Overview

Geopolitical tensions and higher inflation have led to economic concern in recent years. Swiss Re Institute’s annual World Insurance sigma report finds that the global economy has remained remarkably resilient, setting the scene for growth and improved profitability across the insurance industry.

The global insurance industry has reached a new equilibrium after the challenges of recent years. The global economy has surprised on the upside, which should drive more demand for insurance.

The life sector in particular is one to watch as higher interest rates drive investment income and consumer demand for annuities, giving more people secure retirement incomes.

Population changes due to immigration reveal deeper weaknesses in some advanced markets, affecting real GDP per capita. This could increase social tensions and widen protection gaps. For insurers, the high interest rates are beneficial.

The key takeaways:

- Today’s higher interest rates have transformed the operating environment for insurers, most notably for asset-intensive business, from low yields and lows returns to one of higher yields and higher returns.

- We estimate an aggregate 15% improvement in profitability for the life insurance sector across major and advanced markets, with an expected uptick in life savings products as a result of stronger investment returns.

- We also see stronger results in the non-life sector, with newly-underwritten business benefitting as the effects of high interest rates come through, and also due to improved investment returns.

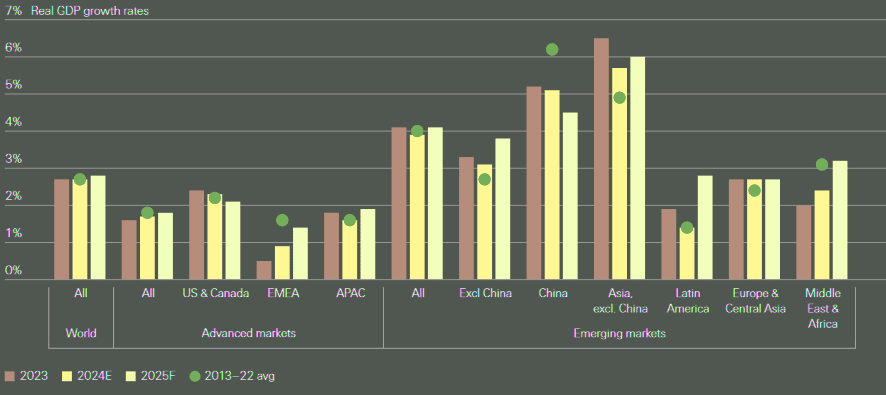

Global economic growth

Global economic growth has been strong over the past year, with high interest rates persisting due to ongoing inflation.

We project global GDP will grow by 2.7% in real terms in 2024. Regional differences exist, with the US growing above trend and the euro area below

Jérôme Haegeli – Swiss Re’s Group Chief Economist

This gap should narrow by 2025 as cyclical factors bring growth rates back to trend. Although the worst of the post-pandemic inflation crisis has passed, risks remain that could drive up insurance claims. Central banks will likely prioritize controlling inflation over growth.

Growth resilience

They boost demand for savings products, particularly in the life insurance sector.

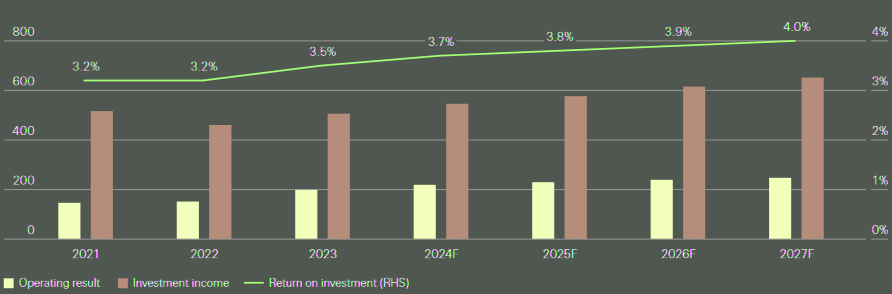

We forecast global life premiums to grow by 2.9% in real terms in 2024, up from 1.3% in 2023. Life sector profitability should see a strong 15% gain this year, driven by a 14% rise in investment income.

Higher interest rates will attract new capital investment, increasing the industry’s capacity for risk transfer solutions and enhancing societal resilience.

