Overview

The London reinsurance industry sees a growing push toward digital approaches. Enhanced underwriting stands out as a new direction for companies seeking better underwriting decisions and portfolio strategies. Experts project steady gains over the next few years as more participants embrace these methods.

We define Enhanced Underwriting as propositions that use data and digital technology to enhance underwriting decisions, and propositions that have taken a new strategic approach to follow business.

Enhanced underwriting now represents about $5 bn in premiums in the Lloyd’s market. That represents about 7% of Lloyd’s 2023 gross written premiums, according to an The Lloyd’s Market Association (LMA) commissioned a report with consultancy Oxbow Partners titled “The Growth of Enhanced Underwriting in the Lloyd’s Market: The New Normal?” It gathered insights from market participants responsible for 77% of Lloyd’s 2023 gross written premiums.

As the insurance market looks increasingly to digital techniques, “enhanced underwriting” is emerging as the strategic future for the London reinsurance market.

- The LMA set up a committee of chief underwriting officers and managing general agents about 18 months ago. One subgroup focuses on enhanced underwriting.

- The LMA found a huge amount of interest in this group and a lot of MGAs who wanted to be in it or understand what was being discussed.

- The LMA noticed confusion about the models, the taxonomy for enhanced underwriting, and how to craft a strategy.

The committee sought approval from the LMA board to produce a paper defining enhanced underwriting, outlining four main models, and projecting growth and needs over the next 5 to 10 years.

Re/Insurance Market Drivers and Early Adopters

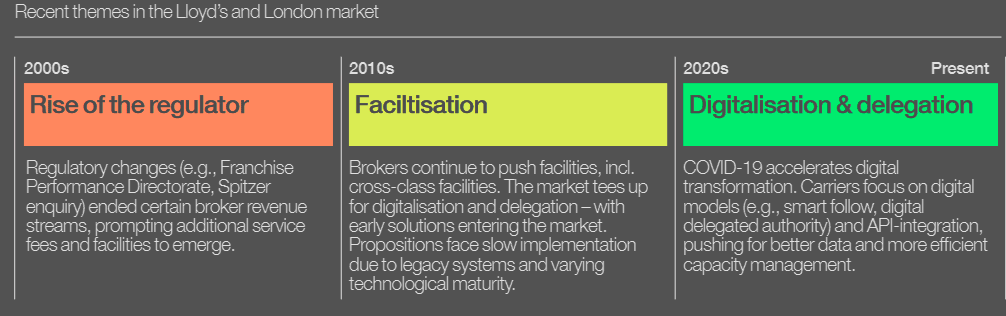

Insurance carriers increasingly invest in technology and data to support underwriting decisions. Many lines in the U.K. personal market went digital in the 2010s. However, complex and specialty segments have only recently seen data-driven tools, such as Ki and Beazley Smart Tracker.

The LMA and Oxbow define enhanced underwriting as any proposition that taps into data and digital tools to boost underwriting decisions or adopts a modern approach to follow business.

