Overview

While global M&A has suffered in 2024, the Fintech sector saw M&A activity rise sharply this year, with 600+ deals recorded. This represents a 46% increase on numbers, and a whopping 70% increase on pre-pandemic figures.

According to Hampleton Report, valuations have remained steady: 2024 saw the trailing 30-month median revenue multiple reach 3.1x – broadly in line with the levels seen in the past two years. The trailing 30-month median EBITDA multiple came in at 14.2x, firmly within the 13x to 15x range monitored since 2015.

The slashed valuations of some publicly traded financial technology companies will continue to prompt M&A interest from strategic and private equity buyers.

Many fintech companies went public with lofty valuations during the latest peak around 2022 only to see their share prices plummet in 2024.

The market correction developed as public market investors shifted their focus to profitable companies and away from those growing at all costs.

Many high-growth but break-even or unprofitable businesses valued off of revenue multiples have faced a material valuation cut, which in some cases could be by nearly half, while the valuations of profitable businesses are less impacted.

The global M&A market saw a sizeable spike across all industries, leading many analysts to question whether such highs would be short-lived.

Their skepticism proved correct: early into 2023, broader market confidence deteriorated as several geopolitical and macroeconomic events made headlines, including post-pandemic inflationary pressures, armed conflict in Ukraine, broken supply chains, and central banks hiking interest rates in an attempt to curb inflation.

Driving this year’s sharp increase in Fintech M&A are many deals in the Payments, Crypto & Blockchain, and Banking & Lending segments

- Fintech is poised for a surge in M&A deal activity. The fintech sectors likely to see most deal activity include: open banking, neobanks, regtech, greentech, paytechs (including embedded finance and buy now, pay later) and central bank digital currency and its digital infrastructure providers

- In part, this activity will be characterized by the consolidation of fintech companies, in order to strengthen finances and speed up growth strategies and scale

- Recent events in the global banking sector will make it harder for some fintech companies to raise finance and achieve significant growth organically. This will also drive M&A as a growth strategy

- Fintech companies will also look to form strategic partnerships with larger corporations, in order to leverage their wider customer bases and brands and drive up scale and customer acquisition

FinTech M&A deals

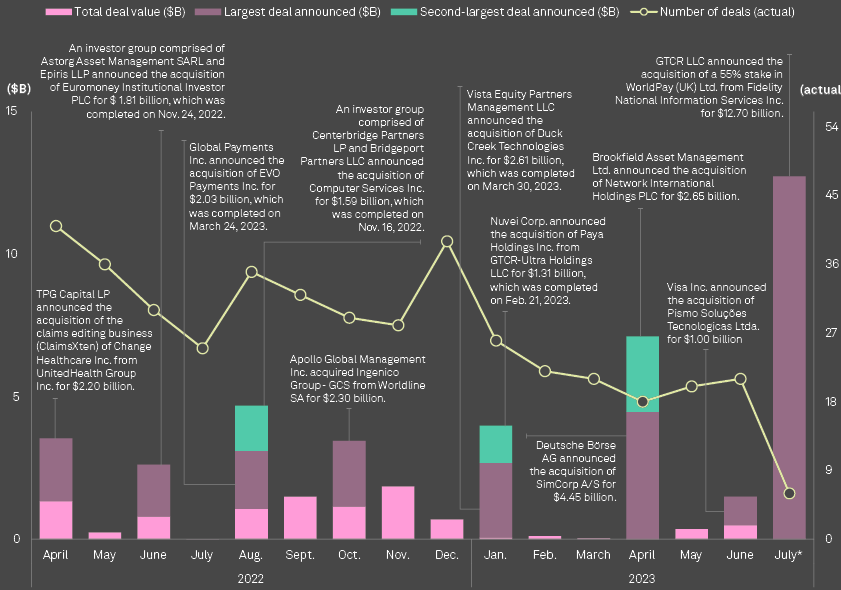

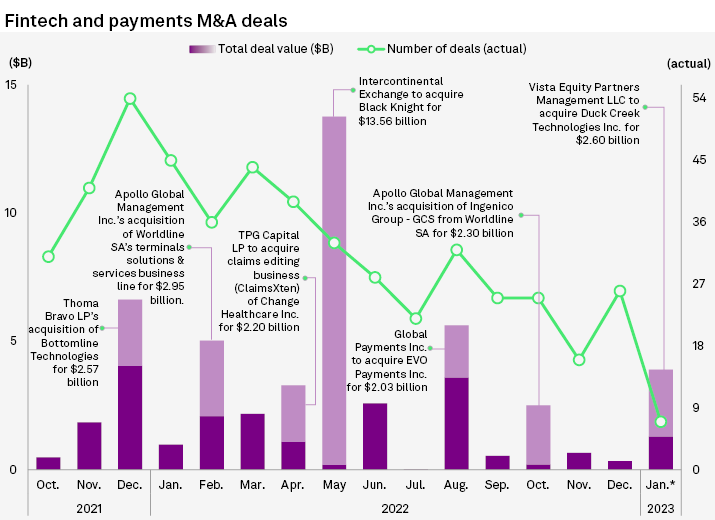

The gloomy deal market had a bright spot in July, when banking software company Fidelity National Information Services Inc. unwound its 2019 acquisition of Worldpay Group Ltd. and sold 55% of the payment processing company to GTCR LLC at an announced valuation of $12.7 billion, according to Global FinTech & InsurTech Funding Highlights.

But the deal was a planned strategic move and does not necessarily reflect the M&A appetite in the broader market.

In many developed jurisdictions only companies authorized by a financial regulator are allowed to access financial data or to initiate payments on a customer’s behalf. This access to data allows those third parties to develop new products and services that customers can use to manage their finances in new and innovative ways.

