Overview

- EV insurance is costlier – here’s what drives the difference

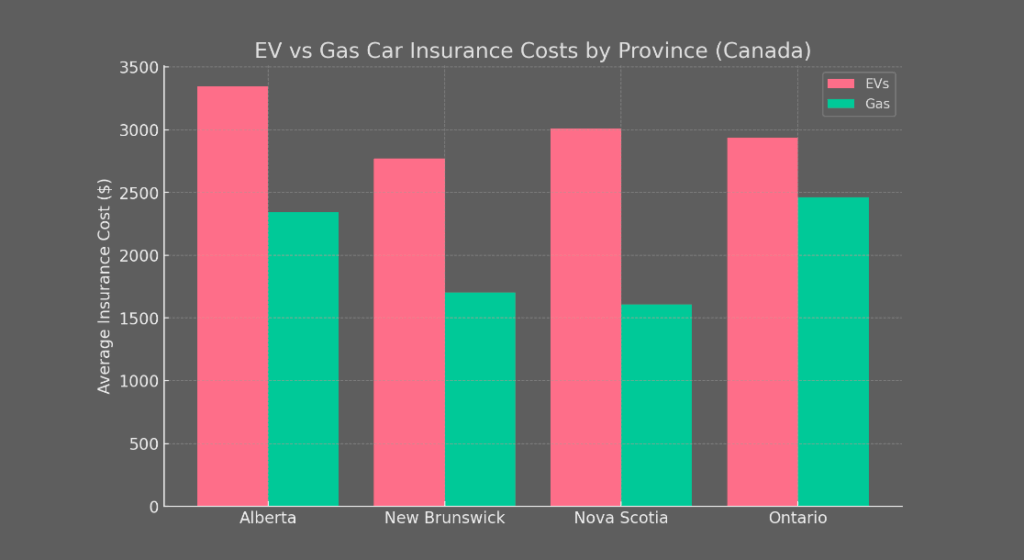

- Provincial averages – EV vs gas car insurance

- EV vs Gas Car Insurance Costs by Province (Canada)

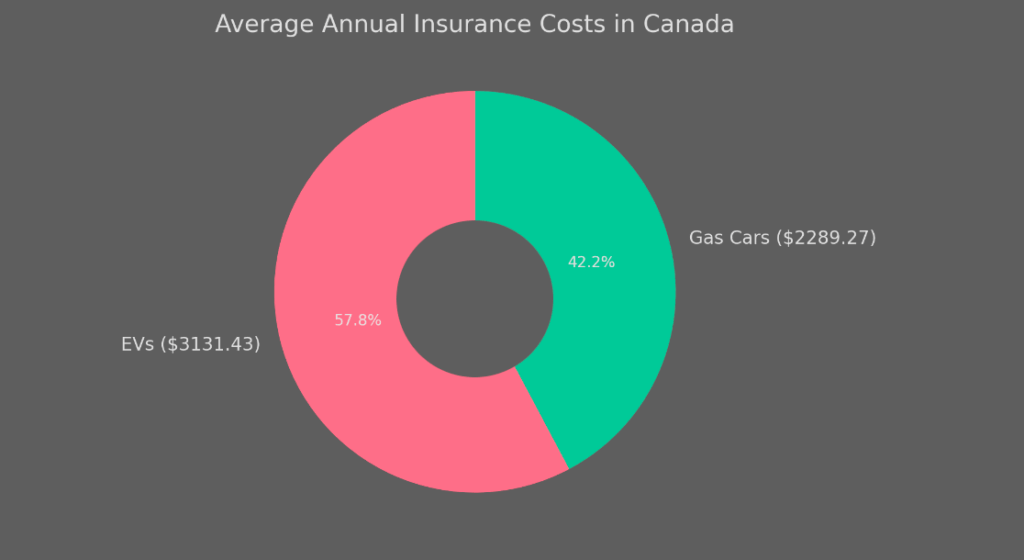

- Average Annual Insurance Costs in Canada

- EV vs Gas: Repairs and maintenance

- Factors influencing EV insurance costs

- EV vc Gas cars: Pros and cons snapshot

Insurance doesn’t always make the list when people compare EVs and gas cars, yet it should. According to Surex data from the past 12 months, insuring an electric vehicle in Canada runs higher than a gas-powered one.

Average gas car insurance premiums landed at $2,289.27 per year. EVs? $3,131.43. A 36.8% gap – not pocket change.

A study by Surex has found that the cost of insuring an electric vehicle in Canada is more than one-third (36.8%) higher than that of a traditional gas-powered automobile.

5 key highlights

- EVs in Canada cost 36.8% more to insure than gas cars – $3,131.43 vs $2,289.27 annually.

- Alberta has the highest EV insurance average at $3,342.93, while New Brunswick is lowest at $2,769.36.

- High repair costs, especially battery replacement, drive premiums upward, sometimes leading insurers to write off vehicles.