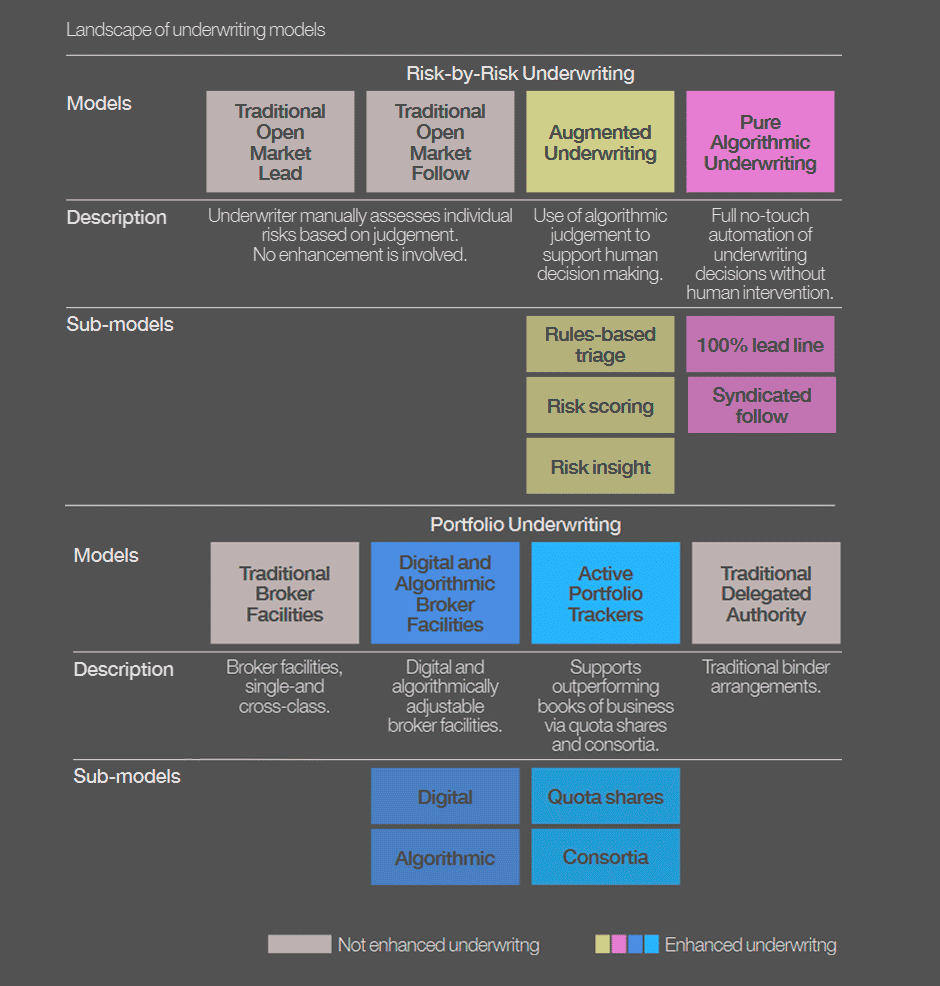

Enhanced underwriting models include risk-by-risk and portfolio categories. Risk-by-risk models add augmented underwriting and pure algorithmic underwriting to the usual open market lead and follow. Portfolio models add digital and algorithmic broker facilities plus active portfolio trackers to existing broker facilities and delegated authority structures.

Ki, part of Brit, has earned a prominent role in this arena. Its pure algorithmic underwriting reached about $877 mn in gross written premiums. Ki, launched in 2020, writes risk by algorithm, offering instant capacity from multiple Lloyd’s syndicates. Brit recently announced that Ki Financial. will operate as a standalone company within the Fairfax Financial Services group starting January 1, 2025.

4 distinct models of Enhanced Underwriting

There are four distinct Enhanced Underwriting models, which split into risk-by-risk underwriting and portfolio underwriting.

Enhanced Underwriting today

Bionic underwriting, augmented underwriting and enhanced underwriting are all terms used in the Lloyd’s and London market to describe digitally enabled underwriting.

We are using this to mean propositions that use data and digital technology to enhance the point of underwriting decisioning, or those that have taken a new strategic approach to follow business.

Note, many carriers are improving the process around the underwriter decision. This includes automated data ingestion, automated workflow, and joining up of systems.

Digitalisation of the market was accelerated by COVID-19

We define this as ‘operational enhancement’ and have not addressed this in detail in this report, although recognise that it is a prerequisite for some forms of Enhanced Underwriting.

- First, Digital and Algorithmic Broker Facilities, where brokers digitalise cross-class facilities. Digital Broker Facilities integrate with brokers’ placing and workflow systems, connecting with carriers via APIs to provide live analytics. Algorithmic Broker Facilities go a step further, allowing carriers to dynamically and digitally change their risk appetite within the facility in-term. There are few live examples of Digital and Algorithmic Broker Facilities in the market. Howden ReThink, launched in 2020, was the first; others such McGill’s Auton are launching in the near future.