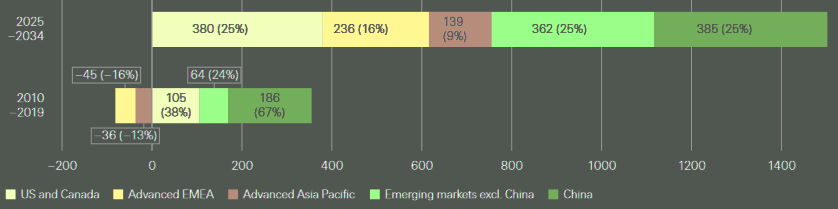

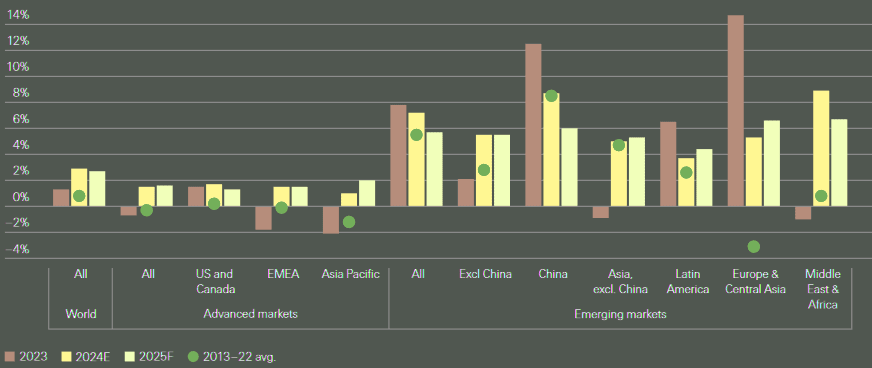

Advanced markets are expected to contribute significantly to life premium growth over the next decade, improving from the 9% contribution during the low-interest-rate era before the pandemic.

Recession fears have faded, and the pace of global growth is not far off the 2.8% average of the past two decades.

The last two years have proven more economically resilient than widely anticipated, providing a strong backdrop for continued growth in insurance premiums

Emerging Asia will lead world in growth for a third consecutive year. Emerging markets in Asia, including India and China, will also see substantial gains in insurance penetration.

Life insurance operating result and investment income and return on investment, G8 markets

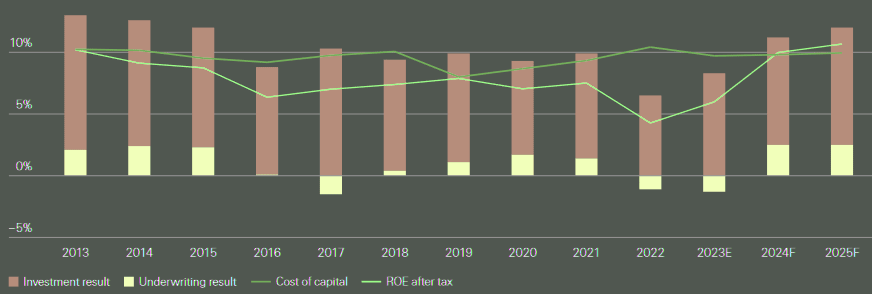

Non-life insurance sector profitability, G8 markets

In non-life insurance, global inflation has driven premium rates higher as insurers offset rising claims costs, especially in property and motor lines.

We expect the hard market conditions to persist this year but ease by 2025 as claims inflation softens.

Non-life premiums grew by 3.9% in real terms in 2023, up from 0.8% in 2022, mainly due to rate increases. Personal lines have seen higher rate increases compared to commercial lines, which are stabilizing after years of hard market conditions.

Social inflation pressures, particularly in the US, and persistent services inflation may continue to impact casualty lines like motor and general liability.

Advanced Markets Life Insurance

Life premium growth will likely see a significant rebound over the next decade. Strong demand for annuities will drive this increase.

Higher interest rates will make savings products more appealing. As a result, life insurers can offer better returns, attracting more interest in pension solutions.

This will help narrow retirement protection gaps. In emerging markets, life insurance will continue to grow as the middle class expands and incomes rise.

