Overview

Economic slowdown will drag on global insurance market growth in 2023 and 2024, with total premiums (non-life and life) forecast to grow at a below-trend 1.2% annual average in real terms.

Swiss Re Institute expect total premiums volumes will rise above USD 7 trillion for the first time ever by the end of 2023. Rate hardening in commercial lines will continue to support nominal premium growth in non-life, but this will in part be offset by higher claims. Life insurance should benefit from higher risk awareness and digital interaction. As a silver lining, over time rising interest rates will support industry profitability by yielding higher investment returns.

Economic dynamics to weigh on overall market growth

Reflecting current economic conditions, we expect insurance markets to tread water this year. At the aggregate level, we see essentially flat growth in total global premiums in 2022 in real inflation-adjusted terms (nominal +6.1%, this based on employment growth, high risk perception and rate hardening).

Nevertheless, in nominal we expect total premiums volumes will exceed the USD 7 trillion mark for the first time ever by the end of this year.

Swiss Re base our estimation of a rise in total Global insurance premiums to USD 7.3 trillion from USD 6.9 trillion at the end of 2021 on strong market recovery from pandemic-induced lows, continued rate hardening in non-life, and stronger premium growth in emerging markets in particular.

At this level, global premium volumes will be 17% higher than at end-2019 before the onset of the COVID-19 crisis. The increase over that three-year time span reflects the overall resilience of insurance markets over the course of the pandemic, and also last year’s strong recovery.

The decline in global premiums resulting from the COVID-19 shock was less severe than the fall seen during the global financial crisis (GFC) of 2008–09. And, with above-trend growth of 3.4% in real terms 2021, the recovery was also stronger than one year after the GFC.

Mid-term Insurance outlook remains challenging

All told, the mid-term outlook remains challenging. At the aggregate level, we expect the stalling of global premium growth this year will be followed by stronger but still slightly below-trend growth in 2024 (2011–2020 CAGR: 2.4%).

We expect that claims inflation will offset rate hardening in non-life insurance, and also a reduction in demand for life savings on account of reduced disposable incomes given high levels of inflation.

Pricing in the commercial property and liability insurance markets will likely continue to harden, especially in advanced markets, with improvement in most lines of business as insurers seek to offset the impact of high inflation. In life insurance, we expect high inflation will erode nominal premium growth. At the same time, however, we expect demand for protection-type products to remain robust.

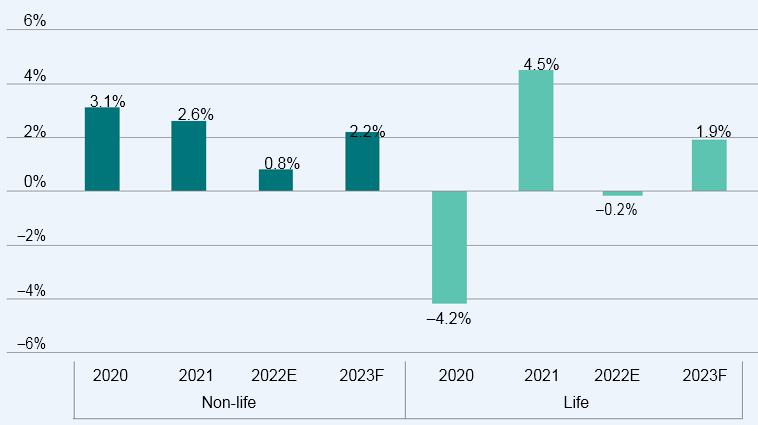

Real premium growth, non-life and life

Outlook for the insurance industry

We expect 2025 will be transition years for the insurance industry as it navigates the economic realities of high inflation and low growth. This and other factors make for a mix of longer-term tailwinds and shorter-term headwinds for sector growth, investment performance and insurers’ balance sheets:

Headwinds in the short- and medium terms

- Impact of the war in Ukraine. The Russian and Ukrainian markets will see considerable loss of premium income due to the conflict and international sanctions. The conflict will also impact consumer sentiment and curb demand for insurance.