- Second, Active Portfolio Trackers identify and provide capacity to high-performing books of business through quota shares and consortia. This is not new; what is new is the explicit strategic focus on this model through emerging follow-only portfolio syndicates – such as Beazley Smart Tracker, Nephila and Hampden Risk Partners – as well as internal Portfolio Solutions teams. These teams describe themselves as ‘proud to follow’.

These underwriters could be characterised as having more of a ‘Portfolio Manager’ role than compared to traditional open market underwriters.

Enhanced Underwriting remains in its early stages

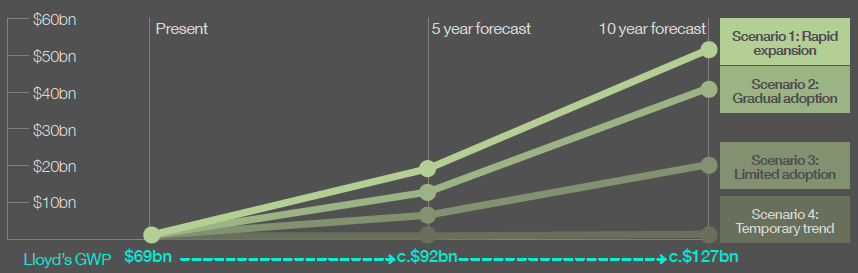

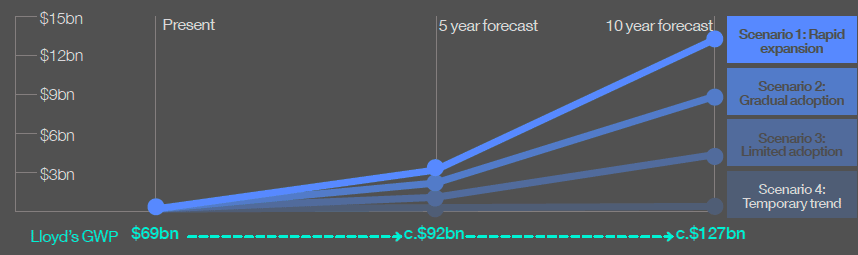

The estimated premiums processed through Enhanced Underwriting models currently stand at around $5 bn, representing roughly 7% of the $69.4 bn in premiums written at Lloyd’s in 2023.

However, premiums provide only part of the picture. Interviews and a market survey identified over 40 Enhanced Underwriting models in development across carriers, MGAs, and brokers, with more firms planning to invest in these capabilities within the next 2-3 years.

These models vary significantly in their level of maturity. Market participants rated the maturity of their Enhanced Underwriting models across five stages. Most reported being in the early phases of development.

Growth Projections and Key Findings

The LMA report drew from interviews with 85 senior leaders across 55 Lloyd’s companies. These leaders see enhanced underwriting as young but rapidly expanding. Over the next five to 10 years, 35% expect fast market-wide growth, while 65% foresee gradual adoption. No one predicts limited or declining use.

Pure algorithmic underwriting and active portfolio trackers may each grow by about 20% per year. Augmented underwriting could grow by about 60%. Digital and algorithmic broker facilities might rise by around 50% from a lower base.

The LMA highlights Beazley’s Smart Tracker Syndicate, active for about seven years, which was set up to write on an enhanced basis. The LMA’s new enhanced underwriting group, chaired by Beazley, includes members from across the Lloyd’s market.

New Models, Distribution, and Efficiency Gains

London has historically operated through syndication, with leaders offering terms and followers filling in capacity. In earlier years, brokers gathered numerous follow markets to complete placements after finalizing lead terms. This process required many people and often proved inefficient.

New digital channels now allow a swift follow capacity that provides clients with immediate cover behind approved leaders. Large shares of London market orders flow into broker facilities and Lloyd’s consortia, built with scientists, actuarial analysis, and underwriting judgment to optimize portfolios.

