Overview

The U.S. property and casualty insurance industry entered 2025 with a mixed underwriting outlook, according to the Insurance Economics and Underwriting Projections: A Forward View report from the Insurance Information Institute (Triple-I) and Milliman. Beinsure has analyzed market data and trends.

Personal auto insurance remains a strong performer, while general liability continues to face profitability challenges.

- Economics: P&C underlying economic growth ended 2024 slightly below U.S. GDP growth at 2.3% versus 2.5% year-over-year (YOY). However, in 2025 and 2026, P/C underlying growth is expected to be above overall GDP growth, an improvement in year-end expectations. A further economic milestone occurred in 2024 with the number of people employed in the U.S. insurance industry surpassing three million.

- Underwriting: P&C net combined ratio (NCR) estimate of 99.5 is a YOY improvement of 2.2 points, while net written premium (NWP) is estimated to increase 9.5% YOY. Personal lines NCR estimate improved by nearly 1 point relative to our prior estimates, primarily due to better-than-expected Q3 performance in personal auto. Commercial lines NCR estimate increased by 1.2 points due to commercial property and general liability. NWP growth rate for personal lines is expected to continue to surpass commercial lines by 9 points in 2024.

Insurance Segment Highlights

P&C underlying economic growth is expected to remain above overall GDP growth in 2025 (2.3% versus 2.1%) and 2026 (2.6% versus 2%) as lower interest rates continue to revive real estate and contribute to higher volume for homeowners’ insurance and commercial property, Beinsure noted.

This is an improvement on our 2025 P&C underlying growth expectations from second half of 2024. The pace of increase in P&C replacement costs is expected to overtake overall inflation in 2025 (3.3% versus 2.5%).

This aligns with our earlier expectations from the second half of last year.

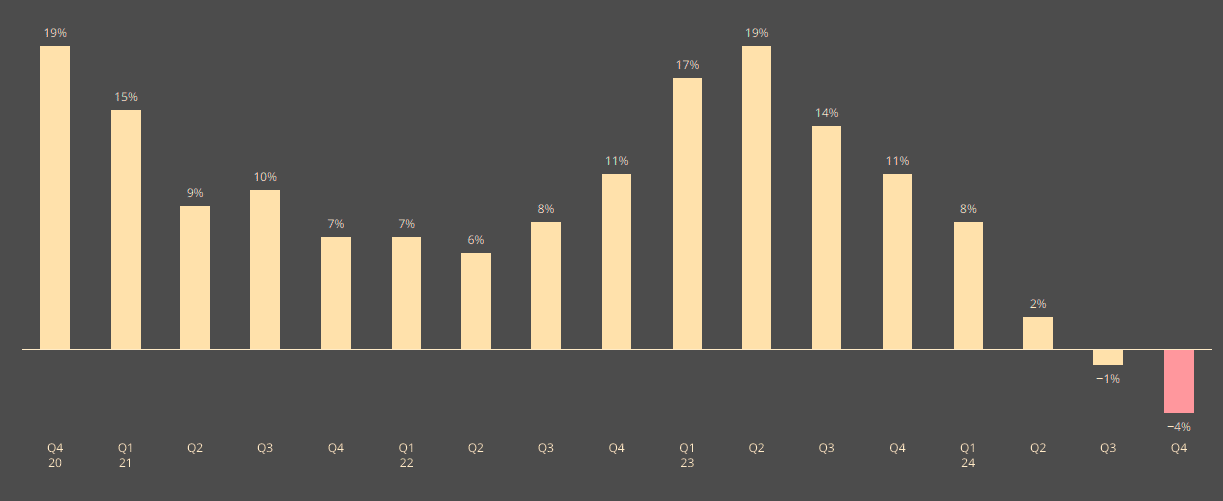

According to Global Insurance Market Index, commercial insurance rates declined by 3% in Q1 2025, the third consecutive decrease in the composite rate following seven years of increases. A continuing increase in insurer competition was the main catalyst behind rate trends, which declined globally in every region and across all major product lines other than casualty.

Marsh’s analysis shows global property insurance rates fell 3% in Q4, with the Pacific region experiencing the sharpest decline at 8%.

The U.S. and UK saw 4% reductions, while Canada, Latin America, the Caribbean, and Asia reported slight decreases.

Financial and professional lines rates fell 6% globally, with declines in every region. Cyber insurance also dropped 7%.

Personal Auto Insurance

The net combined ratio (NCR) for personal auto in 2025 is projected at 96.0, about 1 point higher than in 2024, yet still reflecting ongoing profitability.

Homeowners Insurance

Wildfires in Los Angeles in January 2025 drove significant losses, resulting in the worst first-quarter loss ratio for homeowners in over 15 years and the worst quarterly result since Q2 2011.

