Overview

- Swiss Re Institute key insurance market forecasts

- Macroeconomic trends for the US economy

- Macroeconomic trends for the euro area economy

- Global primary insurance markets

- Global total insurance industry premium real growth rates and forecasts

- The global life insurance industry is buoyant

- Financial stability and debt sustainability risks

The global economy is poised for further solid expansion. We forecast global real GDP growth at 2.8% in 2025 and 2.7% in 2026, roughly in line with 2024. However, the distribution of risks is tilted to the downside, driven by geopolitical risk, the potential for disruptive policy changes, and financial market vulnerabilities. Growing divergence between regions will likely be accentuated by the policy direction of the next US government, according to Swiss Re Institute report.

We continue to view inflation as the number one macro risk, and we expect it to stay sticky, even if headline inflation declines rapidly next year. It brings downside risks to growth from higher central bank interest rates.

In advanced markets we forecast real GDP growth of just 0.4% in 2024, the lowest since the 1980s outside of the global financial and COVID-19 crises. In emerging markets, we anticipate substantially lower growth rates than pre-pandemic that will likely feel akin to recession.

The proposals from President-elect Trump’s campaign have mixed implications for the US economy that will ultimately depend on their extent and sequencing, but we anticipate slower disinflation and a shallower interest rate easing cycle now.

We maintain our view that the US will continue its economic trend of outperformance, even if momentum will slow sequentially.

This will contrast increasingly with the euro area and China, which face headwinds from trade tensions and structural challenges.

Swiss Re Institute key insurance market forecasts

Note: F = forecasts. World GDP consensus forecast comes from the IMF (based on market exchange rates).

We forecast global CPI inflation to decline slowly to an average 3.3% in 2025 and 3.0% in 2026, from 5.1% in 2024.

In response, a cautious US Federal Reserve will likely proceed with only three interest rate cuts in 2025, while central banks in the euro area and China ease policy faster as economic growth concerns dominate. However, fiscal risks may add upside pressure to long-dated bond yields in the West.

Long term, our “five D” structural themes of deglobalisation, decarbonisation, demographics, digitalisation and debt will shape the outlook.

The world economy is set to slow

We expect the global economy to slow in 2025 due to cumulative monetary policy tightening and fading growth impulses from 2023. The Middle East conflict increases risks to this outlook.

Major economies diverge: the US continues to grow, Europe stagnates, and China faces structural growth challenges.

We forecast 2.2% global real GDP growth in 2024, rebounding to 2.7% in 2025, driven by lower inflation and interest rates. However, inflation and interest rates in developed markets will likely remain higher than previously anticipated, with risks skewed to the upside.

We expect global CPI inflation to moderate to 5.1% in 2024 and 3.4% in 2025, though price pressures will remain volatile.

Slower disinflation increases the cost to economic output and the risk of prolonged stagnation. A sharp rise in long-term US bond yields this autumn signals a regime shift, leading to higher yield forecasts. Higher real interest rates may expose fragilities in public and private debt.

Macroeconomic trends for the US economy

Swiss Re foresee growing risks of an adverse economic shift driven by geopolitical or financial disruptions. Escalating geopolitical tensions, such as a disruptive trade war, or sudden spikes in US Treasury risk premia could trigger two key adverse scenarios:

- (i) renewed supply shocks

- or (ii) a global recession.

