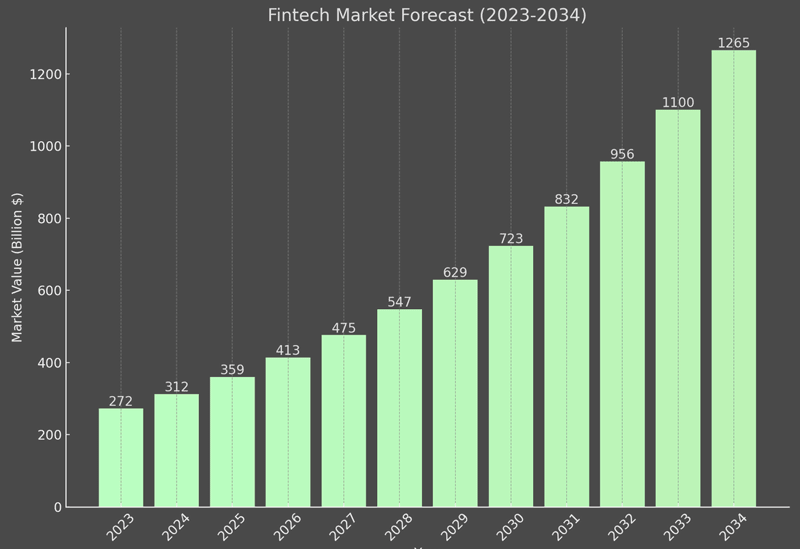

The global fintech market, valued at $272 bn in 2023, is projected to reach $723 bn by 2030 and $1.265 trln by 2034, growing at a CAGR of 15%, according to Beinsure Media forcast.

Fintech innovations have accelerated the digital finance revolution. This growth has democratized investing. Fintech M&A deals remains high, driven by consolidation, strategic banking initiatives, and evolving investor preferences. Traditional banks are acquiring fintech companies to stay at the forefront of financial innovation and enhance adaptability and customer-centricity.

Commission-free trading apps attract millions of new retail investors by offering zero-commission transactions, making stock market investments more affordable.

Automated savings apps are also gaining traction. Research from Cornerstone shows that among the 13% of U.S. consumers using them, almost $17 bn has been generated in additional deposits (see Biggest FinTech Unicorns).

This indicates we are on the brink of the next major evolution: the rise of super-apps. These platforms aim to consolidate various financial and lifestyle services into a single, seamless interface.

Fintech Market Forecast for 2024-2034

Key tech players saw this integration potential early. META integrated payments into WhatsApp, while Apple and Google did the same within their mobile operating systems.

In China, super-apps have gained significant traction. From 2015 to 2023, WeChat’s revenue increased from $3.6 bn to $16.38 bn.

Fintech Market Value Forecast

| Year | Fintech Market Value, bn $ |

| 2023 | 272 |

| 2024 | 315 |

| 2025 | 360 |

| 2026 | 410 |

| 2027 | 480 |

| 2028 | 550 |

| 2029 | 630 |

| 2030 | 725 |

| 2031 | 830 |

| 2032 | 960 |

| 2033 | 1100 |

| 2034 | 1265 |

The fintech market refers to the connection between financial services and technology. It comprises the use of innovative technologies and digital solutions to provide financial products, services, and processes.

Fintech companies’ stimulus expansions in applications such as mobile apps, artificial intelligence, blockchain, data analytics, and cloud computing to dislocate and advance several features of the financial industry.

Fintech companies provide financial technology solutions, tools, and services to other businesses (B2B). Advances in AI, blockchain, cloud computing, and big data analytics have enabled the creation of innovative fintech solutions.

These advancements have boosted the fintech sector by making financial services more convenient, secure, and efficient. Clients increasingly rely on digital platforms for their financial needs.

Fintech areas such as peer-to-peer lending, robo-advisors, and mobile payment apps have gained popularity due to the demand for user-friendly, personalized, and efficient financial solutions.

However, regulatory guidelines for fintech vary widely across regions and can be complex and dynamic. Complying with these regulations can be costly and time-consuming, especially for new and smaller companies (see report Private Equity & Venture Capital Investment in FinTech).

Fintech companies attract hackers because they handle sensitive financial data. Strong cybersecurity measures are essential to protect against fraud, data breaches, and other security threats.

Fintech sector saw M&A activity rise

While global M&A has suffered in 2024, the Fintech sector saw M&A activity rise sharply this year, with 600+ deals recorded. This represents a 46% increase on numbers, and a whopping 70% increase on pre-pandemic figures.

2024 saw the trailing 30-month median revenue multiple reach 3.1x – broadly in line with the levels seen in the past two years.

The trailing 30-month median EBITDA multiple came in at 14.2x, firmly within the 13x to 15x range monitored since 2015.

The slashed valuations of some publicly traded financial technology companies will continue to prompt Fintech M&A interest from strategic and private equity buyers.

Many fintech companies went public with lofty valuations during the latest peak around 2022 only to see their share prices plummet in 2023-2024.

The market correction emerged as public market investors began prioritizing profitable companies over those prioritizing growth at any cost.

- Deal Volume and Value: The overall number of M&A deals in the FinTech sector showed significant activity, with nearly 600 private FinTech deals recorded between 2022-2024.

- Large Transactions: Capital One’s pending $35 bn acquisition of Discover was a standout, marking one of the largest FinTech M&A deals ever.

- Deal Structures and Valuations: FinTech valuations have declined, making the sector attractive for buyers. The median revenue multiple range was 3.4x to 7.2x as of 2024, about 30% lower than in 2021.

- Geographic and Sector Variations: While the Americas, particularly the United States, dominated megadeal activity, regions like EMEA and Asia-Pacific experienced declines in deal volumes due to challenging economic conditions.

Many high-growth but unprofitable or break-even businesses, which were valued based on revenue multiples, experienced significant valuation cuts, sometimes by nearly half. In contrast, the valuations of profitable businesses were less affected.

The global M&A market experienced a notable surge across all industries, prompting analysts to question the sustainability of such highs.

………..

by Peter Sonner – Editor at Beinsure Media

by Peter Sonner – Editor at Beinsure Media