US liability claims costs have risen by an annual average of 16% over the last five years, well above average rates of economic inflation at around 4%. The gap indicates that social inflation remains alive and kicking, according to Swiss Re Institute.

Over the last two years, surging economic inflation has grabbed the headlines, with personal line insurers in particular feeling the impact in terms of higher claims.

With the macroeconomic environment now turning to one of disinflation, the social inflation story is set to come to the fore again, with liability insurers most exposed.

Swiss Re Institute Index of macroeconomic resilience captures the extent to which an economy can withstand a shock such as a recession; Global Insurance resilience indices measure how insurance contributes to maintaining households’ and businesses’ financial stability by transferring or absorbing key risks to life, health and property.

- US liability claims costs rose 16% on average for the last five years, far exceeding economic claims drivers.

- The US is in the middle of a wave of social inflation, which is likely to continue unabated.

- Non-economic drivers of liability claims have been disrupted but not changed by COVID-19.

- Economic disinflation will not provide much relief for liability claims costs, and nor will stronger investment returns.

- The current rate of liability claims inflation is unsustainable. There’s no room for lapses in underwriting discipline.

According to Triple-I Research, for personal auto liability insurance, increasing inflation drove loss and DCC higher by $61 billion, or 6.5% of loss and DCC from 2013 to 2022. For the same period, increasing inflation drove commercial auto liability loss and DCC higher by $35 to $44 billion, or between 19% and 24% of loss and DCC.

Inflationary trends in auto liability insurance, personal and commercial combined, drove loss and defense containment costs (DCC) between $96 billion and $105 billion higher than they would have been for the period from 2013 to 2022.

US general liability insurance claims

Excluding reserves changes, US general liability claims were up 15%. This degree of claims severity, due mostly to social inflation factors, is unsustainable.

Higher investment returns due to higher interest rates will not be enough to cover the high claims, and liability insurers will need to retain focus on underwriting discipline.

Personal lines insurers have felt the impact of the economic inflation of the last two years most. US car insurance prices in the August CPI were up 19.1% from a year earlier, echoing prior surges in used car prices (peaked at 45% yoy in June 2021) and repairs (peaked at 23% yoy in January 2023), which had pushed up claims costs.

Meanwhile, construction costs in the Producer Price Index peaked at 23% in July 2022, driving up claims costs for a range of property lines.

Economic goods to services inflation

With disinflation for cars and construction materials progressing steadily, we see light at the end of the tunnel, although still-high wages for repairs and construction could continue to exert upward pressure on claims.

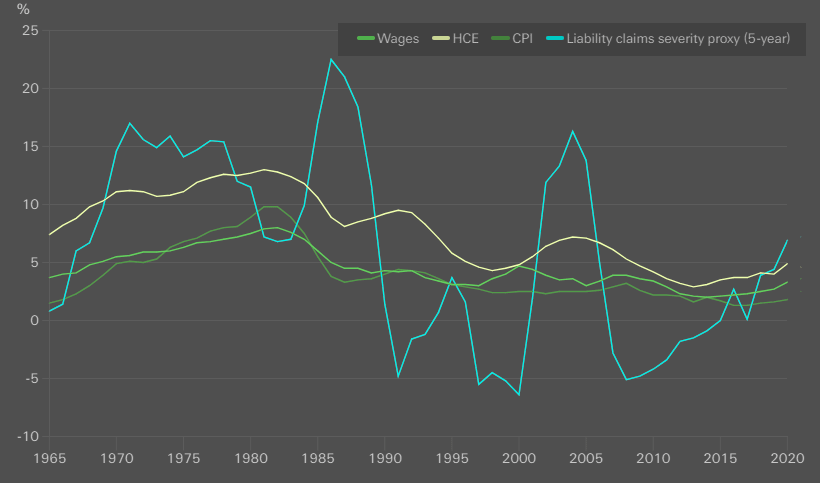

With the current rotation from economic goods to services inflation, attention is shifting back to liability lines, where wages and health care expenditures (HCE) are the key drivers for claims severity.

Figure illustrates long-term trends (5-year averages) between claims severity and HCE, wage and headline CPI inflation over the period 1960-2022. The correlation coefficient with claims severity was 0.61 for HCE and 0.53 for wage inflation.

The correlation between CPI inflation to claims severity was weaker (0.45). And this all in addition to the looming shadow that social inflation casts over the market, which we expect will continue unabated.

5-year averages of US CPI, healthcare and wage inflation

Social inflation has played a dominant role

Social inflation has played a dominant role in previous periods of rising claims severity. The US liability crisis of the mid 1980s was the first episode of runaway social inflation.

Corporates and their insurers were retroactively held liable for environmental damage and huge claims related to asbestos.

The second episode of social inflation in the early 2000s was driven by an expansion of mass tort. The current wave is characterized by a rising frequency of large single-claimant events, often based on ballooning non-economic damages.

At the same time, the number of claimants in multi-district litigation cases has risen to a historic high.

Outlook for social inflation

The current outlook for social inflation is based on several interconnected factors:

- Changing jury attitudes with larger sums awarded in tort cases, especially for non-economic damages. This trend has been driven by the belief that large corporations can afford substantial payouts and that the legal system should correct social injustices;

- The growing availability of third-party litigation funding allows plaintiffs to pursue better-funded cases for longer. According to Westfleet Advisors, the US litigation funding market grew by 44% between 2019 and 2022;

- Additional capital also leads to increases in legal advertising by plaintiff lawyers, further contributing to growth of mass torts;

- Social sentiment: trust in institutions has declined. There is a growing sentiment that corporations should be held accountable for a wide range of issues, from environmental damage to product defects;

- Expanding legal concepts: courts have expanded liability in certain areas, making it easier for plaintiffs to sue. Examples are public nuisance claims against manufacturers that have damaged public health.

Swiss Re see social inflation as particularly disruptive for liability insurance because it is difficult to measure and predict, and can disproportionally affect the longest-tail lines.

With long tail lines, any change in trends can have a leveraged impact, impacting both new business and prior-year loss reserves.

Based on current trends, the impact of social inflation outweighs the benefit of higher interest rates on long-tail lines’ investment income.

Current claims growth is unsustainable, and further pressure points are ahead, with emerging litigation risks originating from factors such as per- and polyfluoroalkyl (PFAS) chemicals, obesity, climate change, algorithmic liability, addictive software design, etc.

This could raise additional uncertainty for tort liability claims trends in the coming years.

…………………

AUTHORS: Dr Thomas Holzheu – Chief Economist Americas, Deputy Head of Group Economic Research and Strategy Swiss Re Institute, James Finucane – Senior Economist & Roman Lechner, P&C Economic Research Lead Swiss Re Institute