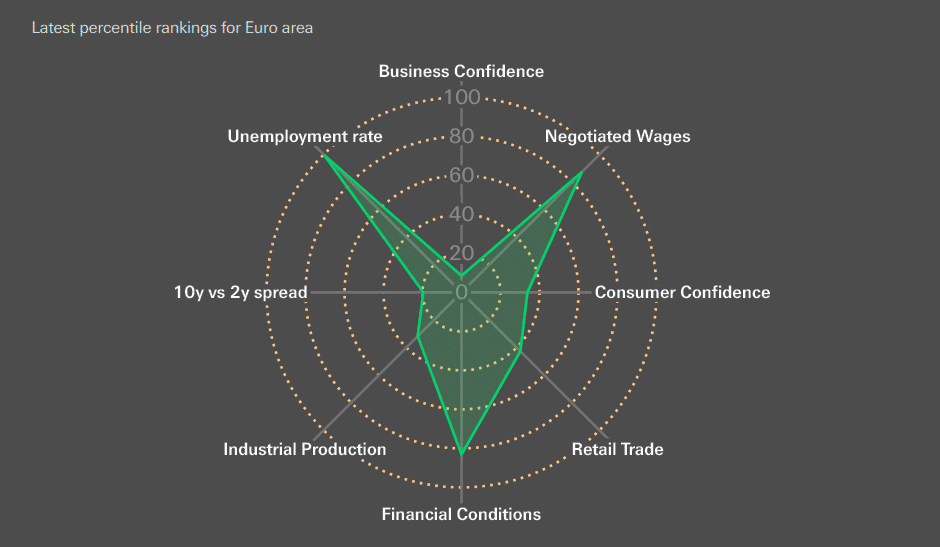

Macroeconomic trends for the euro area economy

Swiss Re macro radar charts reflect the percentile ranks of respective economic indicators using historic monthly data since 1990. Higher percentile ranks reflect stronger data relative to history, while lower percentile ranks reflect weakness. The unemployment rate has been inverted. Financial conditions indices are sourced from Bloomberg, with a higher value indicating accommodative conditions.

The “renewed supply shock” scenario involves stagflation, marked by accelerating inflation and weak economic growth. This would pressure non-life insurers with low real premium growth and increased claims severity. Asset portfolios would suffer mark-to-market losses.

In a “global recession” scenario, broad declines in insurance demand would hurt profitability, especially in exposed business lines. Widening credit spreads, falling interest rates, and declining asset values would further weaken investment returns. We also track an upside “productivity revival” scenario driven by tech-related investments, though we assess its probability as lower than the combined risk of the downside scenarios.

Global primary insurance markets

Global primary insurance markets are expected to maintain above-trend growth through 2025 and 2026. We project total global real premium growth to average 2.6% annually over these two years. This is lower than the 4.6% growth expected in 2024 but above the 1.6% annual average from 2019 to 2023.

Factors such as steady economic growth, resilient labor markets, rising real incomes as inflation eases, and elevated long-term interest rates will drive demand.

The non-life insurance sector is strengthening its profitability and sustainability. Easing inflation and higher premium rates have supported underwriting results in 2024, a trend expected to continue through 2025 and 2026. Combined with improving investment returns, these factors should sustain profitability across the industry.

Global total insurance industry premium real growth rates and forecasts

P&C insurance profitability, 2021‒2026F, % of net premiums earned, ROE and cost of capital, in % of capital

We expect decade-high 4.3% global non-life premium growth this year following the repricing of risk in response to elevated claims.

Premium rates are now moderating and we forecast softer global premium growth of 2.3% annually in real terms over 2025-26, below the 3.1% average of the last five years. The active US hurricane season is likely to take global natural catastrophe insured losses to well over USD 100 bn this year for a fifth consecutive year and may delay the onset of softer property insurance pricing.

The global life insurance industry is buoyant

We project growth of more than twice the historical average, at 3% in real terms over 2025 and 2026, after a decade-high 5% growth in 2024. Total global life insurance premiums should reach $4.8 trillion by 2035, up from $3.1 trillion in 2024, driven by higher interest rates. US individual annuity sales should reach a new record of over $400 bn this year.

Evolution of life insurance saving and risk premiums in volume (USD bn), left axis, and real growth (%), right axis

As monetary policy loosens, we expect fixed rate annuity sales growth to slow and the focus to shift to indexed annuities. Pension de-risking offers another long-term tailwind for the life insurance industry, with potentially over $300 bn of bulk annuity transfers in the UK and US in the next three years.

Demand for risk protection is less interest rate-driven and we expect steady growth. Primary life insurance has a positive profitability outlook in 2025 and 2026, due to still elevated fixed-income yields. Lapse risk is contained, with declining sensitivity to interest rates as central banks lower interest rates.

Dominant role for (geo)politics in driving the macroeconomic outlook

Geopolitics will impact the outlook. The war in Israel introduces new, potentially unpredictable risks, with energy price shocks being a key risk to the global economy.