- Continued claims inflation. The impact of the conflict will be felt primarily through additional price pressures that increase the level of claims. Property, casualty and health insurers are most exposed.

- Balance sheet. Weaker equity markets this year and widening credit spreads will likely lead to mark-to-market valuation losses on assets and capital.

Tailwinds in the medium- and long terms

- Rising interest rates. These will boost insurers’ investment returns.

- Heightened risk awareness post pandemic. There is higher demand for life insurance products (mortality protection, health) as consumers’ risk awareness has increased during the pandemic.

- Rate hardening. We expect claims inflation to feed through into rate hardening in non-life commercial and personal lines this year and next.

Non-life insurance

The war in Ukraine is weighing on global non-life insurance sector growth (see Ukraine conflict: impact on non-life business). Impacts are already showing through in the formof claims inflation. Associated economic slowdown will also have negative implications, the extent of which will depend on the duration of the conflict.

We expect inflation of exposure values and rate hardening to drive nominal premium growth of 7.1% in 2023 in spite of slowdown, with volumes rising to USD 4.1 trillion. However, in real terms, we forecast that global non-life premium growth will slow to 0.8% this year from 2.6% in 2021.

We expect notable slowdown in personal lines growth. Motor in particular will likely see sub-par premium growth, and also sub-par underwriting results due to increased competition across this segment. For 2024, we forecast a return but still slightly below-trend real growth of 2.2% in global non-life sector premiums.

Non-life real premium growth, by region

Ukraine conflict: indirect impacts to outweigh the direct

Slowing premium growth as the global economy heads into downturn and higher claims costs on account of inflation pressures, are the main indirect impacts that the war in Ukraine will have on insurance markets. Food inflation and geopolitical uncertainties will also weigh.

The longerterm ramifications of the indirect will outweigh direct impacts, including the insured losses that the conflict will trigger (see How to Russia’s War in Ukraine is Changing the World and Insurance?).

Capacity wise, the global non-life insurance sector should be able to absorb the direct insured losses triggered by the war. Based on a recent external estimate, potential losses range from USD 13 billion to USD 23 billion.

There could be claims in niche segments such as aviation war, trade credit, political risk or marine war, depending on the covers provided and policy wordings. In relation to the conflict in Ukraine, some 500 aircraft currently in Russia are leased from international firms. The outcome of the evolving situation is uncertain.

Another line of business directly exposed is cyber. Here demand and premium growth will likely accelerate the longer the war goes on, given the heightened perception of the risks that could further emanate. For this reason, we also expect to see rate hardening in cyber, and likewise in other specialty lines with elevated claims exposures.

Russia and Ukraine themselves will see considerable loss of premium income in the non-life sector due to the conflict. We expect direct non-life premium volumes in Russia to contract significantly this year given economic sanctions and the withdrawal of foreign companies from the market.

Wider negative premium impacts may be felt in specialty insurance given lower demand as a result of disruption to in economic activity. In aviation and marine, sanctions mean international traffic to/from Russia is now very limited.

Future foreign investments in Russian assets and infrastructure are unlikely in the near- to medium term, for instance with the UK and EU also prohibiting re/insurance in Russia for strategic sectors like aerospace.

Premium income increased to USD 3 863 bn, up 8.3% in nominal USD terms.

