Overview

Insurers are confronting a new environment, in which disruption from the COVID-19 pandemic presents both short- and long-term challenges and opportunities.

The impact will be significant, although it’s impossible to say exactly how it will play out. Insurers are confronting a new environment, in which the COVID-19 pandemic creates short- and long-term disruption, while they focus on the critical questions right before them such as the safety of their people, solvency, operational effectiveness, regulatory changes, and general questions around what’s covered.

For an industry that was already undergoing significant change on multiple fronts (including a high degree of self-disruption), COVID-19 is likely to act as an accelerant to important trends.

In that sense, it’s bringing the future into much clearer focus. Insurers’ long-term plans suddenly have near-term urgency, as if the future arrived sooner than expected.

- The COVID-19 pandemic has disrupted economies and communities around the world.

- From basic social customs and working arrangements to the global movement of goods and capital, how we live and work is undergoing dramatic change.

- The insurance industry is no exception.

Our view is that insurers must not lose sight of longer-term imperatives – even as they focus on meeting immediate-term customer needs, maintaining solvency and ensuring operational resilience.

Insurers have made large-scale transformation investments – in redefining core value propositions, optimizing operations, updating technology, building a workforce of the future, and meeting new regulatory requirements.

COVID-19 only underscores the importance of these programs and will likely spark rapid need for many of them.

In this article, we look at different recovery scenarios and provide high-level recommendations on what insurers can do to stabilize and advance in four critical areas of the business.

The story so far

As COVID-19 has shut down commerce around the world, interest rates and share prices have fallen as investors weigh the impact of the crisis on both sides of the balance sheet. Some regulators, such as EIOPA, urged insurers and reinsurers to temporarily suspend all discretionary dividend distributions and share buy backs.

Many firms are following suit, while others are postponing annual meetings to reflect on the implications. Supervisors are requesting data more often and monitoring solvency closely. Ratings agencies are also re-evaluating business models.

On the upside, most insurers have implemented business continuity plans relatively smoothly, although some insurers have had issues. Challenges include the resilience of off-shore services and some third-party providers, as well as the ability to maintain a distribution cadence with customers who traditionally rely on face-to-face interaction.

Underwriting exposures have been mostly contained, with notable exceptions in travel, credit, event cancellation and health insurance.

So, what happens next?

Insurers will be looking for accurate and timely information as they evaluate their options in the face of broad uncertainty. There is a real risk that outdated or incorrect data could result in poor decision-making (as past paradigms for decision-making will not apply).

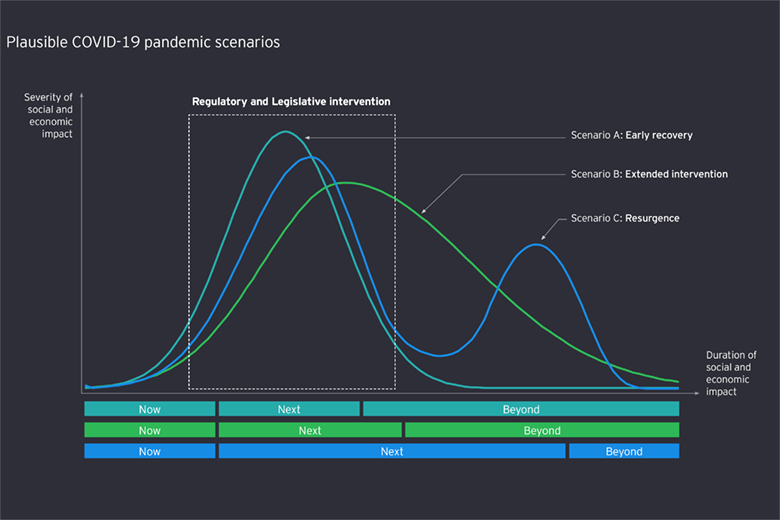

Based on the views of medical experts, economists, and industry analysts, we see three plausible pandemic scenarios. Again, the situation is fluid, but these views can help inform a dynamic planning process.

Scenario 1: Early recovery

In this scenario, strong public health response and the virus seasonality slow and contain the spread of COVID-19. Quarantines and travel restrictions drive sharp contraction in consumer spending, but the economy – supported by fiscal and monetary intervention – bounces back quickly.

Continuity planning and remote technologies alleviate workforce disruptions. This is the best-case, “sigh-of-relief” scenario nearly everyone was hoping for but seems now less and less probable.

