Overview

The crypto VC landscape mirrors the broader crypto and blockchain space, marked by volatility and rapid innovation. Over the last decade, it has undergone several distinct phases. Investing in crypto has been painful this year, but the sector is moving forward in several important ways.

The crypto fundraising landscape is showing signs of recovery. In the last year, we’ve been in the same cycle in terms of sentiment, increasing capital going into the space and more developers coming and building.

According to Beinsure Data, 90 crypto & blockchain unicorn starups (>$1 bn) raised up to 2025 more than $30.2 bn venture capital with cumulative valuation ~$352 bn.

Fundraising trends have mirrored these cycles, with peaks observed in 2014, 2018, and 2022. If these historical trends continue, we anticipate another fundraising peak in 2026, aligning with the next expected major cycle in the crypto market.

After the initial-coin-offering boom in 2017, there was a recalibration where investors became more selective. A new growth cycle began in 2020, fueled by decentralized finance (DeFi) and increasing institutional interest. This led to record-breaking fundraising levels in 2021 and 2022, as the crypto ecosystem matured, especially in infrastructure development.

The crypto VC landscape has seen major fluctuations in recent years. In 2022, fundraising hit a record high at $23.7 bn, nearly doubling 2021’s total. But in 2023, it plunged by 89%, dropping to $2.6 bn.

Despite the downturn, the median fund size grew by 65.1% in 2024, reaching $41.3 mn. Midsized funds, ranging between $100 mn and $500 mn, have become more prominent, offering the flexibility needed to navigate current market challenges without the burdens of managing megafunds.

The Q4 2024 saw a stable overall level of investment, but many signs pointed to a decrease in venture capital inflows were on the way. Beinsure Media presents a Ranking of the top biggest crypto unicorns in the world by valuation for 2024.

This Crypto Companies Ranking provides an overview of major players in the cryptocurrency sector, showcasing their market valuations as of 2025. The valuations reflect the significant role these companies play in the crypto ecosystem, spanning exchanges, lending platforms, and decentralized finance (DeFi) solutions.

