Overview

Gallagher Re’s latest Asia Pacific Market Watch Report paints a detailed picture of Japan’s non-life insurance market – a global top-10 player and one of the largest in the region – as it continues to evolve through disciplined underwriting, structural reform, and shifting reinsurance dynamics. Beinsure analyzed the key trends.

The report highlights trends, challenges, and opportunities shaping the industry across the 14 markets we track in the Asia-Pacific region.

Premium growth has slowed due to competition and other challenges, making business quality a key differentiator for resilience. However, there are opportunities for growth, and the reinsurance market continues to be supportive as we head into the 2026 renewal.

While growth in non-life premiums continues, it has moderated in many places, with infrastructure spending and digitalization driving gains in some areas.

Key Highlights

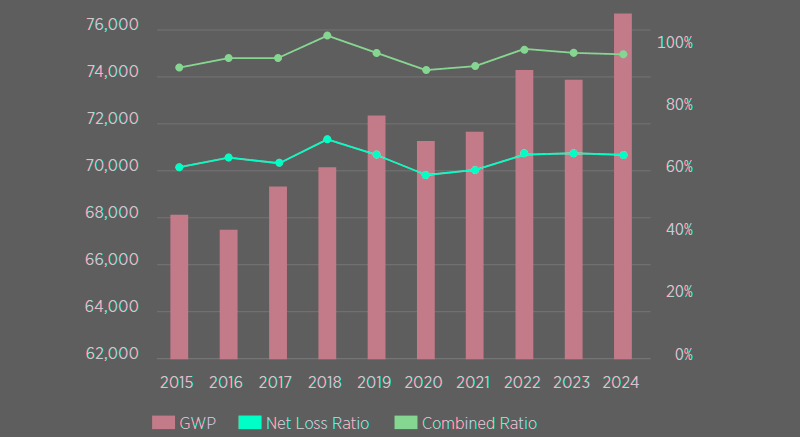

- Japan’s non-life market regained momentum in 2024 with gross premiums up 3.9% to $76.6 bn. Growth has slowed compared with previous years due to competition and cautious underwriting, but profitability and capital strength remain solid across major lines.

- After years of hardening, property catastrophe reinsurance rates eased 10-15% at April 2025 renewals. Insurers maintained strong underwriting discipline, especially in commercial fire, with rate hikes of 10%-30% on loss-affected accounts.

- Japan’s risk environment remains complex, with major 2024 losses from the Noto Peninsula earthquake ($2 bn) and Hyogo hailstorm ($935 mn). Climate-driven physical risks are intensifying, prompting tighter exposure management and new regulatory stress tests led by the Financial Services Agency.

The report identifies five key themes shaping the near-term trajectory of APAC’s non-life insurance industry. We set out how insurers are rising to meet these challenges, and how Gallagher Re can support.

Japan’s Economic Landscape

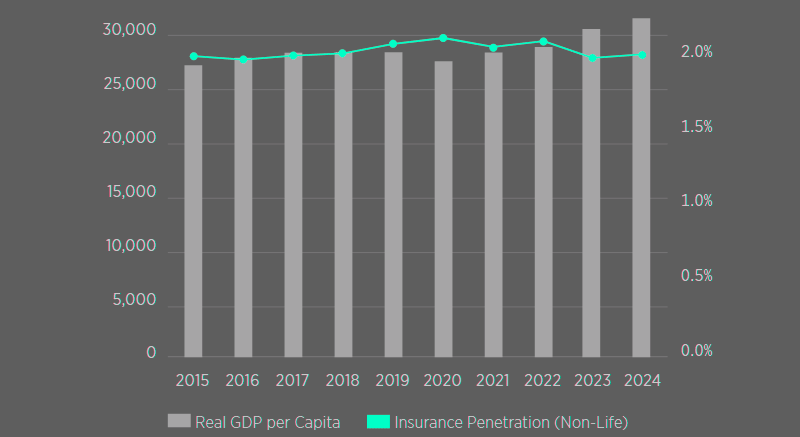

The Bank of Japan (BOJ) revised its forecast for Japan’s real GDP growth in FY2025 to 0.5% at its outlook statement in May, down from the 1.1% projected in January. This adjustment reflected both slower-than-expected private consumption, and global trade uncertainties.

Nevertheless, Japanese corporate profits have remained stable, and unemployment figures remained low at 2.5% as of April 2025.

