Overview

U.S. individual life insurance premium is on track to reach a record $16 bn in 2024 and continue growing in the current year, as the market continues riding a bounce first seen during the COVID-19 pandemic, according to LIMRA Report. Beinsure Media has selected the most important points from the report.

Market conditions are very favorable for the individual life insurance market. In 2024, we expect total premium to be level with or above the record set in 2023 (up 1% to 5%).

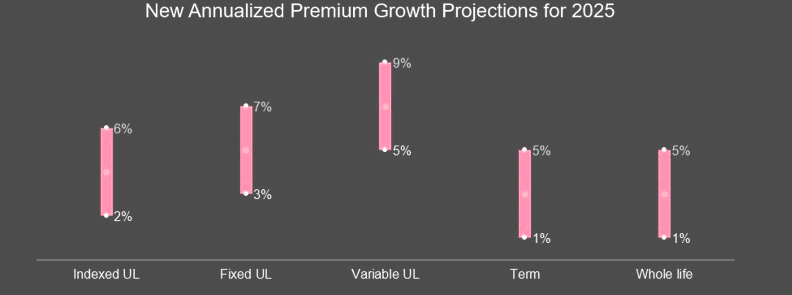

While there may be shifts in the product mix, LIMRA is forecasting 2025 sales growth to improve — increasing between 2% and 6%.

Key Takeaways

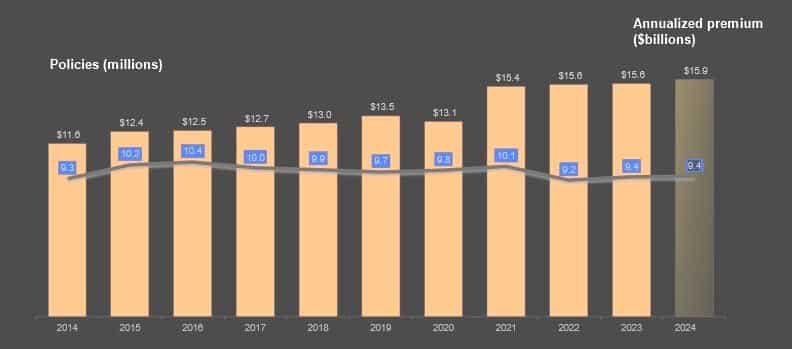

- U.S. individual life insurance premiums are expected to reach $16 bn in 2024, marking the fourth consecutive year of record-high new premiums.

- Rising equity markets, low inflation, and reduced unemployment continue to support growth in life insurance and annuity sales.

- Despite challenges from high interest rates, whole life (WL) and term life sales are forecasted to grow by 1%-5% in 2025 as market conditions stabilize.

- Variable universal life (VUL) is set to grow 12%-16% in 2024, driven by equity market gains, while indexed universal life (IUL) growth is bolstered by simplified products with low face amounts.

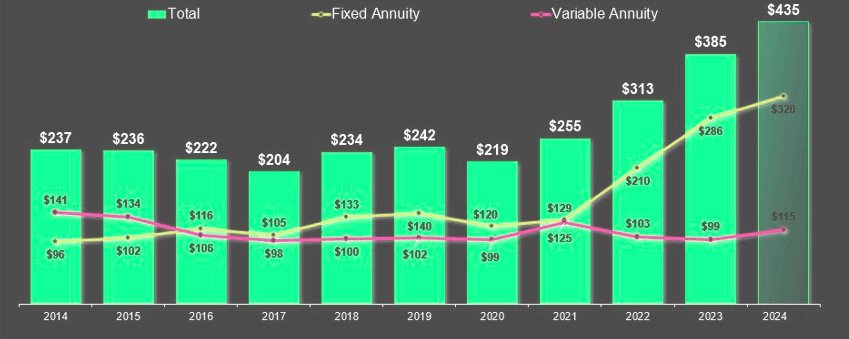

- Retail annuity sales are projected to exceed $430 bn in 2024, reflecting a 10%-15% increase over 2023, despite expected declines in 2025 due to falling interest rates.

Following solid third quarter results and strong preliminary October sales figures, LIMRA expects 2024 will mark the fourth year of record-high new premium collected for the industry. Barring an unforeseen economic downturn, LIMRA is forecasting life sales to grow in 2025.

While interest rates are dropping, the decline may not be as severe as anticipated and reduced rates could relieve pressure on indexed universal life and whole life, according to Global Economic and Insurance Market Outlook.