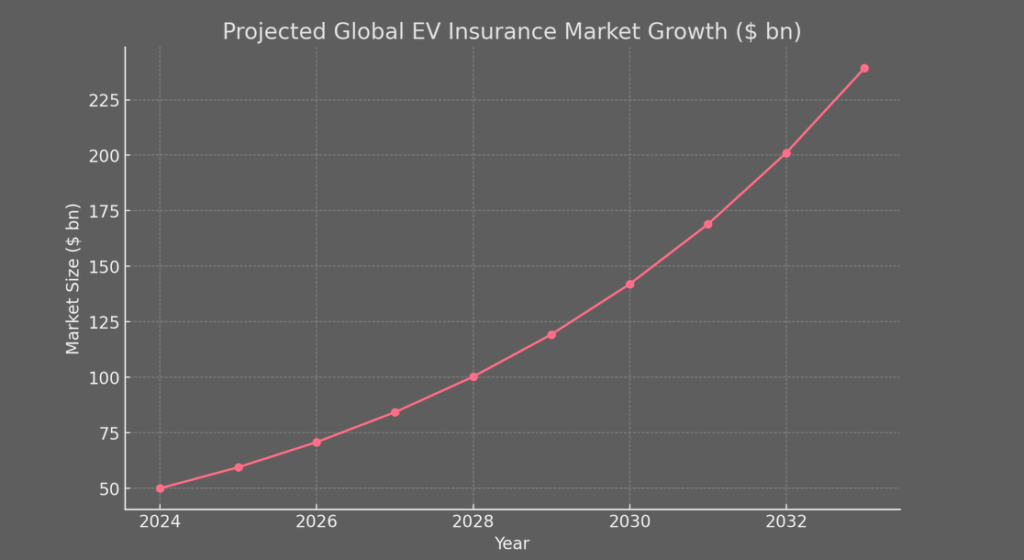

- EV insurance market projected to grow from $50 bn in 2024 to $507 bn by 2033, a CAGR of 19%.

- Telematics and usage-based insurance models are shaping EV coverage, rewarding safer driving and efficient charging habits.

Standard car insurance policies do not adequately address the unique risks and opportunities of EVs, from advanced battery systems to cutting-edge software.

Insurers are developing new types of insurance coverage for high-tech electric vehicles, with policies that also encourage environmentally conscious driving.

These changes aim to give drivers more control while helping advance sustainable transportation.

EV insurance is costlier – here’s what drives the difference

Break the numbers down by province and it gets even clearer. Alberta ranks most expensive for EV coverage at $3,342.93. New Brunswick comes in cheapest at $2,769.36. For gas cars, Ontario tops the chart at $2,464.18, while Nova Scotia drivers see the lowest average at $1,608.95.

According to Beinsure Data, considering the growing demand for EVs, all major insurance providers have already launched their EV-specific insurance products. As a result, the EV insurance market is expected to grow ten-fold from $50 bn in 2024 to $507 bn by 2033

The market is expected to grow at a CAGR of more than 19% during the forecast period. Falling EV prices, greater battery ranges, and sufficient charging infrastructure will contribute to the worldwide proliferation of EVs, growing the market for EV insurance in parallel.

Projected Global EV Insurance Market Growth ($ bn)

So what drives the difference?

EV repairs sit at the core. Battery replacement alone can cost as much as a car. In some claims, insurers simply write the vehicle off rather than pay for a new battery pack.

Add limited repair infrastructure – fewer certified mechanics, fewer independent shops – and labor costs climb. Parts aren’t cheap either. The math tilts premiums upward.

That said, EV owners still catch a few breaks. Green discounts exist, theft rates stay lower, and safety tech often trims risk.

But insurers continue to wrestle with thin historical data on EV claims. Gas cars have decades of loss patterns to lean on; EVs are still a moving target.

Provincial averages – EV vs gas car insurance

| Province | EVs | Gas |

|---|---|---|

| Alberta | $3,342.93 | $2,344.19 |

| New Brunswick | $2,769.36 | $1,704.76 |

| Nova Scotia | $3,009.30 | $1,608.95 |

| Ontario | $2,932.72 | $2,464.18 |

EVs generate vast amounts of data using onboard telematics, providing insurers with real-time visibility into driving behaviors, charging patterns, and vehicle health, Beinsure noted.

This data powers UBI or usage-based insurance models. It dynamically adjusts premiums based on a driver’s specific driving behavior rather than generic risk metrics.

Safe driving, avoiding hard acceleration, hard braking, and late-night charging (which stresses batteries) can earn drivers significant discounts.

EV vs Gas Car Insurance Costs by Province (Canada)

Average Annual Insurance Costs in Canada

Insurers are also applying this data to streamline claims. Telematics can automatically send provider notifications after a crash, accelerating assessments and payments.