The BOJ has maintained a cautious approach to monetary policy, keeping its policy rate at 0.50% as of its meeting in June 2025. The central bank has emphasized gradual adjustments to its monetary stance, focusing on inflation stability and wage growth.

In 2025, Japan’s government bond yields have increased significantly, particularly for long-term bonds such as the 20-year and 30-year securities, Beinsure noted.

As of August 31, the yield on 30-year government bonds had risen by almost 100 basis points since the start of the year, reaching 3.2%, while the 20-year bond yields had climbed over 70 basis points.

Many major Japanese insurance companies may be negatively affected if the yen gets stronger, because they have significant overseas operations. The value of earnings from these foreign subsidiaries may be decreased when converted back into yen, potentially reducing overall profits.

Japan’s Insurance Market Landscap

Japan is one of the world’s top 10 markets by non-life insurance premiums, and one of the largest in the APAC region. The market is conventionally split into three segments. There are 35 domestic non-life insurers, and 22 foreign branches conducting non-life business (including a Lloyd’s operation).

Within the above, there are nine companies operating a reinsurance business only. MS&AD announced in March 2025 that it aims to merge MSI and ADI in April 2027, Beinsure noted.

Consolidation remains active: MS&AD announced in March 2025 that it will merge MSI and ADI by April 2027.

Japan also has a system of “kyosai”, or co-operative insurers or mutuals, which play a key role in providing mutual aid and insurance services.

For the purposes of this report, kyosai are excluded from the analysis, as they operate under distinct legal and regulatory frameworks separate from those governing commercial non-life insurers.

GDP per Capita vs Non-Life Insurance Penetration ($)

Non-Life Premium and Claims ($ mn)

Domestic and foreign insurance players

According to the report, smaller domestic and foreign insurance players are finding new opportunities as major insurers tighten underwriting.

Larger carriers have been cutting exposure in commercial fire and U.S. casualty lines, improving portfolio quality but leaving room for niche specialists to grow.

After a minor setback in 2023, Beinsure noted, Japan’s non-life market regained traction in 2024. Gross premiums climbed 3.9% to ¥12 tn ($76.6 bn), while net premiums increased 4.9% to ¥9.6 tn ($60.9 bn).

Members of the General Insurance Association of Japan reported a collective net loss ratio of 64.1%, a notable improvement.

Japan’s Non-Life Insurance Market Structure

Premiums rose strongly in 2024, mainly driven by fire and motor lines, which saw revisions of products and increases in rates. Fire insurance saw rate hikes for profitability.

Motor insurance loss ratios worsened, prompting planned 2025 increases. Structural reforms support stronger underwriting and exposure.

Property insurance

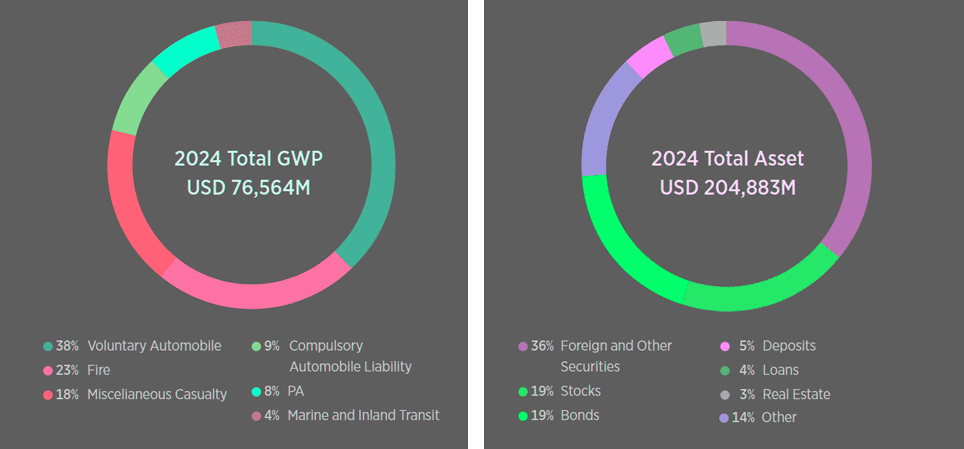

Property insurance, which makes up about 23% of total premiums, benefited from rate hikes, product redesigns, and stronger profitability targets.

Insurers are tightening exposure controls and expanding internationally, while Japan’s broader corporate reforms are promoting a more independent, underwriting-driven culture.