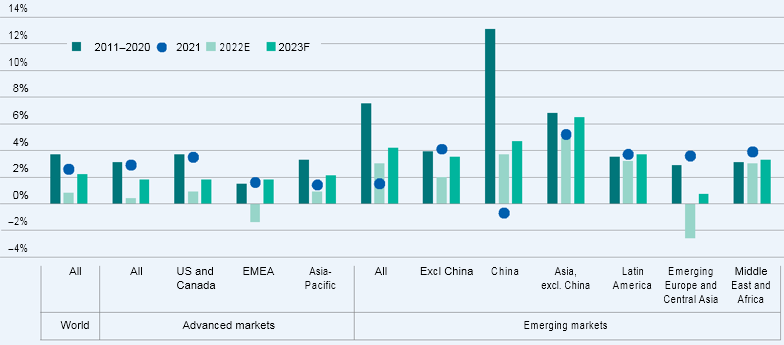

Advanced market premiums were up 2.9% in real terms, mostly on the back of rate hardening in commercial lines. In the US and Canada, premiums grew by 3.5%, followed by advanced EMEA with a 1.6% gain and advanced Asia Pacific with 1.4%.

Emerging market premiums were up 1.5% in real terms. The slower aggregate growth rate relative to advanced markets was mostly due to a 0.7% decline in premiums in China, where motor premiums contracted by 6.6% due to de-tariffication. This was partly offset by a 10.6% in medical insurance premiums in China.

The aggregate for emerging markets excluding China was stronger, with premiums up 4.1%. Premium growth in Latin America improved to 3.7%, emerging Europe and central Asia to 3.6% (2020: –0.2%), but emerging Asia down to 0.4%.

By business, global commercial insurance premiums grew by 4.4% in real terms last year, after a 2.6% gain. This was on the back of rate hardening across all major lines of business except commercial motor.

Premiums in personal lines were up 0.7% with weakness in motor, which accounts for 60% of global personal lines business. The weakness resulted from heightened competition after the windfall profits due to low claims, with lockdowns across markets having taken many drivers off the road.

The slump in China on account of the de-tariffication also dragged. Health/medical expense (medex) insurance premiums were up 3.7%. US medex premiums, which account for more than 80% of the global total, were up 3.1%.

In emerging Asia, medex premiums grew by 13.8% last year, due to rising awareness of health protection in the wake of the COVID-19. Growth was strong in India (22.4%) and China (10.6%).

Outlook non-life industry

We estimate 0.8% growth in global non-life premiums. The US primary health insurance market, which accounts for one-third of global non-life premiums, remains a primary contributor to growth. Rising prices and utilisation across the US health care system are driving premium increases.

Further, the expected continuation of the public health emergency declaration beyond July 15 indicates that the 18.7 million additional people who have Medicaid coverage due to pandemic relief legislation, will likely continue to be covered until at least 2024.

We forecast that global medex premiums will grow by below-trend 1.7% in 2023 and 1.5% in 2024, with strong demand in emerging markets due to increased awareness of health security continuing to support.

Commercial lines (including workers compensation) will continue to expand more than personal lines (including health). We estimate a 1.1% increase in commercial premiums, and a 3.1% gain in 2023, supported by rate hardening.

Personal lines insurance premiums will expand by an estimated 0.5%, mainly on account of stagnation in advanced markets. A main reason for this a still competitive environment in motor, with new car sales 12% below pre-pandemic levels.

In China on the other hand, growth in motor should normalise after the de-tariffication effect although there too, new car sales are still weak. For 2024, we forecast that global premiums in personal lines business will grow by 2.7%.

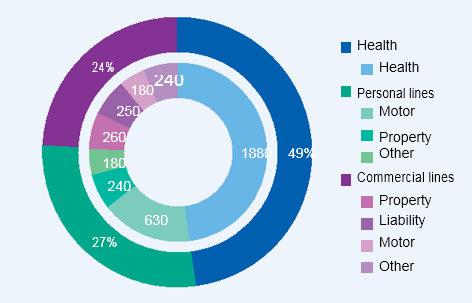

Global non-life premiums, by line of business, USD bn

The impact of high inflation on claims costs

In non-life insurance, inflation means higher claims costs (ie, claims inflation), and these erode profitability. By line of business, motor and property insurance will bear the brunt of the immediate claims cost impact of the current high-inflation environment.