The group is forecasting rising equity markets, coupled with lower inflation and unemployment, will be tailwinds for the industry this year.

Interest rates have had a negative impact on WL sales and rising interest rates have shifted sales toward products with longer premium payment periods. LIMRA is forecasting WL sales to decline through year-end 2024 and grow by 1% to 5% in 2025 as the yield curve reverts to normal.

U.S. Life Insurance Sector Trends

After dropping 5% in 2022, term life sales rebounded the following years driven by digital platform expansions and competitive pricing. Premium will remain level in 2024 and grow 1% to 5% in the full year 2025, LIMRA said.

Whole life and term are often considered the core of the life insurance business. These products have represented more than 85% of the policies sold and a majority of the new premium collected each year,

“While recent higher interest rates have had a negative impact on whole life sales and inflation has likely dampened the term sales a bit, LIMRA expects both product lines to grow in 2025,” says John Carroll, senior vice president and head of life and annuities, LIMRA and LOMA.

U.S. Retaile Life Insurance Sales

Variable Universal Life and Market Diversification

Strong stock market growth propelled variable universal life in recent years. LIMRA is predicting growth of 12% to 16% in 2024 and 2025 will see VUL growth of 5% to 9% assuming continued equity market increases.

The VUL market has undergone substantive changes in recent years. In 2023, just a few carriers were driving most of the sales.

Bryan Hodgens, senior vice president and head of LIMRA Research

In 2024, as equity markets continued to rise, we started to see more companies selling VUL products, particularly protection-focused products, with death benefit guarantees.

The interest rate environment “significantly” shifted the indexed universal life market and split it into two segments: Traditional IUL carriers and distributors, which experienced a decline in premiums over the past few years; and carriers and distributors with a focus on simplified products with a low face amount, which have seen success.

2025 Individual Life Insurance Growth Forecast

After years of declining premium attributed to falling interest rates, fixed universal life premium sales started to rebound in late 2023 and into 2024. LIMRA is calling for FUL sales to be up 8% to 12% for 2024 and to moderate in 2025 with growth of 2% to 6%.

Whole life (WL) sales continue to struggle under higher interest rates as consumers move to products with potentially better returns. Should the yield curve return to normal next year, we expect WL sales to improve in 2025.

Whole life insurance new premium represented 34% of the total life insurance market.

Indexed universal life (IUL) new premium was $882 mn in the third quarter, up 2% from the prior year. Life insurers reporting increases attributed the growth to expanded distribution, product innovation and higher consumer demand. Policy count grew 9%. In the first nine months of 2024, IUL new premium improved 1% to $2.7 bn, and the number of policies sold increased 11%.

U.S. Retail Annuity Insurance Sales

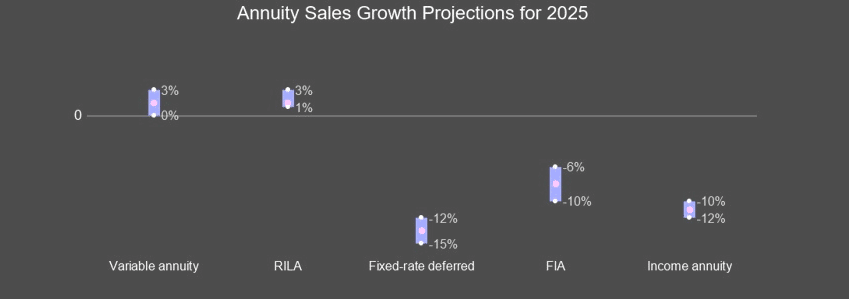

U.S. retail annuity sales are projected to surpass $1.1 tn from 2022 to 2024. However, fixed-rate deferred (FRD) and fixed indexed annuities (FIA) sales may decline in 2025 as interest rates fall, according to LIMRA.

LIMRA estimates 2024 annuity sales to exceed $430 bn, a 10%-15% increase over 2023. However, sales are expected to drop in 2025, returning to $364-$410 bn.

Favorable market conditions and demographics continue to support annuity growth. Rising rates fueled significant gains in 2023 and 2024, but declining rates in 2025 will slow the expansion of fixed annuity products.

Annual U.S. Annuity Sales

Despite this decline, annuity sales will remain over 50% higher than pre-pandemic levels, reflecting investors’ growing preference for protection-based retirement solutions. FRD sales, which represented more than 40% of the annuity market in 2023, are projected to reach $160 bn in 2024.