High wage and healthcare insurance costs in advanced economies contribute to ongoing claims inflation. In some markets, wage growth has not kept pace with premium rate increases, potentially affecting affordability, though insurance uptake rates remain stable.

Non-life sector profitability is on the rise. Return on equity rose to 6% in 2023, and we estimate it will improve to 10% in 2024 and 10.7% in 2025.

This improvement is driven by positive underwriting results and high investment returns due to higher interest rates. However, insurers should stay vigilant for potential new inflation shocks.

Geopolitical conflicts disrupting global supply chains could reignite claims inflation. Social inflation has been a concern for US liability insurers since 2015 and is now appearing in Australia as well.

Ranking of insurance markets by total premium

| Rank | Country | Total premium volume | Market Share | ||

| 2023 | 2024 | 2025f | 2023 | ||

| 1 | United States | 3,227 | 3,424 | 3,584 | 44.9% |

| 2 | China | 724 | 812 | 893 | 10.1% |

| 3 | United Kingdom | 375 | 401 | 420 | 5.2% |

| 4 | Japan | 363 | 370 | 382 | 5.0% |

| 5 | France | 283 | 292 | 303 | 3.9% |

| 6 | Germany | 245 | 255 | 264 | 3.4% |

| 7 | South Korea | 186 | 194 | 205 | 2.6% |

| 8 | Canada | 171 | 176 | 185 | 2.4% |

| 9 | Italy | 159 | 165 | 171 | 2.2% |

| 10 | India | 136 | 149 | 162 | 1.9% |

| 11 | Netherlands | 93 | 98 | 102 | 1.3% |

| 12 | Brazil | 84 | 92 | 98 | 1.2% |

| 13 | Spain | 83 | 88 | 92 | 1.2% |

| 14 | Taiwan | 78 | 80 | 84 | 1.1% |

| 15 | Australia | 74 | 76 | 79 | 1.0% |

| 16 | Hong Kong | 66 | 70 | 75 | 0.9% |

| 17 | Switzerland | 61 | 63 | 65 | 0.9% |

| 18 | Mexico | 45 | 50 | 54 | 0.6% |

| 19 | Denmark | 44 | 47 | 51 | 0.6% |

| 20 | Sweden | 44 | 45 | 48 | 0.6% |

*Data for 2023 is provisional for Canada, Switzerland, Hong Kong. Data for 2023 is estimated for US, UK, Japan, France, Germany, South Korea, Italy, India, Netherlands, Brazil, Spain, Australia, Denmark and Sweden.

Continuing global insurance growth for 2024 and 2025

Swiss Re Institute estimates that global gross domestic product (GDP) will grow by 2.7% in real terms in 2024, the same as 2023. This resilient growth is expected to continue into 2025 at 2.8% in real terms.

While the overall outlook is positive, regions are on different trajectories, with the US forecast to grow at 2.5% in 2024, while the euro area is expected to show below-trend growth of 0.7%.

The trend to global disinflation continues. However, returning to target inflation levels is unlikely to be a smooth journey.

Life premium growth, by region, in real terms

In the US, inflation is expected to return to target in 2025, due to higher-than-anticipated core services prices. Europe is already near its target inflation levels, driven by a fall in energy prices in 2023, softer core prices and an expected deceleration in wage growth.

Profitability for non-life insurance expected to improve

Due to inflation and the resulting rise in claims costs, non-life insurers have increased rates over recent years. Swiss Re Institute sees higher prices continuing for personal lines in 2024, moderating into 2025.

