP. In January, Alaska introduced a bill proposing a state-based flood insurance program.

FAQ

The private flood insurance market shows favourable underwriting performance, with loss ratios below 50% in most years. However, it remains a small segment of the overall property and casualty insurance industry. This is partly because most flood insurance policies are still written under the federally backed National Flood Insurance Program (NFIP), which dominates the market.

Flood insurance in the US has traditionally been purchased only to meet mortgage requirements for properties in high-risk zones designated by FEMA. Outside those zones, many homeowners opt out, even though flood risk exists nationwide. Standard homeowners’ policies do not cover flood damage, leaving many underinsured.

Growth has been supported by improved flood risk analytics and mapping, new technologies, regulatory changes, and updated NFIP pricing policies. These factors have made private products more viable and competitive compared to NFIP offerings.

The gap remains wide. For example, flooding in Texas in 2025 caused estimated economic losses of $18 bn–$22 bn, while insured losses were significantly lower. Only about 4% of US homeowners carry flood insurance, and many claims come from outside designated high-risk zones.

Private residential flood policies grew at a 20% annual rate from 2020 to 2024, while NFIP policies declined. In 2024, private insurers wrote around $0.5 bn in residential flood premiums and $750 mn in commercial premiums. Private policies can offer higher limits and broader coverage, but NFIP remains the primary provider, especially in high-risk areas.

Underwriting results have been favourable in most years. Since private flood data began being tracked separately in the Insurance Expense Exhibit nine years ago, only 2017 showed an underwriting loss due to multiple hurricanes, including Harvey. The average direct combined ratio between 2018 and 2024 was about 60.4%.

The NFIP created a catastrophe reinsurance program that includes placements with private reinsurers and capital market transactions, such as catastrophe bonds. Since 2018, it has secured over $3 bn of reinsurance limit through these initiatives. However, frequent short-term program extensions in Congress have hampered its long-term planning and effectiveness.

…………………

AUTHORS: Christopher Grimes, CFA – Senior Director at Fitch Ratings, Laura Kaster, CFA – Senior Director, Risk (North and South American Financial Institutions), Credit Commentary & Research at Fitch Ratings.

Edited by Nataly Kramer — Editor at Beinsure Media.