Motor insurance

Motor insurance remains dominant, accounting for roughly 47% of total premiums. Voluntary motor loss ratios worsened to 60% in 2024, reflecting rising repair costs and natural catastrophe losses. Significant rate increases are planned for 2025 to counter that trend.

Casualty and financial lines

Casualty and financial lines, together representing around 26% of premiums, held steady. Domestic liability rates stayed firm, while pricing for accounts with U.S. exposure continued to be refined.

Directors’ and officers’ and errors and omissions coverages also remained stable in Japan, though modest softening appeared in overseas placements.

Gallagher Re highlighted that the country’s top insurers maintained strict pricing discipline, particularly in commercial fire.

Three major players implemented around 10% rate hikes in late 2024, with some loss-heavy accounts seeing increases above 30% and reduced capacity.

Reinsurance Trends in Japan

Reinsurance trends in Japan showed similar discipline. The property catastrophe segment, which hardened after repeated typhoon events since 2018, reached near-record pricing levels. Improved profitability in 2024 led to risk-adjusted rate cuts of 10%–15% at April 2025 renewals.

Property risk portfolios saw reductions between 2.5% and 7.5% for loss-free programs, while proportional treaties earned modest commission increases of up to 2.5% – the first in years.

Third-party liability reinsurance renewals proved complex but generally successful as insurers trimmed U.S. exposure and reinsurers allocated capacity carefully. Loss-free accounts saw flat to 5% rate increases.

Cyber reinsurance remains a bright spot, buoyed by low loss ratios and controlled limits, while personal accident coverage has softened as capacity flowed back post-pandemic.

Japan’s Insurers Face Shifting Risks

Japan’s insurance market remains exposed to multiple natural and systemic risks, with 2024 highlighting just how complex that landscape has become.

Gallagher Re’s analysis points to steady improvements in underwriting discipline even as insurers adapt to tightening regulation and evolving climate pressures.

The year began with the Noto Peninsula earthquake, which caused about $2 bn in insured losses, followed by April’s Hyogo hailstorm that generated $935 mn in claims.

While typhoon-related losses have been relatively contained in recent seasons, Japanese property insurers have managed to improve results by curbing catastrophe exposure and lowering policy limits.

- Casualty insurers continue to wrestle with their U.S. exposure — a long-standing concern. Many have reduced their participation in general liability accounts tied to American risks, prioritizing capital efficiency and volatility control.

- In cyber, a surge in ransomware attacks has pushed up the frequency of large claims. Growth has slowed to roughly 5–10% per year, but rates remain stable, and margins are still solid. The segment continues to stand out as one of Japan’s most profitable non-life lines.

- Marine insurers, meanwhile, face a tougher outlook. Global cargo premiums are expected to contract amid weaker trade volumes linked to U.S. tariff policies. At home, inflationary claims are eroding profitability, with frequent small losses and rising repair costs. Hull insurance profitability also remains difficult.

Another evolving front is energy. Japan’s drive toward carbon neutrality by 2030 is spurring major investment in renewables, including offshore wind. The government aims for 10 GW of capacity by 2030 and 30–45 GW by 2040, with large-scale offshore projects expected to reach full operation starting in 2026.

New Insurance Rregulation and Climate Focus

Regulatory reform is moving in parallel. The revised Insurance Business Act, passed in May 2025, will require insurers and agents to build stronger compliance systems. Enforcement is due by May 2026, following updates to related regulations and industry guidance.

The law may reshape relationships between insurers, agencies, and customers while boosting the profile of independent brokers — who currently write less than 1% of Japan’s direct non-life premiums.

Cross-shareholdings, long a structural feature of Japan’s corporate world, are being dismantled. Tokio Marine, MS&AD, and Sompo plan to sell all $60 bn worth of cross-holdings by March 2031, freeing capital for acquisitions and reducing balance-sheet risk.

On the accounting side, IFRS reporting has become optional for consolidated accounts since fiscal 2023, while J-GAAP remains mandatory for non-consolidated filings. Sompo has already adopted IFRS, and TMHD along with MS&AD will follow from FY2025.

A new solvency regime based on economic value, announced in July 2025, will take effect by March 2026.

Gallagher Re said the transition should be smooth for larger insurers already managing risk on similar frameworks.

Climate risk management also remains a regulatory priority. In 2024, Japan’s Financial Services Agency worked with 19 non-life insurers and the General Insurance Rating Organization of Japan to conduct its second climate risk scenario test.