Scenario 2: Extended intervention

Countries struggle to contain the virus due to its virulence, as well as disorganized responses and variable enforcement of containment strategies and tactics. A global recession caused by declining consumer spending and corporate investment continues even as infection rates decline seasonally.

As COVID-19 continues to spread globally, business supply chains are strained and the sustained contraction prompts layoffs and structural realignments.

Technology constraints on remote workers further depress productivity. The “new normal” proves very challenging and a profound shift for individuals, businesses and communities around the world.

Scenario 3: Resurgence

Public health and economic measures are lifted as the virus abates, but then the general public and policymakers get caught off-guard by a secondary and even tertiary wave of infections. Public fatigue dampens political appetite for further market intervention and industry “bailouts.”

Insurance operations struggle to keep up with customer activity and government action. Workforce attrition increases operational and cyber risks.

This scenario, in particular, underscores the need for insurance executives to conceive their response strategies along three-time horizons – now, next and beyond.

The framework for tracking impacts and actions

For insurers, managing the implications of COVID-19 across the business is critical to maintaining financial and operational resilience, as well as protecting brands and reputations. We see four core areas they should be focusing on:

We encourage preparers to address some key tasks in the near future to keep their projects on track, particularly given the potential COVID-19 impact.

1. Customers, products and distribution

Non-life and specialty insurers have several priorities related to customers, products and distribution. Customer and stakeholder needs must come first. That means clear and consistent communication around coverages, though future product needs and distribution preferences also merit consideration. The stakes are high: customers will remember for many years the decisions and actions insurers take now.

Life insurers must support in-force business while adapting rapidly to a redrawn landscape.

Specifically, that means managing risk within the investment book, while meeting obligations to policyholders in a fair manner. A good customer experience now will help mitigate reputational risks. Looking forward, new products will be necessary to drive revenue and maintain the industry’s relevance. The shift away from face-to-face distribution will gain momentum and self-service will increasingly dominate customer interactions. Here again, the pandemic is reinforcing the need for bold change.

2. People, operations and technology

Insurers face a number of practical threats and challenges as they respond to the pandemic. Some contact centers and service providers are struggling to operate remotely and to handle the high volume of inquiries.

To overcome challenges related to remote working, insurers are adopting tools to foster collaboration and keep their people engaged. Control and security frameworks are being hardened to deal with increased cyber threats.

On all these fronts, COVID-19 is accelerating the digitization of back-office processes (mirroring the automation of customer-facing processes). The pandemic is likely to power a permanent shift away from office-based teams, which will bring significant cultural impacts.

3. Capital, liquidity and investments

The financial impact of COVID-19 on the industry will be significant and won’t be fully known for years to come. Lower interest rates, wider spreads and lower equity values are significant threats to solvency.

Firms are taking steps to optimize hedging and protect capital. Proactively engaging regulators may help ease liquidity pressures as cash flows are squeezed by premium holidays and margin calls.

Earnings pressures are likely to rise due to shrinking revenue and increasing claims for some parts of the insurance industry. The intense financial pressures must be balanced with the need to serve customers and contribute to economic recovery.

4. Financial reporting and operations

Financial reporting and operations will feel the strain from COVID-19, too. Remote working could lead to longer close cycles, capacity issues, limited access to critical systems and delayed data from external partners. Time for management review may also be constrained.

Overall market volatility means a greater need for judgment from skilled finance and actuarial teams, as well as more complex off-cycle reporting to boards, regulators and investors.

COVID-19 won’t stop the need for IFRS 9 and 17 implementations; indeed, the pandemic will only increase the scrutiny of key metrics. There’s a lot for management to think about and they must do so across multiple time horizons.

The world has changed. Insurers must change, too

The current pandemic poses uniquely complex and unpredictable challenges. It is both an immediate threat and a long-term driver of disruption. In response, insurers need to use all the tools they have – and develop new ones.

Now more than ever, the insurance industry must find new ways to fulfill their critical purpose to provide protection.

EY expect leading insurers and reinsurers to expand not only specific coverage for pandemics but also loss prevention and risk consulting services that will allow them to significantly upgrade their core value proposition.

Above all, insurers must be ready to flex their plans as circumstances change. Despite economic uncertainty, firms must be prepared for each of the plausible recovery scenarios and understand the potential actions they can take to stay relevant, maintain client trust and position for long-term success.

………………………

AUTHORS: Isabelle Santenac – EY Global Insurance Leader, Peter Manchester – EY Global Insurance Consulting Leader and EY EMEIA Insurance Leader