90 Biggest Crypto Unicorns in the World by Valuation in 2026

| № | Crypto Unicorns | Country | Valuation, $ bn | VC raised, $ mn |

| 1 | Revolut | UK | 45,0 | 1 800 |

| 2 | BITMAIN | CN | 15,0 | 765 |

| 3 | Ripple | US | 15,0 | 325 |

| 4 | OpenSea | US | 13,3 | 423 |

| 5 | Kraken | US | 10,8 | 112 |

| 6 | Alchemy | US | 10,5 | 414 |

| 7 | NEAR | US | 10,0 | 355 |

| 8 | KuCoin | SYC | 10,0 | 180 |

| 9 | Digital Currency Group | US | 10,0 | |

| 10 | Chainalysis | US | 8,6 | 537 |

| 11 | StarkWare | ISR | 8,0 | 262 |

| 12 | Fireblocks | US | 8,0 | 1 000 |

| 13 | FalconX | US | 8,0 | 427 |

| 14 | Circle | US | 7,7 | 1 100 |

| 15 | Dapper Labs | CA | 7,6 | 643 |

| 16 | Gemini | US | 7,1 | 400 |

| 17 | New York Digital Investment Group | US | 7,0 | 1 400 |

| 18 | ConsenSys | US | 7,0 | 733 |

| 19 | Ava Labs | US | 5,3 | 356 |

| 20 | Blockchain.com | UK | 5,0 | 1 200 |

| 21 | Binance US | US | 4,5 | 217 |

| 22 | Sorare | FR | 4,3 | 775 |

| 23 | Bitpanda | AT | 4,1 | 589 |

| 24 | Yuga Labs | US | 4,0 | 450 |

| 25 | Celestia | LI | 3,5 | 158 |

| 26 | MoonPay | US | 3,4 | 555 |

| 27 | Blockdaemon | US | 3,4 | 494 |

| 28 | Autograph | US | 3,2 | 205 |

| 29 | Amber Group | SG | 3,0 | 630 |

| 30 | Monad Labs | US | 3,0 | 244 |

| 31 | Anchorage Digital | US | 3,0 | 487 |

| 32 | LayerZero | CA | 3,0 | 263 |

| 33 | Immutable | AU | 2,5 | 286 |

| 34 | Blockstream | CA | 2,5 | 600 |

| 35 | WorldCoin | US | 2,5 | 240 |

| 36 | Paxos | US | 2,4 | 535 |

| 37 | Aptos Labs | US | 2,4 | 410 |

| 38 | 1inch | VGB | 2,3 | 190 |

| 39 | Story Protocol | US | 2,3 | 164 |

| 40 | Bitso | MEX | 2,2 | 332 |

| 41 | Current | US | 2,2 | 611 |

| 42 | CoinDCX | IN | 2,1 | 250 |

| 43 | Copper.co | CH | 2,1 | 329 |

| 44 | DFINITY | CH | 2,0 | 102 |

| 45 | AMINA | CH | 2,0 | 246 |

| 46 | Mysten Labs | US | 2,0 | 342 |

| 47 | LootMogul | US | 2,0 | 211 |

| 48 | CertiK | US | 2,0 | 300 |

| 49 | Sky Mavis | SG | 1,9 | 170 |

| 50 | CoinSwitch | IN | 1,9 | 302 |

| 51 | Scroll | SYC | 1,8 | 80 |

| 52 | BitGo | US | 1,8 | 188 |

| 53 | Uniswap | US | 1,7 | 178 |

| 54 | Limit Break | US | 1,7 | 190 |

| 55 | Optimism | US | 1,6 | 179 |

| 56 | CoinList | US | 1,6 | 119 |

| 57 | Magic Eden | US | 1,6 | 193 |

| 58 | Matrixport | SG | 1,5 | 167 |

| 59 | Enya Labs | US | 1,5 | 48 |

| 60 | Ledger | FR | 1,4 | 578 |

| 61 | Figment | CA | 1,4 | 165 |

| 62 | Concordium | CH | 1,4 | 46 |

| 63 | Talos | US | 1,3 | 151 |

| 64 | Betterment | US | 1,3 | 435 |

| 65 | Lukka | US | 1,3 | 261 |

| 66 | CoinTracker | US | 1,3 | 104 |

| 67 | iTrustCapital | US | 1,3 | 125 |

| 68 | Hashkey Group | HK | 1,3 | 100 |

| 69 | Nova Labs | US | 1,3 | 251 |

| 70 | Zyber 365 | UK | 1,2 | 100 |

| 71 | Offchain Labs | US | 1,2 | 144 |

| 72 | Phantom | US | 1,2 | 118 |

| 73 | Quantstamp | US | 1,1 | 147 |

| 74 | EigenLayer | US | 1,1 | 165 |

| 75 | Sentz Global | US | 1,1 | 114 |

| 76 | VNLIFE | VIE | 1,0 | 550 |

| 77 | Polyhedra Network | SG | 1,0 | 45 |

| 78 | Dune Analytics | NOR | 1,0 | 79 |

| 79 | io net | US | 1,0 | 35 |

| 80 | BitFury | NL | 1,0 | 140 |

| 81 | Bitget | ZA | 1,0 | 30 |

| 82 | Humanity Protocol | US | 1,0 | 30 |

| 83 | Andalusia Labs | US | 1,0 | 51 |

| 84 | Injective | US | 1,0 | 53 |

| 85 | Farcaster | US | 1,0 | 180 |

| 86 | Gauntlet | US | 1,0 | 45 |

| 87 | Unstoppable Domains | US | 1,0 | 70 |

| 88 | Forte | US | 1,0 | 952 |

| 89 | Mythical Games | US | 1,0 | 320 |

| 90 | Flashbots | KY | 1,0 | 62 |

| 90 | Axelar | CA | 1,0 | 64 |

Leading crypto unicorns globally

This list highlights the leading crypto unicorns globally, showcasing their valuations and brief descriptions of their operations and services.

The cryptocurrency industry continues to expand rapidly, attracting substantial investments and reaching new heights in valuation. The cryptocurrency and blockchain has witnessed growth in 2025, driven by substantial venture capital investments

Emerging managers continue to lead the crypto VC space, capitalizing on their specialized expertise in areas like “tokenomics” and governance. However, first-time funds have dropped from 58% in 2020 to 45.8% in 2024, indicating a more cautious approach to market entry.

Fundraising timelines have extended, reflecting growing caution among investors. Both the time between raises and the duration to close funds have lengthened, suggesting a challenging future for fundraising. LPs are becoming more selective and risk-averse due to recent market downturns.