Augmented Underwriting

Taking each model individually, Augmented Underwriting accounts for only $0.3bn of the $5bn of premium

associated with Enhanced Underwriting models.

However, interviews with carriers suggest that there are over 15 Augmented Underwriting models in the market. The low premium is largely driven by the low maturity of those taking part. While many carriers are conducting ‘Tight Experimentation’ with rules-based triage, risk scoring and risk insight, there is limited live premium currently

flowing through.

The key challenge is retrofitting new technology and data into existing workflows. This is compared to new models that tend to be greenfield.

Despite this, Augmented Underwriting was widely accepted as ‘logical’ and ‘valuable’ in interviews, citing dual

benefits of more streamlined processes and enhanced underwriter decision making.

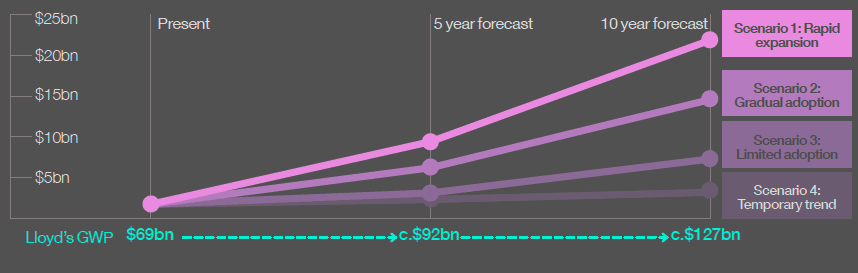

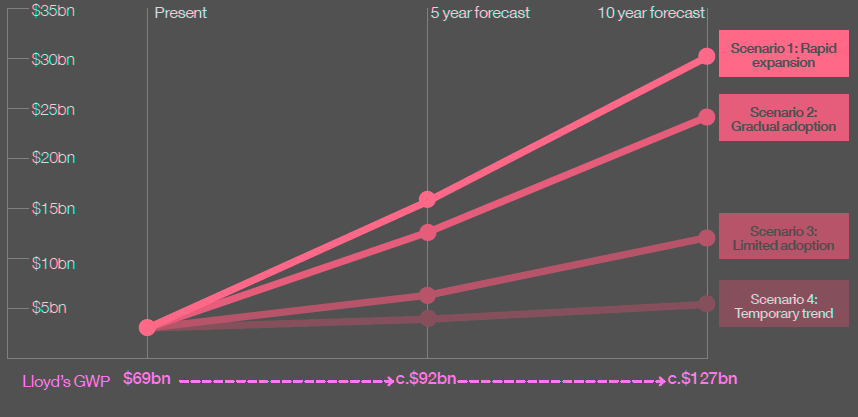

Augmented Underwriting could grow to c.$42bn in 10 years

Pure Algorithmic Underwriting

Pure Algorithmic Underwriting currently represents $1.7bn in premium. This is driven primarily by Ki ($877m – 2023 GWP), the most established syndicated follow vehicle. Other sources of premium come from no-touch quote and bind systems – such as Aegis Opal and Atrium’s AU Gold. These models are typically focused on highvolume, low-value business.

We identified eight established Pure Algorithmic Underwriting propositions in the market, which account for the 20% of vehicles reported to be above ‘Strategic Foundations’.

In the survey, a number of participants also indicated that they are in the ‘Awareness’ stage of Pure Algorithmic Underwriting (47%) – often viewing straight-through processing as the end state for segments of their Augmented Underwriting.

Pure Algorithmic Underwriting could grow to c.$15bn in 10 years

Digital and Algorithmic Broker Facilities

Digital and Algorithmic Broker Facilities make up the smallest proportion of premium associated with Enhanced Underwriting. There are currently few examples of Digital and Algorithmic Broker Facilities in the market, and most

(>60%) are in the ‘Awareness’ and ‘Tight Experimentation’ stages of maturity.

In interviews, many brokers were still evaluating whether a Digital or Algorithmic Broker Facility should be part of their strategic roadmap – either by digitising current or creating new digital facilities.