We expect the war in Ukraine and continuing lockdowns in China to prolong disruptions in the auto industry’s supply chains for spare parts and new cars. In the construction sector, supply disruptions related to raw materials and labour shortages are putting near-term upward pressure on property claims.

Accident, motor liability and general liability business will also be impacted by high inflation, showing through in elevated claims for bodily injury. The longer the inflation surge lasts, and the more it broadens out to wages and higher healthcare costs, the more it will drive bodily injury claims higher. This will not only negatively impact current claims but also claims reserves of unsettled claims from prior years.

Property, specialty and professional liability are more exposed to CPI inflation and/or social cost escalation.

In non-life business, the degree of potential exposure is driven by:

- the duration (years of claims) of loss reserves exposed to the spike in inflation;

- the reserve leverage, meaning the level of affected reserves as a % of premiums.

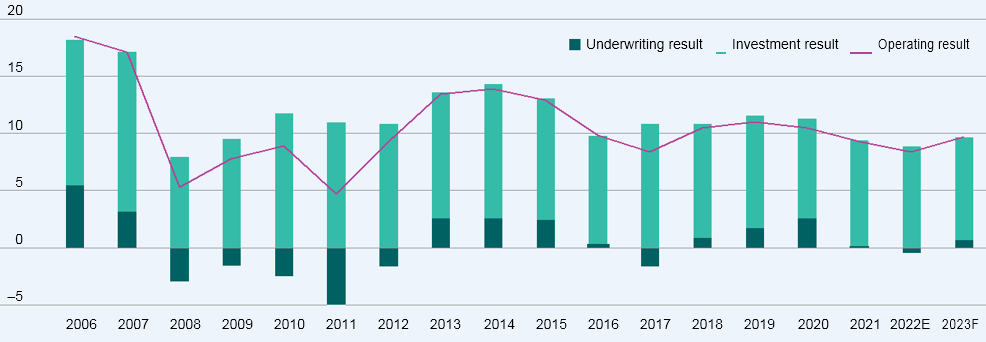

With respect to underwriting results, we expect that higher interest rates will have more immediate positive impact by easing pressure on the underwriting gap.

In the last decade of low interest rates, we estimated that in a sample of G7 markets, non-life insurers had to improve underwriting margins in a range of 6-9 ppt depending on market if they were to meet their long-run ROE targets.

We estimate that in a still-challenging environment of high inflation and low growth, higher interest rates will mean that underwriting margins will need to rise by a lesser 4 ppt in order to meet ROE expectations.

Meanwhile, lower equity markets, rising interest rates and widening credit spreads have led to mark-to-market valuation losses. With re/insurers typically holding fixed income investments to maturity, most of these near-term book value losses do not flow through ROE earnings but do reduce capital in GAAP accounting.

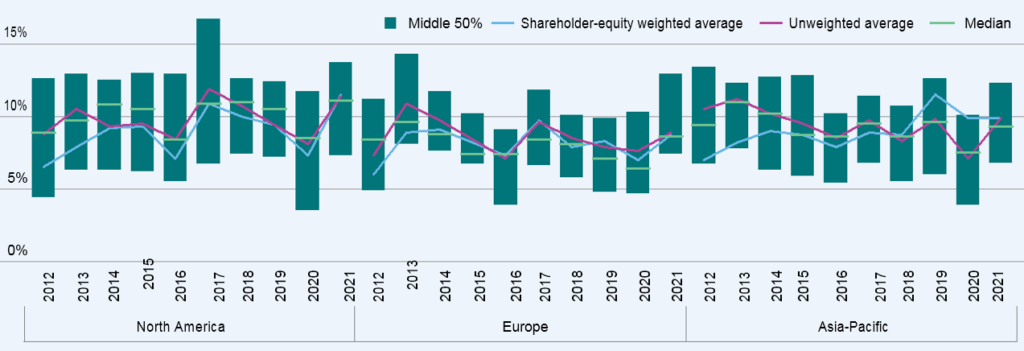

Profitability of the eight major non-life markets, % of net premiums earned

Insurer investment yields to react slowly to interest rate lift-off

Monetary policy tightening will further lift the short end of the US yield curve, which has been moving higher since 2021. This will increase future non-life industry profits through higher returns on the investment portfolio. However, even if policy rates rise as we expect, the near-term impact on the total industry results will likely be small.

