Overview

According to a ranking and analysis completed by Insuramore, the value of revenues earned worldwide by MGAs, MGUs and cover-holder groups (a.k.a. delegated underwriting authority groups) was around USD 12.5 billion, implying premiums intermediated by such groups in that year of approximately USD 100 billion.

However, at a global level, the market for this type of intermediary (“the MGA market”) is a fragmented one. The top five groups are thought to have accounted for a combined 18.2% of worldwide revenues, rising to 39.6% for the top 20, 56.9% for the top 50, 68.5% for the top 100 and 82% for the top 250.

Worldwide ranking insurance broking groups

Placed a respective first, third, fourth and fifth in the worldwide ranking came broking groups Brown & Brown, Amwins, Ryan Specialty Group and Truist Insurance Holdings. Meanwhile, given disclosures made by it in advance of its planned public listing, classic vehicle specialist Hagerty may reasonably be assumed to have come second in the ranking.

Revenues earned worldwide by MGAs, MGUs and cover-holders had a value of around USD 12.5 billion. 55 of the top 250 MGA groups (including four of the top five) belong to insurance brokers while 28 are owned by insurers. The rapid growth of MGA revenues relative to mainstream broking revenues is due to several factors including the development of specialized risk classes

Insuramore’s analysis of the revenues of MGA / MGU / cover-holder groups – with data for a majority of groups covers up to the top 300 groups worldwide by this measure. Together, these 300 groups accounted for an estimated 85.8% of total revenues earned by these types of group.

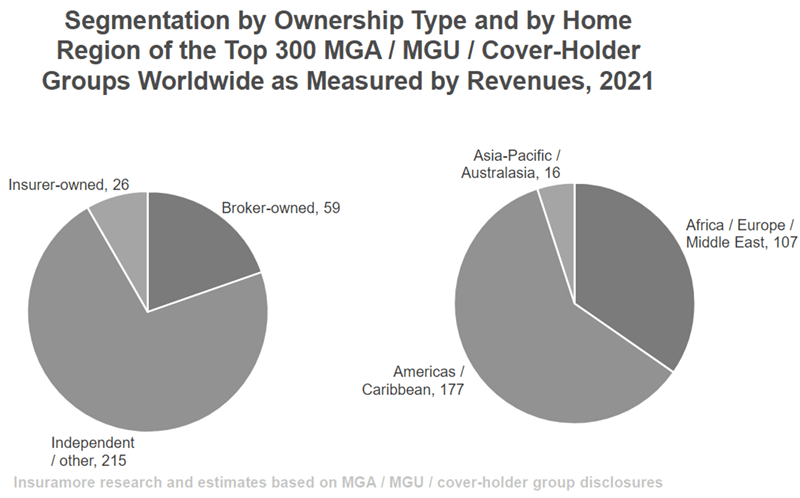

Segmentation of MGA / MGU Insurance Groups Worldwide

By ownership, 55 of the top 250 groups in this space are classifiable as broker-owned, 28 as insurer-owned and the remaining 167 as independent (albeit many of these are backed by private equity firms). Furthermore, by type of insurance underwritten, 73 can be defined as specialist groups (i.e. MGAs underwriting a single product class or a small number of closely-related ones, such as cyber and technology E&O, or private auto and home) with the rest classifiable as multiline players.

How many individual MGA enterprises worldwide?

Finally, by location, 145 of the groups are identifiable as based in the Americas (with 134 of these in the US), 90 in Africa, Europe or the Middle East (including 46 headquartered in the UK), and 15 in the Asia-Pacific region or Australasia.

In total, Insuramore believes that there are around 1,000 groups globally in the MGA space adding up to approximately 2,000 individual MGA enterprises worldwide given that many of the larger groups own multiple MGAs.

Moreover, launches of new MGAs have been coming thick and fast in recent times; typically, such new entrants are seeking to take advantage of opportunities afforded by use of advanced technologies (i.e. insurtech) to bring about digital disruption in established market segments. On the other hand, the origins of some MGAs date back more than 100 years.

Revenues in the global MGA market

Partly because of this development of new MGAs, revenues in the global MGA market are likely to have been growing more rapidly in recent years than those in the (much larger) insurance broking sector (with total revenues valued by Insuramore at USD 117.7 billion).

Other factors have been superior growth in segments of the insurance market traditionally served by MGAs (notably, the market for excess and surplus cover in the US) plus the emergence of specialized risk classes for which the need for highly customized underwriting makes them well-suited to the MGA model, one of the most obvious of these being cyber.

Nevertheless, in keeping with the broader broking market, the MGA space is also characterised by significant acquisition activity; of the 250 leading MGA groups at the end of year, 12 are known to have been taken over by the date of this press release. Indeed, a key strategic question for both broking and insurer groups in future is the extent to which they should gain or increase their exposure to MGA activity via acquisitions.

With regards to the latter, the leading insurer-owned MGA clusters are estimated by Insuramore to have been Zurich (mainly through its ownership of crop insurance provider RCIS) and Tokio Marine (whose MGA portfolio includes renewable energy specialist GCube and ProAg, another crop insurance provider, among others).

MGA, MGU and cover-holder revenues

MGA, MGU and cover-holder revenues are defined as fees and commissions earned from underwriting / program administration (and related activities) by entities with the authority to underwrite or bind insurance (or reinsurance) risk in any class and that do this exclusively or mainly on behalf of unaffiliated carrier partners (see Global Reinsurance Sector Outlook).

Such entities that are insurer-owned and that are believed to place risks exclusively or mainly with parent or sister underwriters (i.e. affiliated entities) are excluded from the analysis. Revenues from wholesale or other broking / agency activity that do not meet this definition of MGA, MGU or cover-holder business are also not in scope.