90 Largest Crypto Unicorns by Venture Capital Raised up to 2026

| № | Company | Country | VC raised, $ mn | Valuation, $ bn |

| 1 | Robinhood | USA | 5 600 | 32,0 |

| 2 | Revolut | UK | 1 800 | 45,0 |

| 3 | New York Digital Investment Group | US | 1 400 | 7,0 |

| 4 | Blockchain com | UK | 1 200 | 5,0 |

| 5 | Circle | US | 1 100 | 7,7 |

| 6 | Fireblocks | US | 1 000 | 8,0 |

| 7 | Forte | US | 952 | 1,0 |

| 8 | Sorare | FR | 775 | 4,3 |

| 9 | BITMAIN | CN | 765 | 15,0 |

| 10 | ConsenSys | US | 733 | 7,0 |

| 11 | Dapper Labs | CA | 643 | 7,6 |

| 12 | Amber Group | SG | 630 | 3,0 |

| 13 | Current | US | 611 | 2,2 |

| 14 | Blockstream | CA | 600 | 2,5 |

| 15 | Bitpanda | AT | 589 | 4,1 |

| 16 | Ledger | FR | 578 | 1,4 |

| 17 | MoonPay | US | 555 | 3,4 |

| 18 | VNLIFE | VIE | 550 | 1,0 |

| 19 | Chainalysis | US | 537 | 8,6 |

| 20 | Paxos | US | 535 | 2,4 |

| 21 | Blockdaemon | US | 494 | 3,4 |

| 22 | Anchorage Digital | US | 487 | 3,0 |

| 23 | Yuga Labs | US | 450 | 4,0 |

| 24 | Betterment | US | 435 | 1,3 |

| 25 | FalconX | US | 427 | 8,0 |

| 26 | OpenSea | US | 423 | 13,3 |

| 27 | Alchemy | US | 414 | 10,5 |

| 28 | Aptos Labs | US | 410 | 2,4 |

| 29 | Gemini | US | 400 | 7,1 |

| 30 | Ava Labs | US | 356 | 5,3 |

| 31 | NEAR | US | 355 | 10,0 |

| 32 | Mysten Labs | US | 342 | 2,0 |

| 33 | Bitso | MEX | 332 | 2,2 |

| 34 | Copper co | CH | 329 | 2,1 |

| 35 | Ripple | US | 325 | 15,0 |

| 36 | Mythical Games | US | 320 | 1,0 |

| 37 | CoinSwitch | IN | 302 | 1,9 |

| 38 | CertiK | US | 300 | 2,0 |

| 39 | Immutable | AU | 286 | 2,5 |

| 40 | LayerZero | CA | 263 | 3,0 |

| 41 | StarkWare | ISR | 262 | 8,0 |

| 42 | Lukka | US | 261 | 1,3 |

| 43 | Nova Labs | US | 251 | 1,3 |

| 44 | CoinDCX | IN | 250 | 2,1 |

| 45 | AMINA | CH | 246 | 2,0 |

| 46 | Monad Labs | US | 244 | 3,0 |

| 47 | WorldCoin | US | 240 | 2,5 |

| 48 | Binance US | US | 217 | 4,5 |

| 49 | LootMogul | US | 211 | 2,0 |

| 50 | Autograph | US | 205 | 3,2 |

| 51 | Magic Eden | US | 193 | 1,6 |

| 52 | Limit Break | US | 190 | 1,7 |

| 53 | 1inch | VGB | 190 | 2,3 |

| 54 | BitGo | US | 188 | 1,8 |

| 55 | KuCoin | SYC | 180 | 10,0 |

| 56 | Farcaster | US | 180 | 1,0 |

| 57 | Optimism | US | 179 | 1,6 |

| 58 | Uniswap | US | 178 | 1,7 |

| 59 | Sky Mavis | SG | 170 | 1,9 |

| 60 | Matrixport | SG | 167 | 1,5 |

| 61 | Figment | CA | 165 | 1,4 |

| 62 | EigenLayer | US | 165 | 1,1 |

| 63 | Story Protocol | US | 164 | 2,3 |

| 64 | Celestia | LI | 158 | 3,5 |

| 65 | Talos | US | 151 | 1,3 |

| 66 | Quantstamp | US | 147 | 1,1 |

| 67 | Offchain Labs | US | 144 | 1,2 |

| 68 | BitFury | NL | 140 | 1,0 |

| 69 | iTrustCapital | US | 125 | 1,3 |

| 70 | CoinList | US | 119 | 1,6 |

| 71 | Phantom | US | 118 | 1,2 |

| 72 | Sentz Global | US | 114 | 1,1 |

| 73 | Kraken | US | 112 | 10,8 |

| 74 | CoinTracker | US | 104 | 1,3 |

| 75 | DFINITY | CH | 102 | 2,0 |

| 76 | Zyber 365 | UK | 100 | 1,2 |

| 77 | Hashkey Group | HK | 100 | 1,3 |

| 78 | Scroll | SYC | 80 | 1,8 |

| 79 | Dune Analytics | NOR | 79 | 1,0 |

| 80 | Unstoppable Domains | US | 70 | 1,0 |

| 81 | Axelar | CA | 64 | 1,0 |

| 82 | Flashbots | KY | 62 | 1,0 |

| 83 | Injective | US | 53 | 1,0 |

| 84 | Andalusia Labs | US | 51 | 1,0 |

| 85 | Enya Labs | US | 48 | 1,5 |

| 86 | Concordium | CH | 46 | 1,4 |

| 87 | Polyhedra Network | SG | 45 | 1,0 |

| 88 | Gauntlet | US | 45 | 1,0 |

| 89 | io net | US | 35 | 1,0 |

| 90 | Humanity Protocol | US | 30 | 1,0 |

| 90 | Bitget | ZA | 30 | 1,0 |

This table highlights the substantial venture capital investments driving the growth and innovation within the cryptocurrency and blockchain industry.