We see a flattening of the yield curve with long-term yields moving sideways as bond markets anticipate slower growth for the next few years.

The gradual turnover of the longer-dated bond portfolio will delay any effect of rising rates on average portfolio yield. In addition, an existing portfolio yield that includes securities purchased in higher interest rate periods will do likewise.

In addition, companies’ reinvestment yields on long-dated securities are generally within 1 ppt of the effective portfolio yield, despite the recent uptick in interest rates.

For example, assuming the 10-year US Treasury yield is close to 3%, that compares with a 2% average over the preceding decade.

Barring significant additional yield increases, we expect the reported industry investment result to improve but remain broadly in line with recent experience. One positive is that the expected profitability of new business has improved immediately from the higher yield curve compared to the low-yield environment of last year.

Cash equivalents and short-term investments benefit immediately from higher policy rates but in the US, for instance, these comprise just 7% of the non-life sector investment portfolio.

The more significant impact will accrue as higher rates are earned in bond portfolios, which account for more than half of invested the sector’s assets, as well as in other long-term investments. However, only one-tenth of bonds with an initial duration of more than 1 year mature within any given year. As market yields increase (or decrease), effective portfolio yields will follow with a considerable lag due to the large legacy portfolio.

Life insurance

We estimate that global life premiums will contract slightly (–0.2%) in real terms in 2022 after last year’s robust recovery from pandemic-induced lows. In nominal terms, we estimate 4.8% growth to USD 3.1 trillion in 2022.

Inflationary pressures, economic uncertainty and financial markets condition are the primary drivers of subdued premium growth.

Saving premiums, which represent more than three-fourths of the total life premiums, will likely suffer due to volatility in the financial markets and as disposable incomes fall. Heightened risk awareness due to COVID-19 continues to support demand for life protection (and health) insurance products, while rising interest rates will supportprofitability of savings-linked business.

We forecast that global life premium growth will recover to 1.9% in real terms as inflation pressures ease and economic conditions improve.

Life premiums in advanced markets grew above trend at 5.4% in 2024 after shrinking by 5.8% in 2020. Strong premium growth was supported by a surge in asset values and labour market recovery that lifted demand for saving-linked business.

Regulatory developments and a tax law change boosted the sale of annuity products in the US, resulting in real premium growth of 2.7%.

In western Europe, insurers’ continuous business and a low base effect. In advanced Asia-Pacific, market shifts towards protection products under regulatory encouragement supported market growth.

The main reason was subdued income growth in China, which undermined consumers’ confidence in their financial position and thus demand for saving policies. Regulatory headwinds and a declining insurance agent workforce further weighed, leading to a 2.6% contraction in life premiums. Sector performance in other emerging markets was stronger.

Improved economic conditions after the pandemic-induced slump, increased risk awareness due to COVID-19, and a low level of insurance penetration boosted demand for life insurance.

In emerging Asia, life premiums in India, Malaysia, and Vietnam grew by 8.5%, 5.3% and 18.6%, respectively. On aggregate, premiums in the Emerging Europe and Central Asia region grew by 7%, and in Latin America by 3.8%, driven by Brazil and Mexico (premiums up 2.8% and 5.2%, respectively).

Outlook non-life industry

The life sector faces near-term headwinds from this year’s high-inflation environment, and we estimate that global premiums will contract by 0.2% in real terms. However, medium-term tailwinds remain well anchored and will continue to support industry growth over the longer term. Heightened risk awareness post-pandemic is driving demand for protection-type products, and insurers are changing their business models to be digital-age ready.