The study found that acute physical risks will intensify as global temperatures rise — a warning that Japan’s risk models will likely face new stress in the coming decade.

We think this mix of market recalibration, climate exposure, and sweeping policy reform underscores how Japan’s insurance industry is preparing for its next phase — one built less on protection from volatility and more on managing through it.

Insurance and Reinsurance Pricing Environment

Japanese cedants have put tremendous efforts into improving profitability, especially for commercial fire (property) business.

They have made great efforts to achieve greater underwriting discipline, through measures such as improving the terms and conditions for unprofitable business, and managing their line-size for high-hazard business.

For commercial fire business, the major three insurance companies have increased rates by around 10% since October 2024.

In some cases, insurers increased rates by more than 30% on loss-affected and loss-making accounts with reduced line-size. For casualty business, rates are stable except for businesses with US exposures.

In the reinsurance market, compounded hardening since the major typhoon activity of 2018 has led to near-historic pricing levels in property catastrophe business.

But the majority of programs have been profitable since 2024, whilst there has been an overall reduction in cat XL limit. As a result, at the most recent renewal in April 2025, we saw risk-adjusted rate reductions of between -10% and -15%.

In property risk business, there has been extensive remediation following poor results. Capacity deployed by both new and existing markets has been more moderate, compared to cat business.

Loss-free portfolios saw risk-adjusted rate reductions of between -2.5% and -7.5% at the April renewal. There was a flat-to-2.5% increase in commissions for pro rata business; the first increase for many years.

In general third-party liability business, the renewal was more challenging. Nevertheless, insurers have made significant efforts to reduce US exposures, and reinsurers were willing to deploy strategic capacity placements. As a result, most programs were comfortably placed, albeit with loss-free portfolios experiencing rate rises between 0% and 5%.

Cyber business was attractive to reinsurers, with low loss ratios and small limits, and in personal accident lines, there was considerable softening as capacity returned, post COVID.

Gallagher Re’s analysis captures a clear shift: Japan’s insurers are trading short-term volume for long-term sustainability.

In an environment defined by measured growth and tightening discipline, that’s a story of quiet strength — and resilience built, not bought.

FAQ

Japan’s non-life market continues to expand, driven by disciplined underwriting, structural reforms, and strong reinsurance support. Growth is moderate compared to past years, with property and motor lines leading premium increases. Corporate governance reforms and capital discipline are also improving profitability.

The Bank of Japan cut its FY2025 GDP growth forecast to 0.5% from 1.1%, citing weaker consumption and trade uncertainty. Despite this, corporate profits and employment remain steady. Rising bond yields and yen fluctuations are affecting insurers’ investment returns, especially for companies with large overseas portfolios.

Japan ranks among the world’s top ten non-life markets, with 35 domestic and 22 foreign insurers. Consolidation is ongoing, with MS&AD planning to merge MSI and ADI by 2027. The market also includes cooperative kyosai insurers, though they operate under separate legal frameworks and are excluded from commercial analysis.

Natural catastrophes remain a constant risk, highlighted by the Noto earthquake ($2 bn loss) and Hyogo hailstorm ($935 mn). Other challenges include managing U.S. casualty exposure, rising cyber claims from ransomware attacks, and global trade pressures hurting marine and cargo profitability. Climate-related losses are also under regulatory review.

The revised Insurance Business Act, effective by May 2026, mandates stronger compliance systems for insurers and agents. Regulators are encouraging independent brokers and curbing cross-shareholdings among major carriers. IFRS reporting is becoming standard for large groups, and a new economic-value-based solvency framework will apply from March 2026.

Property catastrophe reinsurance rates, which had surged since the 2018 typhoon seasons, are now stabilizing. At April 2025 renewals, risk-adjusted rates dropped 10–15% on profitable programs. Property risk business saw 2.5–7.5% cuts for loss-free accounts, while proportional treaties earned commission increases up to 2.5% — the first in years.

Gallagher Re expects Japan’s insurers to prioritize profitability over volume, maintaining strict underwriting standards. The transition to cleaner balance sheets, renewable energy investment, and modernized regulation positions the industry for sustainable, risk-adjusted growth. In short, it’s less about chasing expansion and more about mastering resilience.

……………………..

AUTHORS: Hemant Nagpal – Regional Director, Head of Analytics (APAC) at Gallagher Re, Juivy Tan – Executive Director Cat Analytics (Rest of Asia) at Gallagher Re

Edited by Nataly Kramer – Lead Insurance Editor at Beinsure Media