Others expressed the view that digitalisation was becoming part of their value proposition and that they were actively developing a Digital or Algorithmic facility. For example, McGill’s Algorithmic Broker Facility, Auton, is about to go live. As brokers continue to debate to what extent digitalisation of cross-class facilities is a priority, the maturity of these models will likely remain below ‘Strategic Foundations’.

Digital and Algorithmic Broker Facilities could grow to c.$9bn in 10 years

Active Portfolio Trackers

Active Portfolio Trackers account for the biggest proportion of premium (c.60%) flowing through Enhanced Underwriting models. This is made up of standalone followonly syndicates – such as Beazley Smart Tracker, Nephila and Hampden Risk Partners – as well as internal Portfolio Solutions teams.

Active Portfolio Trackers are also the most mature model, with 60% in the ‘Scaled Execution’ stage. This is largely because the underlying methods, such as placement through consortia and quota shares, are well established.

Additionally, Portfolio Solutions teams operate separately from traditional models, allowing teams to scale

quickly without being hindered by legacy processes.

Regulation matters for continued progress in enhanced underwriting. Lloyd’s monitors each syndicate’s performance, reviews strategies, and examines business plans.

Active Portfolio Trackers could grow to $24bn in 10 years

Our projections assume that rapid growth of Active Portfolio Trackers would require the majority of large carriers to have mature, optimised vehicles in the next 10 years.

Current follow-only portfolio syndicates would continue to grow, and the span of GWP written by Portfolio Solutions teams will continue to expand.

The adoption of Active Portfolio Trackers relies on the delivery of cost efficiency in capacity deployment. While there are already established vehicles, they will need to maintain low administrative ratios as they scale.

The impact of Enhanced Underwriting on the market

Algorithmic Business Models Are Gaining Traction

There is growing consensus that homogenous, less complex risks are increasingly suited for algorithmic underwriting. Platforms such as Vave, Aegis Opal, and AU Gold are leading this shift. Supporters believe these pure algorithmic models could expand market reach in London by tapping underserved segments, effectively “growing the pie.” Many interviewees predicted a steady rise in digitally tradable risks.

However, some expressed doubts about the sustainability of this model within London’s portfolio. They questioned whether commoditised risks align with the market’s focus and warned that such business could exit the market if conditions soften.

Market Bifurcation Between Lead and Follow Capacity

The rise of Enhanced Underwriting is driving a clear split between lead and follow capacity. Historically, insurers applied similar operating models across both, failing to account for the unique skills and processes required to lead versus follow on a risk. This traditional approach led to inefficiencies and higher costs.

Now, carriers are shifting strategies to focus on their true lead roles. They are adopting Augmented Underwriting models to strengthen risk assessment and accelerate decision-making.

This enables them to better manage complex, high-value risks, increasing their influence as lead underwriters.

Interviewees noted that true leads will increasingly attract automated follow capacity. In this setup, lead underwriters would hold more control over capacity allocation and market risk assessment. Their robust underwriting practices would be critical to ensuring quality risk evaluation.

Economic Models Are Still Evolving

Enhanced Underwriting models differ significantly from traditional open-market underwriting, particularly in acquisition costs, administrative expenses, and loss costs. These newer approaches aim to streamline follow capacity at a lower cost by transferring much of the underwriting process—such as risk assessment and pricing—to lead underwriters.

As a result, carriers have explored charging fees for lead roles in consortia or facilities to reflect this workload shift. Similarly, brokers suggested higher fees for digital and algorithmic facilities due to the added services they provide.

Despite these developments, Enhanced Underwriting remains in its early stages. Economic performance data is still limited, and most companies remain cautious about disclosing results. However, anecdotal evidence from interviews suggests potential for improved profitability through reduced administrative costs and more efficient risk placement.

Opportunities and Risks for London

Opportunity: Access to New or Underserved Markets

Enhanced Underwriting opens doors to new and underserved markets for London. Technologies like algorithmic quote-and-bind platforms allow carriers and brokers to connect with clients worldwide and underwrite risks even in regions lacking a physical presence.