The fundraising environment will remain difficult as the market continues to recover. Some fund managers may need to liquidate token holdings at lower values.

Without substantial returns to LPs, seasoned crypto investors are expected to maintain a cautious stance, while newer LPs may be drawn to trending sectors like restaking or the intersection of crypto and AI.

Reflecting on venture capital activity, while it hasn’t returned to the peak levels of 2022, the landscape is looking better compared to last year. As of July 30, 2024, $2.2 bn has been raised across 24 funds, putting it on track to surpass 2023’s total.

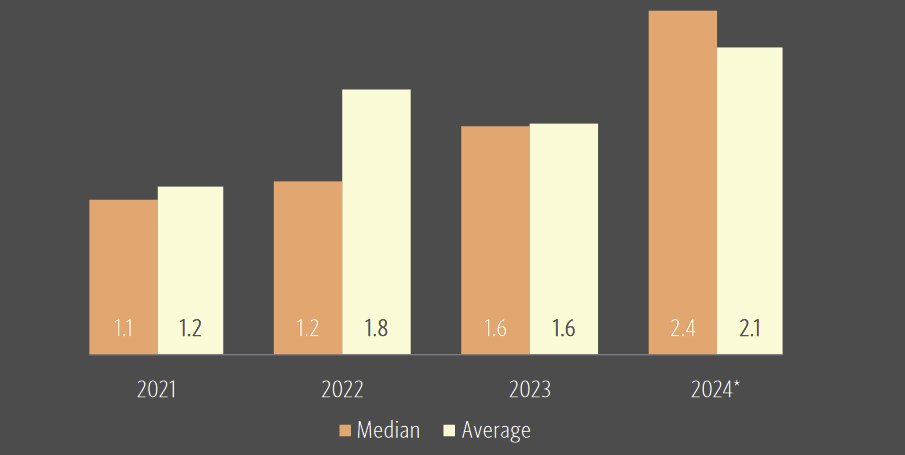

Median and average time between crypto VC funds

From 2021 to 2024, the time between fundraises has steadily increased, with the median time between funds more than doubling from 1.1 years to 2.4 years. This lengthening period suggests that fund managers are taking longer to return to market, likely due to spending more time with their portfolios and deploying capital much slower during the crypto bear market.

FAQ: Crypto Venture Capital Landscape Insights

The crypto VC landscape has undergone distinct phases, marked by peaks in 2014, 2018, and 2022. The initial coin offering boom in 2017 led to recalibration and selective investments. A new growth cycle began in 2020, driven by decentralized finance (DeFi) and institutional interest, culminating in record-breaking fundraising in 2021 and 2022.

Fundraising hit a record high of $23.7 bn in 2022, nearly doubling 2021’s total. However, it plunged by 89% to $2.6 bn in 2023. Despite this, the median fund size grew by 65.1% in 2024, reaching $41.3 mn, with midsized funds gaining prominence.

Fundraising timelines have lengthened, with the median time between funds increasing from 1.1 years in 2021 to 2.4 years in 2024. Managers are deploying capital more slowly and spending more time with their portfolios, reflecting a cautious approach in the crypto bear market.

According to Beinsure, Revolut leads with a $45 bn valuation and $1.8 bn VC raised. Other top unicorns include BITMAIN ($15 bn valuation, $765 mn VC raised) and Ripple ($15 bn valuation, $325 mn VC raised).

Institutional interest has driven growth in infrastructure development and DeFi, resulting in significant fundraising cycles. However, investors have become more cautious, leading to extended fundraising timelines and a focus on midsized funds for flexibility.

Emerging managers dominate the space, leveraging expertise in areas like tokenomics and governance. However, first-time funds have dropped from 58% in 2020 to 45.8% in 2024, reflecting a cautious stance among LPs due to market volatility and downturns.

Venture capital activity is gradually improving, with $2.2 bn raised across 24 funds as of July 30, 2024. This puts the market on track to surpass 2023’s total, showing signs of recovery despite a challenging fundraising environment.

………………

Edited by Peter Sonner – lead tech editor at Beinsure Media

Fact-checked by Oleg Parashchak – CEO Finance Media & Editor-in-Chief at Beinsure Media and Insurance TOP Ratings (25+ years of professional experience in Rankings, Insurance & Media).