General Liability Insurance

The Q1 2025 general liability loss ratio was the second-worst first quarter in more than 15 years, improving by less than 1 point compared to Q1 2024 and signaling continued profitability concerns.

Insurance Industry Trends and Economic Factors

Insurance Premium Growth

Net written premium growth for 2025 is forecast at 6.8%, down 2.0 points from 2024 and the lowest since 2020. Personal lines are expected to outpace commercial lines by 1.5 points in 2025, though the gap is projected to narrow by 2027.

Further premium growth and improved underwriting performance should continue in 2025 and 2026, provided geopolitical and economic conditions remain relatively stable, Beinsure noted.

Profitability

The industry-wide NCR is projected at 99.3 for 2025, 2.7 points higher than 2024. Broader profitability is anticipated to return in 2026 despite current challenges in specific lines.

Michel Léonard, Ph.D., CBE, chief economist and data scientist at Triple-I, remarked that the U.S. economy and P/C industry have shown resilience despite tariffs and trade uncertainty, with industry growth outperforming U.S. GDP.

However, he warned that revised economic data later this year may indicate a weaker economy and raise concerns about contraction or recession heading into fall.

With inventories running low, their depletion will now accelerate inflation and slow growth for the rest of the year.

Michel Léonard, Ph.D., CBE, chief economist and data scientist at Triple-I

He noted that rising prices, especially for personal auto, are significant, with used car and truck prices up 7.7% in the first half of 2025.

The P&C industry typically lags the economy by one to two quarters, suggesting potential industry impacts from broader economic contraction beginning in Q1 or Q2 of 2026.

US Insurance Market Rates

Below are insights into the US insurance market rates. U.S. property insurance rates dropped 4%, a sharper decline than the 1% recorded in the previous quarter.

Increased insurer capacity, driven by strong financial results over the past three years, contributed to the trend. Casualty insurance rates rose 7%, with an 11% increase when excluding workers’ compensation.

US property insurance rate change

Property insurance rates declined 4%, compared to a decline of 1% in the prior quarter. Casualty insurance rates increased 7%; excluding workers’ compensation, the increase was 11%, Beinsure noted.

- The property market remains sensitive to loss events, particularly the ongoing Los Angeles wildfires, which will impact aggregate catastrophe losses in 2025.

- Workers’ compensation continued to be the primary casualty line of interest for most insurers; however, concerns continued regarding increasing reserves and rising medical costs.

- Auto liability continued to pose profitability challenges for insurers due to larger jury verdicts nationwide and rising auto physical damage costs. General liability rates remained relatively stable, with average increases of approximately 3%.

In the umbrella and excess liability market, risk-adjusted rates increased 15% compared to 21% in the prior quarter.

Outlook by Insurance Line

Personal Auto Insurance

Personal auto projected NCR of 98.8 is 6.1 points better than 2023, with 2024 NWP growth rate of 14% the second highest in over 15 years. Homeowners projected 2024 NCR of 104.8 is a 6.1-point improvement over 2023 despite an above-normal hurricane season.

Commercial Auto Insurance

Jason B. Kurtz, FCAS, MAAA, principal and consulting actuary at Milliman, noted that commercial auto is expected to remain unprofitable through 2027 despite double-digit premium growth estimated in 2025.

Commercial lines continue to have better underwriting results than personal lines, but the gap is closing

Dale Porfilio, FCAS, MAAA, Triple-I’s chief insurance officer

“The impact from natural catastrophes such as Hurricane Helene in Q3 2024 and Hurricane Milton in Q4 2024 significantly impacted commercial property. The substantial rate increases necessary to offset inflationary pressures on losses have driven the improved results in personal auto and homeowners,” Dale Porfilio added.

Commercial auto continues to remain unprofitable. The 2024 direct incurred loss ratio through Q3 is only marginally improved relative to 2023 and is the second highest in over 15 years.

Regarding general liability, the line has seen significant worsening, with each quarterly loss ratio in 2024 worse than 2023 on a YOY basis.

“The 2024 direct incurred loss ratio through Q3 is the highest in over 15 years. As a result, we have increased our expectations for 2025 and 2026 net written premium growth, as the industry responds to the worsening 2024 performance,” Dale Porfilio said.

Commercial Property Insurance

Commercial property insurance projected NCR of 91.2 is 3.3 points worse than 2023, with Hurricane Milton projected to be the worst catastrophe for commercial property insurance since Hurricane Ian in 2022 Q3. General liability projected 2024 NCR of 103.7 is 3.6 points worse than actual 2023 experience.

Fitch Ratings projects that the property and casualty (P&C) insurance sector will continue to face difficulties in 2025 due to volatile natural catastrophe risks.