An expanded conflict involving major regional oil producers could add 2.4 percentage points to global inflation.

Assertive industrial policies are emerging, with long-term implications. Major government initiatives to boost sectors like semiconductors and clean energy may increase inflation, fiscal deficits, and interest rates.

The insurance industry can benefit from growth in commercial lines like liability, property, engineering, trade credit, and surety as these initiatives develop.

Geopolitical dampen the insurance outlook

The economic slowdown and geopolitical uncertainty are affecting the primary insurance industry’s outlook, according to World Insurance Industry report.

We predict global real premium growth to average 2.2% annually over the next two years. This is lower than the pre-pandemic trend of 2.8% but higher than the past five years’ average of 1.6%.

Profitability is improving, and underwriting gaps are closing as investment returns rise with high interest rates. However, the industry might not meet its cost of capital in major markets in 2024 or 2025. Events like the Middle East war could impact insurers’ capital due to inflation and market volatility.

Claims dynamics are a key concern in non-life insurance

For the insurance industry, we expect the macro environment of higher interest rates, insurance market rate hardening and scarce capital to be a very positive catalyst over 2023-2024; these drivers should strengthen medium-term investment results and profitability.

In our view, the global economy will cool down noticeably under the weight of inflation and interest rate shocks. The repricing of risk in the real economy and financial markets is actually healthy and a long-term positive.

Jerome Jean Haegeli, Group Chief Economist, Swiss Re

In today’s challenging times – and for the economic recovery ahead – the insurance industry can show its value as it provides financial resilience.

We anticipate significant rate hardening in 2024 and potentially some years after in response to high inflation and global natural catastrophe and financial market losses this year. Global premium growth is forecast at 2.1% in real terms annually on average over 2023 and 2024.

Financial stability and debt sustainability risks

This year we add debt and its related risks, as a fourth dimension to the “3D” set of long-term economic drivers we identified last year. As central banks unwind unconventional monetary policies, it is exposing financial vulnerabilities that have built up over the past decade.

Debt, and specifically whether governments can sustain public spending commitments in the face of higher interest rates, is a key concern. We see a risk that market shocks accumulate and fuse into financial instability.

Central banks face competing priorities of price stability, financial stability and enabling governments to pursue looser fiscal policy. This creates a risk of real interest rates being repressed in the longer term, either through higher inflation or eventually lower nominal interest rates, to manage debt sustainability or financial stability concerns.

If so, we see inflation likely being higher and more volatile. Addressing demand-side drivers of inflation with supply-side or productivity-enhancing policies and investments would help ease this tension.

Inflation still a concern, but higher interest rates a tailwind for insurers

Inflation remains the number one industry concern. We forecast high inflation in cost components relevant for insurers, such as construction and healthcare that suggests insurers’ claims and costs could rise markedly in 2022 and 2023, even without considering changes in claims frequency and natural catastrophe activity.

However, higher interest rates should be a silver lining as inflation pressure abates in 2023 and 2024.

Insurance premium forecasts, global regions

In non-life insurance, slowing global growth and inflation will likely cut real premium growth to below 1% this year, with a recovery as inflation eases and the hard market goes on.

Global non-life insurance return on equity (ROE) is expected to be lower in 2024 as underwriting performance and investment results are weaker, but rebound to a 10-year high in 2024 as the interest rate tailwind and potential rate hardening take effect.

In life insurance, we forecast a 1.9% contraction in global premiums in real terms in 2023 as consumers face cost-of-living pressure, but a return to trend growth in 2023 and 2024, carried by emerging markets. Life profitability is improving due to rising interest rates and normalising COVID-19 mortality claims.

Non-life claims are in focus, life insurance premiums are recovering

Global non-life insurance is facing challenging claims dynamics, with rising claim frequency and severity despite declines in economic inflation. The rapid growth in claims in the liability line is making these risks harder to insure.

We estimate that natural catastrophe insured losses will reach $100 bn in 2023 for the fourth consecutive year and the sixth year since 2017 (adjusted for inflation). We expect hard market conditions to persist at least through 2024.

In the Property and Casualty (P&C) segment, we estimate global real premium growth of 3.4% in 2023, which is stronger than our forecast for 2024-2025 (2.6%). This reflects significant risk repricing, especially in lines impacted by claims.