EV vs Gas: Repairs and maintenance

Routine upkeep favors EVs. No oil changes, no spark plugs, no transmission rebuilds. But when things break, they break big, Beinsure noted.

Gas vehicles need more frequent servicing, yet the costs are predictable and widely available. EVs still lack technician availability.

Wait times, specialty labor, and proprietary parts inflate costs. Batteries remain the wildcard.

Other challenges that are impacting EV insurance premiums are charging infrastructure, immature supply chains, and global supply-side problems. These issues will subside over time, and the insurance premiums for EVs will resemble more closely to those of traditional ICE vehicles (see How to Reduce the Premium in Car Insurance).

On the other hand, government initiatives, legislation, greater battery ranges, falling EV prices, and increasing fuel prices are some of the opportunities that will lead to a rapid proliferation of EVs across the world.

Factors influencing EV insurance costs

Many factors are considered when determining your insurance rate. Because every driver’s situation is different, there’s no single coverage or price that works for everyone.

Policies are personalized to reflect your unique risk profile and needs.

What insurers look at

Premiums are never one-size-fits-all. They vary by make, model, provider, and driver. Still, five EV-specific factors show up consistently:

- Higher replacement costs than gas equivalents.

- Batteries priced so high they can push a total loss.

- Less claims data to set precise rates.

- Insurer-to-insurer pricing swings as competition shifts.

- Driver history, age, and address remain decisive.

Governments and insurers are also recognizing the economic and environmental benefits of EVs. In response, many regions are instituting incentives to reduce ownership costs. This, in turn, lowers the insurance premiums for electric car owners.

Discounts for green driving, reduced premiums for low-mileage driving, and partnerships with renewable energy programs are just a few examples.

While insurers do not generally offer direct rebates, some reward drivers who utilize renewable energy or adopt environmentally friendly practices with premium discounts. These incentives illustrate the growing movement toward sustainability in the insurance industry, Beinsure noted.

Detailed look at the factors that can impact the cost of EV car insurance

- Higher replacement cost – EVs are often more expensive to purchase than an equivalent gas car, making them more costly to replace after an accident.

- Battery replacement – The cost to replace an EV battery is a significant factor, as it can be very expensive and sometimes equivalent to the cost of buying a new car. In some cases, the price is so high that insurers may choose to write the vehicle off altogether.

- Vehicle make and model – The EV make and model, and how it stacks up against a comparable gas vehicle, plays a major role in insurance costs. Higher-value EVs (or those packed with advanced technology) often come with steeper premiums, much like luxury cars in the gas-powered market.

- Lack of claims data – Insurers have less historical claims data on EVs than on traditional gas cars, making it harder for them to accurately assess risk and set premiums.

- Insurance provider – Insurance prices can differ significantly from one company to another. As EVs become more common, some insurers are offering more competitive rates. That’s why it pays to shop around and compare quotes to find the best deal.

- Driving history – No matter the vehicle type, factors like your driving history, age, and where you live will still have a major impact on your insurance costs.

EV vc Gas cars: Pros and cons snapshot

EVs: cheaper long-term maintenance, cleaner footprint, smooth ride. Downsides – higher upfront price, limited range, slower charging.

Gas cars: longer range, faster refueling, cheaper entry price, broad infrastructure. Cons – higher fuel and service costs, more emissions, less efficient.

Choosing between EV and gas comes down to trade-offs. Some prioritize budget and convenience, others care about environment or long-term operating costs.

Insurance adds another layer. For now, EVs remain pricier to cover, though as adoption grows, that gap may close. Until then, it’s about personal math – what fits your lifestyle, your habits, your wallet.

FAQ

EVs come with high repair bills, mainly tied to batteries. A replacement can run so steep that insurers sometimes write the car off instead. Add pricier parts, limited repair networks, and specialized labor, and premiums climb

Surex data shows EVs cost 36.8% more to insure. Gas cars average $2,289.27 per year. EVs average $3,131.43.

Alberta tops the list for EVs at $3,342.93. New Brunswick is cheapest at $2,769.36. For gas vehicles, Ontario leads with $2,464.18, while Nova Scotia drivers average just $1,608.95.

Yes. Many insurers offer green driving discounts, reduced rates for low mileage, or perks tied to renewable energy use. Safety technology and lower theft rates can also bring premiums down.

EVs generate rich driving data. Insurers use it to power usage-based insurance (UBI), adjusting premiums based on braking, acceleration, charging habits, or mileage. Safer driving equals lower rates.

Major carriers already have EV-focused policies that cover advanced battery systems, charging infrastructure, and specialized risks. The EV insurance market is projected to surge from $50 bn in 2024 to $507 bn by 2033.

Gas cars are cheaper to insure today. EVs carry higher premiums but offset that with lower long-term maintenance, fuel savings, and environmental benefits. The choice depends on your budget, driving habits, and priorities.