This is particularly relevant for products such as wind-deductible buyback insurance within the global renewable energy sector. While carriers must still meet local regulatory requirements, Enhanced Underwriting is viewed as a chance to expand London’s market reach, with one interviewee describing it as “an opportunity to increase the size of the pie.”

Risk: Losing the Power of the Syndicated Market

There is concern that Enhanced Underwriting could undermine the current syndicated market structure. Digital platforms may give lead underwriters more control, increasing their line sizes.

However, this shift risks creating a “blind follow” culture where followers rely too heavily on leaders without independent assessments. The existing model ensures robust decision-making, with followers acting as a critical second set of eyes to verify the leader’s decisions.

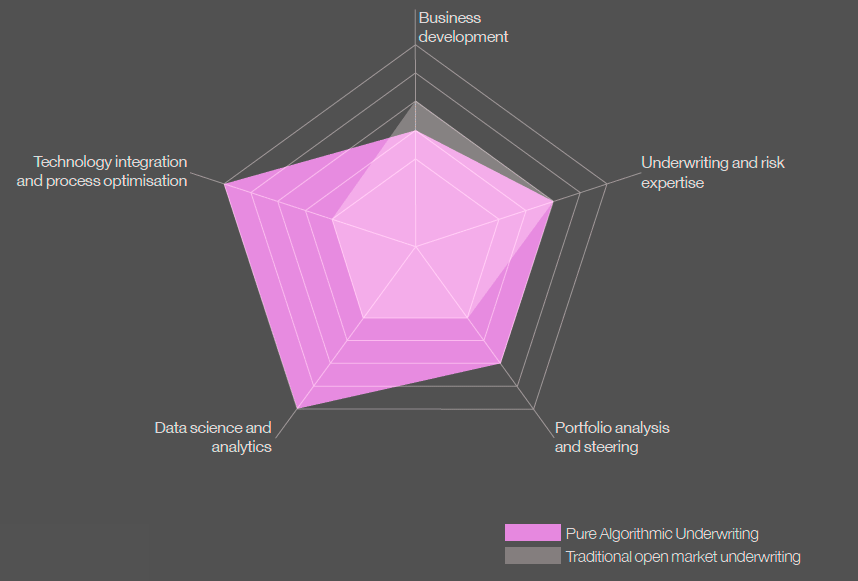

Pure Algorithmic Underwriting requires extensive technology integration

Opportunity: Attraction of Third-Party Capital

Specialty insurance has drawn interest from third-party capital providers due to strong returns and its low correlation with traditional markets. Enhanced Underwriting may attract even more capital through initiatives like Insurance-Linked Securities (ILS) and structures such as the London Bridge Risk (LBR) Protected Cell Company. However, capital providers remain cautious.

While they support the Enhanced Underwriting approach, they prefer to see proof of sustained performance before making additional investments.

Increased digitalisation, risk data standardisation, and performance insights are key drivers for attracting this capital. Improved data capture and analysis could strengthen Lloyd’s appeal to international investors by offering more transparency and reliability.

Risk: A ‘Lost Generation’ for Talent

The push for efficiency through Enhanced Underwriting often involves automating lower-complexity tasks. This shift raises concerns about training the next generation of underwriters. Traditionally, junior staff develop skills through tasks like data entry and basic risk assessments.

If these tasks are automated, younger professionals may miss out on valuable learning opportunities. While humans adapt over time, the immediate challenge is ensuring that early-career professionals gain enough exposure to build expertise.

Opportunity: Potential Flattening of the Cycle

A key benefit of Enhanced Underwriting is better access to data, leading to improved risk assessments. This deeper understanding could reduce the market’s exposure to traditional underwriting cycles. Executives have suggested that cycles may flatten or become more specific to particular classes of business.