The high-inflation environment will have much lesser impact in terms of feeding through into claims inflation than in the non-life insurance sector. This is because policy benefits are defined at inception, and inflation itself does lead to a rise in mortality.

We forecast that global life premiums will grow by 1.9% in 2024, stronger than the previous 10-year annual average (2011–2020) of 0.9%. Next year’s improvement will reflect recovery in both advanced and emerging markets.

In terms of sector profitability, higher interest rates will boost investment returns in the longer term. And, while COVID-19 related claims are likely to linger through 2022, they should gradually decrease thereafter.

We estimate that life premiums in advanced markets will decline by 0.6%, after growing by 5.4% in 2021, and to recover to 1.2% in 2023. Inflationary pressure will reduce real premium growth in 2022.

Return on equity (%) of a sample of life insurers, by region

In nominal terms, we estimate that life premiums will increase by 4.8% in advanced markets this year. Labour market normalisation and increased risk awareness will continue to underpin protection business in 2022 and 2024.

The conflict in Ukraine, higher inflation and adverse financial markets developments has weakened the near-term outlook in advanced Europe, and there we estimate that life premiums will contract by 1.1%.

In North America, we see a 0.4% decline in premiums in real terms this year, mainly due to high inflation expectations. In nominal terms, we expect life premiums in the region to grow by 6.7% as ongoing regulatory developments and higher interest rates support annuity business growth.

Advanced Asia-Pacific is likely to see a flat premium growth in real terms (+2.5% in nominal terms) due to market shifts towards protection products under regulatory push and increased risk awareness post pandemic.

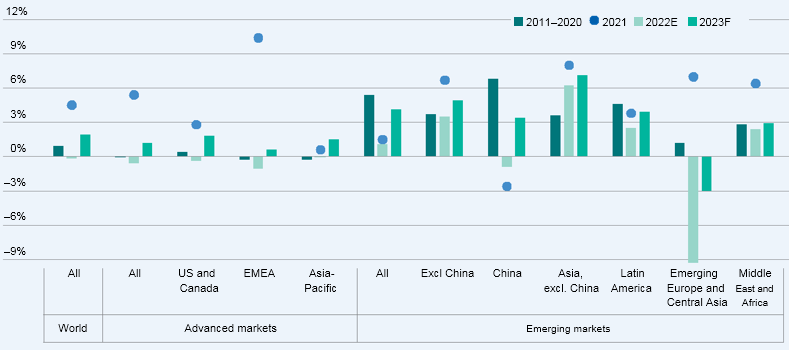

Life real premium growth, by region

In the other emerging markets together (excluding China), we estimate that life premiums will grow by 3.5% in real terms this year, below 3.9% growth between 2011 and 2020. The outlook for emerging Europe and central Asia is negative.

Given its proximity, this region is the most exposed to the economic turbulence caused by the conflict in Ukraine, and we estimate an 9.3% contraction in real life premiums.

Global Insurance Market forecast

We forecast growth of 6.6% in India in real terms, the second largest life insurance market in emerging world, as group business continues to perform well. Term products have also performed well, post-COVID-19. For Latin America, we see life premiums up 2.5% this year, with real growth eroded by high inflation.

We also estimate 2.4% real premium growth in the Middle East and Africa this year. As an underlying reality, we expect low insurance penetration rates to continue to support growth in emerging markets over the medium-term.