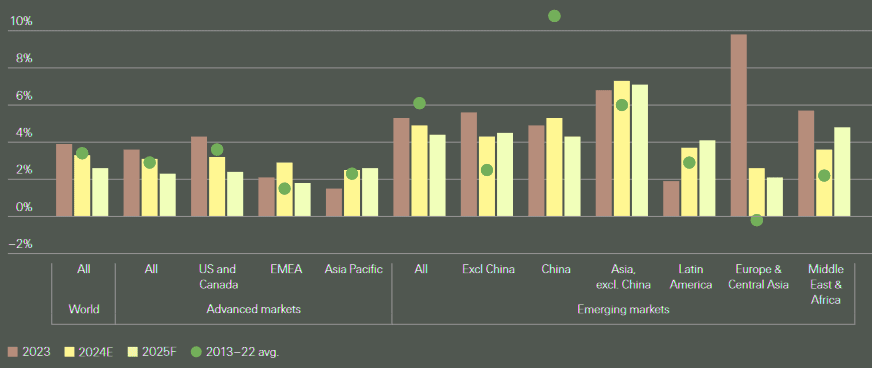

For commercial lines, though still positive, rate increases have decelerated with some markets starting to soften. Overall, non-life premium volume is forecast to build on the 3.9% growth achieved in 2023, reaching USD 4.6 trillion in 2024 and USD 4.8 trillion in 2025.

We estimate global non-life insurance premiums will grow by 3.3% in real terms this year, mainly due to sustained hard market conditions, particularly in personal lines.

Premiums grew by 3.9% in 2023, significantly improving from 0.8% growth in 2022 and exceeding the previous 10-year average of 3.4%.

The primary driver was rate hardening in advanced markets, with insurers raising prices to cover rising claims. As claims inflation eases, rates will likely moderate, and we forecast a slight slowdown in premium growth to 2.6% next year.

Non-life premium growth, by region, in real terms

Commercial insurance accounts for almost half of the total property and casualty market.

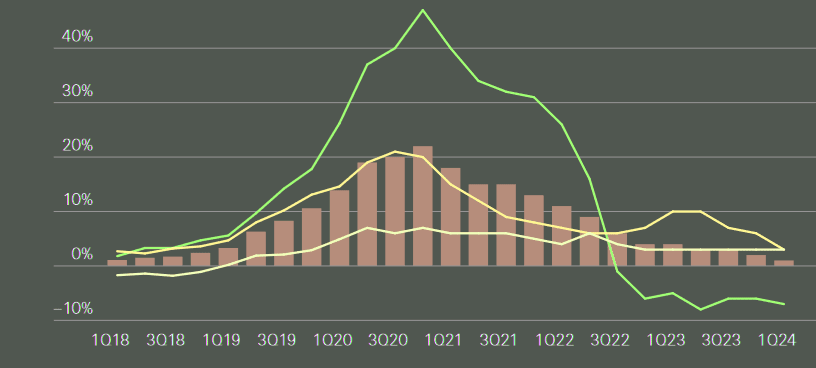

We expect commercial P&C carriers to maintain profitability in 2024, as rate trends have enabled lines like property to stay sustainably priced

Kera McDonald, Chief Underwriting Officer Swiss Re Corporate Solutions

The industry has seen single-digit rate increases for property business written this year. On the casualty side, we observe a trend of general market softening across most long tail lines.”

Property and casualty insurers are expected to improve profitability in 2024, with industry-wide return on equity (ROE) across eight major markets at 10% so far this year, up from 6% in 2023. ROE of above 10% is forecast into 2025.

Life insurance boom on the back of higher interest rates

The life insurance industry is facing a double benefit from the higher interest rate environment, with both top-line growth and improved profitability.

Swiss Re Institute forecasts 2.9% premium growth for the industry by the end of 2024, reaching a total premium pool of USD 3 trillion. Similar growth of 2.7% is expected in 2025.

Strong rebounds in growth should be visible in many key markets, with Western Europe and advanced APAC returning to premium growth.

Global commercial insurance rate development

A significant growth area for life insurance is the uptake of annuities to boost retirement savings. In the US, for example, sales of fixed-rate annuities jumped 63% in 2022 and 36% in 2023.

Longer term, advanced markets are expected to contribute half of all additional premiums over the next 10 years, driven by strong growth in annuities.

For 2024, Swiss Re Institute forecasts that the combination of increased premium and increased investment income will boost profitability in the life sector, with the operating results across eight top markets increasing 15% for the year.

………………..

AUTHOR: Jérôme Haegeli – Swiss Re’s Group Chief Economist, Mahesh Puttaiah – Head Insurance Market Analysis at Swiss Re Institute, Kera McDonald – Chief Underwriting Officer Swiss Re Corporate Solutions