Active Portfolio Trackers and broader use of broker facilities may contribute to longer-term certainty in follow capacity. However, most broker facilities still operate under one-year contracts. For the full potential to be realized, longer-term contracts for follow capacity may be needed, potentially requiring regulatory changes at Lloyd’s.

Risk: Dilution of London’s Value Proposition

The London market has built its reputation on underwriting complex and bespoke risks. Critics argue that Enhanced Underwriting could dilute this identity by focusing on more commoditised risks. There is concern that digitalisation may erode the market’s hallmark physical experience, where clients and brokers value personal interactions and negotiations.

The challenge lies in preserving London’s unique selling points—its human expertise and physical presence—while embracing technological advancements. Critics question whether digital tools can match the responsiveness of human underwriters during major loss events.

Opportunity: Validate London’s Competitive Edge in the Digital Age

Enhanced Underwriting offers a chance for London to maintain its leadership in the evolving insurance market. As a historic center of innovation, the London market can leverage digital solutions to stay relevant and competitive.

Lloyd’s strength lies in its ability to bring competitors together to collaborate for the benefit of clients—a concept known as “coopetition.” Both supporters and sceptics agree that coopetition will be essential for Enhanced Underwriting’s success. Through collaboration, carriers can accelerate innovation and deliver new products and services to meet clients’ evolving needs.

FAQ

Enhanced Underwriting refers to the use of digital tools and data to improve underwriting decisions and streamline portfolio management. It involves risk-by-risk models and portfolio-based approaches to optimize capacity allocation and enhance efficiency. The London Market Association (LMA) defines it as propositions that enhance underwriting decision-making or introduce new strategic follow-business models.

Enhanced Underwriting accounts for approximately $5 bn in premiums, representing about 7% of Lloyd’s gross written premiums in 2023. The LMA report, conducted with Oxbow Partners, gathered insights from participants responsible for 77% of Lloyd’s premiums that year.

The four models are split between risk-by-risk and portfolio underwriting approaches:

1) Augmented Underwriting – Uses advanced data and tools to enhance human decision-making.

2) Pure Algorithmic Underwriting – Relies on fully automated systems to assess and bind risks.

3) Digital and Algorithmic Broker Facilities – Integrates brokers’ placing systems with carriers through APIs for real-time analytics.

4) Active Portfolio Trackers – Focuses on managing portfolios through quota shares and consortia.

Enhanced Underwriting is transforming how capacity is allocated, reducing reliance on traditional manual processes. The use of data-driven tools has allowed insurers to reach underserved markets, improve efficiency, and attract third-party capital. However, it has also raised concerns about potential talent gaps and the dilution of London’s unique value proposition.

Key participants include Brit’s Ki, a prominent algorithmic underwriting platform, and Beazley’s Smart Tracker Syndicate, which focuses on follow-only underwriting. Other notable players include McGill’s Auton and broker facilities such as Howden ReThink. These models are supported by internal Portfolio Solutions teams within various Lloyd’s syndicates.

Enhanced Underwriting models are expected to grow significantly over the next decade. Augmented underwriting could reach $42 bn in premiums, pure algorithmic underwriting could hit $15 bn, and digital broker facilities may grow to $9 bn. Active Portfolio Trackers, which currently represent the largest share, could expand to $24 bn.

Enhanced Underwriting faces several challenges:

1) Talent Development: Automation risks creating a “lost generation” of underwriters by removing entry-level tasks traditionally performed by junior staff.

2) Market Identity: Critics warn that focusing on commoditised risks may dilute London’s reputation for handling complex, bespoke risks.

3) Technology Reliance: There are concerns about how well digital tools can handle major loss events compared to human underwriters.

Despite these challenges, Enhanced Underwriting is seen as crucial for London’s continued leadership in the global insurance market.

…………..

AUTHORS: Greg Brown – Partner, Oxbow Partners, Max Deacon – Principal, Oxbow Partners, Eleanor Ewen – Oxbow Partners Senior Consultant, Struan Hancock – Oxbow Partners Consultant, Elias Formaggia – Oxbow Partners Consultant