We expect health premiums to return to growth at 1.5% in 2024-2025. In life insurance, higher interest rates are increasing demand for savings products, supporting bulk annuity transfers, and boosting profitability in 2024 and 2025.

We forecast an average life premium growth of 2.3% for 2024-2025. Our forecast for life savings market growth over the next decade is significantly higher than in the past 20 years.

FAQ

Swiss Re forecasts global real GDP growth at 2.8% in 2025 and 2.7% in 2026. These projections are in line with 2024 growth levels. However, risks are skewed to the downside due to geopolitical tensions, potential disruptive policies, and financial vulnerabilities.

Inflation remains a top macroeconomic risk, especially with higher central bank interest rates aiming to curb it. Despite efforts, inflation is expected to stay sticky, particularly impacting costs in sectors like construction and healthcare, which are crucial for insurers managing claims.

Geopolitical tensions, such as the war in Ukraine and the Middle East, create unpredictable risks, including potential energy price shocks. These could add to global inflation and slow economic recovery, affecting sectors like insurance that rely on stable macroeconomic conditions.

While inflation pressures increase claims costs, higher interest rates provide a silver lining for insurers by improving investment returns. This trend supports profitability, especially for life insurance, where rising rates boost demand for savings products and annuities.

Global insurance premiums are expected to grow at an average annual rate of 2.1% in real terms for 2024. However, growth varies across segments: non-life insurance is set to see slower growth, while life insurance may benefit from increased demand for savings products.

Insurers are likely to pass some costs onto customers through premium rate increases. In non-life insurance, rate hardening is expected to continue, especially in lines like liability and property, where claims frequency and severity are on the rise.

High public and private debt levels create financial stability risks, especially as central banks unwind past monetary policies. Rising interest rates may expose debt vulnerabilities, potentially impacting financial markets and posing challenges for insurers managing investment portfolios.

The primary risks include geopolitical tensions, disruptive trade policies, and financial market vulnerabilities. Inflation remains the top macroeconomic concern, with sticky inflation likely to lead to prolonged higher interest rates by central banks. Additionally, rising bond yields signal financial fragility.

Swiss Re expects real GDP growth in advanced markets to reach just 0.4% in 2024 — the lowest since the 1980s, excluding the global financial crisis and COVID-19. Emerging markets will see slower-than-usual growth, feeling similar to a recession compared to pre-pandemic levels.

Swiss Re projects global CPI inflation to decline to 3.3% in 2025 and 3.0% in 2026, down from 5.1% in 2024. The US Federal Reserve is expected to proceed with three interest rate cuts in 2025. Meanwhile, central banks in Europe and China are likely to ease policies more aggressively due to slower economic growth.

The US economy is expected to maintain growth, though at a slower pace. In contrast, Europe is likely to stagnate, and China will face structural challenges. This divergence will be influenced by policies of the next US government and ongoing trade tensions.

Global primary insurance markets are expected to grow above-trend in 2025 and 2026, with an average real premium growth of 2.6% annually. Non-life insurance is improving profitability due to easing inflation and higher premium rates. However, global premium growth will soften to 2.3% over 2025-26, driven by moderating risk repricing and economic headwinds.

Life insurance premiums are forecast to grow at 2.3% annually over 2024-2025, driven by demand for savings products. Non-life insurance premiums are expected to grow at 3.4% in 2023, with slightly lower growth projected for 2024-2025 as inflation pressures ease.

Geopolitical risks, such as the ongoing conflict in the Middle East, pose significant risks to the global economy. Energy price shocks from expanded conflicts could add 2.4 percentage points to global inflation. On the positive side, industrial policies focused on clean energy and semiconductors present growth opportunities for commercial insurance lines like liability, property, and trade credit.

……………………..

AUTHORS: Fernando Casanova Aizpun – Senior Economist Swiss Re Institute, Li Xing – Head Insurance Market Analysis Swiss Re Institute, Roman Lechner – P&C Economic Research Lead Swiss Re Institute, Rajeev Sharan – Senior Economist Swiss Re Institute, James Finucane – Senior Economist of the Swiss Re Institute for the Americas