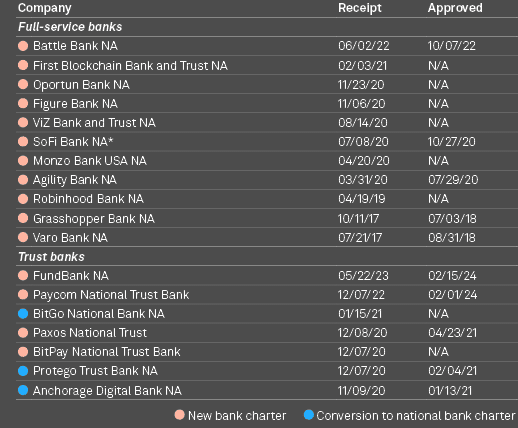

FinTech companies are increasingly looking into the possibility of getting bank charters, though few have actually taken the plunge, according to S&P Global Market Intelligence.

Heightened regulatory scrutiny in banking-as-a-service (Baas) has fintechs taking fresh stock of their reliance on bank partners.

However, if deploying deposits for lending is not core to their business models, fintechs have tended to walk away from getting their own bank charters.

The number of inquiries we got increased, but the number of people who wanted to follow through on that has not been all that high.

The FinTech sector saw a surge in mergers and acquisitions in 2024. Companies aimed to expand their market share and integrate advanced technologies. Key drivers included the desire to enhance digital capabilities and meet customer demands.

Significant deals shaped the competitive landscape. Traditional financial institutions and tech companies formed strategic partnerships. This trend underscored the growing importance of innovation and technology integration in finance.

Several high-profile acquisitions marked the year. Leading firms acquired startups to bolster their service offerings and enter new markets. These moves highlighted a focus on expanding digital payment solutions, blockchain technology, and cybersecurity measures.

Regulatory considerations played a crucial role. Companies navigated complex legal frameworks to finalize their deals. This aspect emphasized the importance of compliance and strategic planning in M&A activities.

Fintechs have been able to obtain a bank charter

Inquiries spiked during the March 2023 turmoil that saw several crypto-connected banks fail, Crane said, and also picked up following recent incidents around Evolve Bank & Trust.

BaaS provider Evolve and its middleware vendor Synapse Financial Technologie, which filed for bankruptcy in April, encountered issues in reconciliation that caused difficulties with distributing funds to depositors because ledger records did not match.

Regulators have been paying particularly close attention to the BaaS space as of late. Evolve is one of many BaaS providers that have received severe enforcement actions in the past 12 months. With that backdrop, some fintechs have considered bank charters to get more control over their destiny.

That interest has only increased with some of the recent enhanced scrutiny by the federal prudential regulators on bank-fintech partnerships.

The global fintech market, valued at $272 bn in 2023, is projected to reach $723 bn by 2030 and $1.265 trln by 2034, growing at a CAGR of 15%, according to Beinsure Media forcast.

Fintech innovations have accelerated the digital finance revolution. This growth has democratized investing. Fintech M&A deals remains high, driven by consolidation, strategic banking initiatives, and evolving investor preferences. Traditional banks are acquiring fintech companies to stay at the forefront of financial innovation and enhance adaptability and customer-centricity.

Alignment with its core business, rather than uneasiness with bank partners, should take precedence when a fintech considers a bank charter. A key element in the business model is the need to use deposits to reduce funding costs and maintain liquidity.

UK small business lender OakNorth Bank is one of the fintechs pushing full steam ahead with getting a charter as it makes inroads in the US market.

It is currently searching for a US bank target and is open to other options, including a de novo bank charter application. It makes sense for a fintech to have a bank charter for small business lending because of the benefit of deposits and the strong community ties in small business banking.

by Peter Sonner

by Peter Sonner