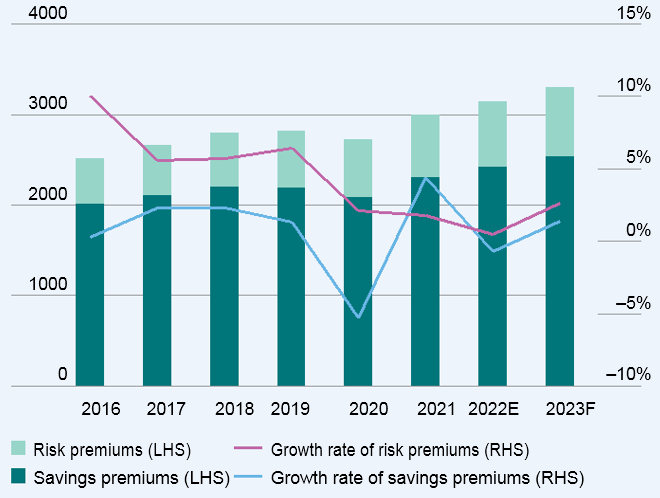

By line of business, we expect savings premiums to soften this year under challenging financial market conditions and in high-inflation economies.

At the global level, we forecast a 0.7% contraction in premiums. This follows an exceptionally strong 2023 driven by favourable macro-financial conditions.

We see savings premiums growth recovering slightly to 1.4% in 2023. Most advanced markets will likely see a decline in saving premiums, as inflation pressures dampen disposable incomes and propensity to save. In parallel, interest rate hikes increase the attractiveness of saving-linked products.

We estimate global life premiums from protection business (ie, “risk premiums”) will grow only slightly by 0.5% mainly due to a contraction in North America where inflation will erode nominal growth.

Global L&H premiums by risk and savings in USD billion

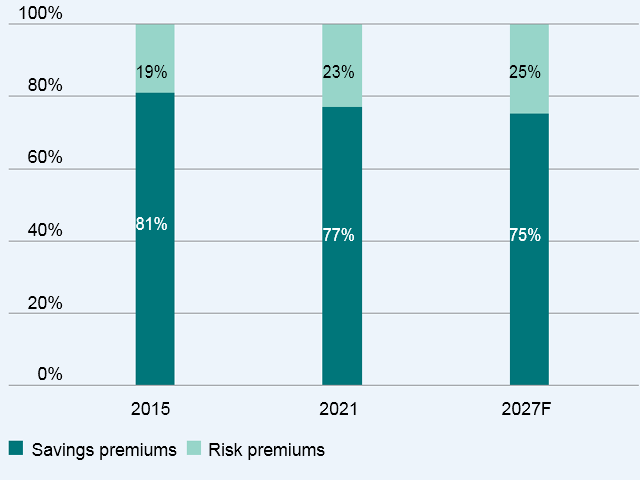

Global L&H premiums share of total

We estimate that life insurance profitability in 2022 and 2023 will continue last year’s trend of moderate improvement, based mainly on rising interest rates. We also expect that the severity of pandemic-related claims will likely subside and normalise.32 Life insurance sector stock price indices, a forward-looking indicator of expected performance, reflect our outlook.

Life insurance indices for all regions trended upwards through 2021 in the aftermath of the COVID-19 delta wave at the start of the year. Indices in all regions saw sharp declines in February this year due to heightened economic and geopolitical uncertainty caused by Russia’s invasion of Ukraine.

However, there was a partial recovery soon after, driven by interest rate hikes and the expectation that overall, the conflict will have little impact on life insurance business. The impact will mostly be felt through higher inflation, which in any case should be offset by monetary policy tightening.

Downside risks to the profitability outlook mainly emanate from high inflation and what are still low interest rates and potential fallout of the Russia-Ukraine conflict. Life insurers in western European markets are more vulnerable to potential fallout from the Russia-Ukraine conflict given geographical proximity and region’s dependence on gas from Russia, which could accentuate the economic slowdown in the region.

High inflation poses downside risk to profitability through potentially lower demand for insurance and, to a lesser extent, through a higher expense ratio.

Also, though rising, interest rates in all major markets are still below the pre-pandemic levels.

The associated boost to investment returns from higher interest rates takes time to show through on the balance sheets of insurers as life insurer’s portfolio comprises long-term fixed-income assets and turns over slowly.