2025 Individual Life Insurance Growth Forecast

It will be a mixed outlook in 2025 for the overall annuity market. While market conditions and demographics are very favorable for the annuity market, a decline in interest rates (which propelled the remarkable growth in 2023 and 2024) will undercut fixed annuity products continued growth. For 2024, we expect sales to be more than $430 bn, up between 10% to 15% over 2023.

Retail Annuity Falling Rates

Falling rates will reduce demand, but maturing contracts could lead to reinvestment in FRD products. LIMRA expects FRD sales to decrease by 15%-25% in 2025, totaling $122-$147 bn.

FIA sales are set to hit a record $120 bn in 2024, nearly double the 2021 figure. While sales are forecasted to decline by 5-10% in 2025, they will remain above $100 bn.

Meanwhile, registered index-linked annuity (RILA) sales will see their 11th consecutive year of growth in 2024, driven by strong equity markets.

LIMRA projects RILA sales to stay at or above 2024 records, reaching $62-$66 bn in 2025. John Carroll, senior vice president of LIMRA and LOMA, highlighted investor demand for products offering downside protection and growth potential. Seven new carriers entered the RILA market in 2024, enhancing offerings with competitive index caps and participation rates.

Traditional Variable Annuity Sales

Traditional variable annuity sales rebounded in 2024, recovering from record lows in 2023. Double-digit equity market growth, product innovation, and increased interest from registered investment advisers pushed sales to $60 bn in 2024, with similar levels expected in 2025.

Income annuity sales are projected to reach $18 bn in 2024. However, lower interest rates will prompt carriers to reduce payout rates, potentially cutting 2025 sales by 10%, bringing totals to $16-$18 bn.

U.S. individual life insurance premiums are on track to hit $15.9 bn in 2024, continuing the growth momentum established during the COVID-19 pandemic.

U.S. Single-Premium Pension Risk Transfer

Total U.S. single-premium pension risk transfer (PRT) premium was $14.2 bn in the third quarter, up 36% from prior year’s results. Year-to-date (YTD), total single-premium PRT premium increased 21% to $39.9 bn.

While new premium growth rebounded in the third quarter, the growth can be attributed to larger deal activity. The bigger story continues to be the expansion of the PRT market. Life insurers reported the largest number of contracts ever sold in the first nine months of the year.

Higher interest rates are driving companies to de-risk their pension liabilities to annuity providers. LIMRA expects this trend to continue through the rest of the year.

Single-premium buy-out premium totaled $18 bn, up 62% from prior year’s results. There were 203 contracts finalized in the third quarter, level with prior year. YTD buy-out premium jumped 26% to $36.5 bn.

Through 2024, there were 750 buy-out contracts, 10% growth over prior year. This marks a record-high number of buy-out contracts sold.

Single-premium buy-in premium was $1 bn, falling 56% from 2023. YTD, buy-in premium totaled $3.3 bn, down 15% year over year.

Through 2024, there were nine buy-in contracts sold, one more sold than prior year (representing a 13% increase).

Single premium buy-out assets reached $288.8 bn through the third quarter, up 13% from the prior year. Single premium buy-in assets were $9.1 bn YTD, 11% higher than the same period in 2023.

Combined, single premium assets were $298 bn, an increase of 15% year over year.

A group annuity risk transfer product, such as a pension buy-out product, allows an employer to transfer all or a portion of its pension liability to an insurer. In doing so, an employer can remove the liability from its balance sheet and reduce the volatility of the funded status.

FAQ

Growth is fueled by rising equity markets, low inflation, and declining unemployment. The post-COVID-19 economic recovery also plays a key role.

High interest rates have negatively impacted whole life sales, but declining rates are expected to relieve pressure on indexed universal life (IUL) and whole life products.

Term life premiums will remain stable in 2024 and grow by 1%-5% in 2025, supported by digital platforms and competitive pricing.

VUL sales are expected to grow 12%-16% in 2024 and 5%-9% in 2025, driven by market expansion and protection-focused product innovations.

Annuity sales will rise 10%-15% to $430 bn in 2024 but may decline to $364-$410 bn in 2025 as interest rates fall.

Simplified IUL products with low face amounts and expanded distribution are driving growth, with premiums reaching $2.7 bn in the first nine months of 2024.

PRT premiums hit $39.9 bn YTD in 2024, with buy-out contracts reaching record highs due to companies de-risking their pension liabilities amidst high interest rates.

……………..

AUTHOR: John Carroll – senior vice president and head of life and annuities, LIMRA and LOMA, Bryan Hodgens – senior vice president and head of LIMRA Research