However, the firm believes strong capital reserves, prudent risk management, and effective reinsurance strategies will help insurers absorb potential losses.

Property catastrophe rates remain high due to the growing frequency and severity of storms. Larger insurers can better manage these risks through diversified portfolios and strong reinsurance protections.

However, in states like Florida, smaller specialty insurers depend heavily on reinsurance and state-backed programs such as the Florida Hurricane Catastrophe Fund and Citizens Insurance. If losses exceed reinsurance coverage, many of these firms could face financial distress.

Hurricane intensity is becoming more unpredictable due to rising sea surface temperatures. Recent storms, including Helene and Debbie, have impacted areas previously considered lower-risk.

General Liability Insurance

Kurtz expects the general liability NCR to improve in 2026–2027 but remain unprofitable. He called attention to the high first-quarter 2025 direct incurred loss ratio which only slightly improved compared to 2024, Beinsure noted. On the positive side, premium growth appears to be strengthening.

Workers’ Compensation Insurance

Workers’ compensation shows a more positive trend, with a forecasted 2025 NCR of 90.6, an improvement of 1 point over prior estimates. The Q1 2025 loss ratio was the lowest in over 15 years.

Stephen Cooper, executive director and senior economist at the National Council on Compensation Insurance (NCCI), highlighted the labor market’s role in supporting workers’ compensation.

With economic uncertainty elevated and recession concerns resurfacing, consumer behavior will be important to watch.

“While employment has been concentrated in fewer industries, the labor market has remained resilient with continued strong payroll growth,” he said.

Turning to workers’ compensation, Donna Glenn, FCAS, MAAA, chief actuary at the National Council on Compensation Insurance (NCCI), provided a preview of this year’s average lost cost level changes and discussed the long-term financial health of the workers compensation system.

The 2025 average loss cost decrease of 6% is moderate, which will inevitably have implications on the overall net written premium change.

Donna Glenn, FCAS, MAAA, chief actuary at the National Council on Compensation Insurance

She added that the –6% average loss cost level change in 2025 is notably different than was seen in 2024: an average decrease of more than 9%, representing the largest average decrease since before the pandemic.

“Payroll for 2025 will develop throughout the year resulting from both wage and employment levels. Therefore, overall premium will become clearer as the year progresses,” Glenn said.

FAQ

The outlook remains mixed because personal auto continues to perform well with a projected NCR of 96.0, signaling profitability, while general liability and commercial auto face ongoing challenges. General liability posted its second-worst Q1 loss ratio in over 15 years, and commercial auto is expected to stay unprofitable through 2027.

P&C underlying economic growth ended 2024 slightly below U.S. GDP at 2.3% versus 2.5% year-over-year. However, in 2025 and 2026, P/C growth is expected to outpace GDP, driven by lower interest rates, stronger real estate activity, and higher volume in homeowners’ and commercial property insurance.

Net written premium growth for 2025 is forecast at 6.8%, down from 2024 but still positive. The industry-wide NCR is projected at 99.3, up 2.7 points from 2024, though profitability is expected to recover in 2026. Personal lines are forecast to grow faster than commercial lines by 1.5 points in 2025, with the gap narrowing by 2027.

U.S. property insurance rates fell 4% in early 2025, while casualty rates rose 7% (11% excluding workers’ compensation). Commercial insurance rates globally declined 3% in Q1, marking a third consecutive drop after years of increases, mainly due to higher competition. Cyber insurance and financial/professional lines saw notable rate reductions as well.

Commercial property faces higher catastrophe risks and volatile losses, with projected NCR of 91.2 in 2024 — worse than 2023 — influenced by hurricanes Helene and Milton. General liability remains unprofitable with quarterly loss ratios at multi-year highs, although some improvement is anticipated in 2026–2027.

Workers’ compensation continues to show strength. The forecasted 2025 NCR is 90.6, better than prior estimates, and the Q1 2025 loss ratio was the lowest in more than 15 years. A moderate 6% average loss cost decrease is expected in 2025, following a larger 9% decrease in 2024, with strong payroll growth supporting premiums.

Rising prices, especially in personal auto (with used car and truck prices up 7.7% in H1 2025), low inventories, and potential recessionary signals pose risks. The P&C industry usually lags the economy by 1–2 quarters, suggesting that any broader economic contraction could impact results starting in early 2026. Geopolitical stability and natural catastrophe trends will also remain critical influences.

……………………

AUTHOR: Michel Léonard, Ph.D., CBE, chief economist and data scientist at Triple-I, Stephen Cooper, executive director and senior economist at the National Council on Compensation Insurance, Dale Porfilio, FCAS, MAAA, Triple-I’s chief insurance officer, Donna Glenn, FCAS, MAAA, chief actuary at the National Council on Compensation Insurance