The objective is to simplify how financial information is retrieved, shared, processed and presented.

A good example of this is the use of open banking data to deliver an efficient and streamlined credit application process, whereby lenders are able to analyze a potential borrower’s financial standing based on multiple data points such as income and outgoing payments to run an affordability assessment on the proposed loan.

This sector has faced challenges related to public awareness and market perception and is likely to experience M&A consolidation.

With economic uncertainty remaining persistent, targets in recent deals are locking in the market premium offered by the buyer instead of waiting for a rebound of stock prices.

This sentiment among sellers has the potential to pick up in 2023, and there is no shortage of smaller publicly traded fintech companies — particularly in the payments sector — that private equity firms or larger corporate players can covet, according to equity analysts.

Customer uptake of payment initiation services in particular has been low, often due to a general lack of awareness and understanding of the products themselves.

Since payment card fees are charged to the merchant and not to the customer, there is little direct incentive for customers to switch payment methods.

FinTech M&A market in 2024

The FinTech mergers and acquisitions (M&A) market has been dynamic and evolving, characterized by several key trends:

- High Activity Levels

- Payments Sector Dominance

- Disruptions and Deal Value Changes

- Integration with Established Financial Institutions

- Strategic Realignment in Financial Services

- Financial Crime Prevention Solutions

- Growth of Payment Service Providers

- Global Expansion and Sector Headwinds

- AI’s Transformative Impact and Data Analytics Focus

- Digital Evolution in Banking

Fintech M&A activity remains high, driven by consolidation, strategic banking initiatives, and evolving investor preferences. Traditional banks are acquiring fintech companies to stay at the forefront of financial innovation and enhance adaptability and customer-centricity.

Over 50% of all fintech M&A deals were in the payments sector, a significant increase from 17%. This growth is attributed to technological advancements, major tech companies entering the payment market, and the fragmented nature of the payment sector.

The financial sector witnessed disruptions, such as UBS acquiring Credit Suisse for USD 3.25 bn – saw a decrease in both deal value and volume, with 130 acquisitions totaling USD 4 bn.

Fintech firms capable of seamlessly integrating with traditional banks and financial institutions are increasingly sought after, creating symbiotic relationships that bridge innovation and stability.

Focus on B2B Ecommerce and Credit Risk Management: In B2B ecommerce, there is a significant focus on credit and payment terms, leading to strategic acquisitions like Sidetrade’s acquisition of CreditPoint Software for EUR 3 mn.

Notable developments include FIS divesting its majority stake in Worldpay to GTCR for USD 18.5 bn, reflecting the need for streamlined operations and management focus.

Payment service providers are seeking synergies, cost savings, and strategic market access. Companies like Nexi are making strategic moves, like acquiring a 30% stake in Computop, to expand in the ecommerce space. Companies like Rapyd are expanding globally, as seen in its USD 610 mn acquisition of PayU GPO. The Buy Now, Pay Later (BNPL) sector faced adjustments in valuation and share price declines.

The anticipation of AI’s transformative impact is driving M&A activities, with companies like Equifax and Payoneer acquiring firms to enhance their AI and data analytics capabilities.

European banks are acquiring equity and debt funds and forming strategic partnerships in response to the digital revolution. Examples include Citi’s sale of its Taiwan consumer unit to DBS and Alpha Bank’s acquisition of Orange Money Romania.

FinTech M&A market presents a blend of risk, innovation, and adaptation, with incumbents seeking strategic partnerships and consolidation opportunities to enhance their digital capabilities and address regulatory pressures

Fintech M&A will display resilience in a stormy market

A potential recession won’t dampen Fintech M&A as it did in 2008

While global M&A has suffered, Fintech M&A is expected to remain robust despite concerns of a possible market downturn.

Analysts point to a determining difference between now and the 2008 recession: deployable private capital (buyout, VC, growth, real estate, etc.) has reached its highest ever level at $3.6 trillion, representing around three times that of 2008.

The availability of capital drives buyers and investors to increase their acquisitions at a time when their pockets are full and high-growth Fintech companies are being sold at affordable prices.

In addition, a survey conducted by Bain Capital shows that deals completed during recessions tend to deliver healthy returns, something executives learned in the wake of the 2008 financial crisis.

Share of PE fintech acquisitions stable

The number of private equity acquisitions of fintech targets has increased, while the share of PE acquisitions as a percentage of total number of deals remains in line with prior periods at 31%.

Following recent turmoil across the broader tech sectors in Europe and North America, investors saw risk in deploying capital in Q2. Interest rate hikes also justified greater caution in making acquisitions.

Such hesitation is dissipating, however, as PEs rush to utilise available capital to prevent inflation from eating into their purchasing power. Overall, 2023 PE investment into Fintechs is on track to outpace prior years.

Paytechs cover a wide range of services in the payments value chain, including payment service providers and payments facilitators (PayFacs), networks creating new payment solutions and payment technology suppliers.

Embedded payments and embedded finance form an important feature of the evolving payments industry. The concept of embedded finance has been around for a while in different shapes and forms, but continues to be one of the fastest growing sectors in fintech.

Top recent Fintech acquirers organised by the geography of their latest target

Top deals in FinTech

Neobanks have seen a rapid expansion in recent years and offer huge appeal to tech-saavy customers seeking easy, hassle-free banking options. Sometimes referred to as “challenger banks,” they have been compared to digital disruptors in other industries.

Neobanks are a type of digital financial institution that operate exclusively online, without traditional physical branch networks.

They often start life as non-bank financial institutions (engaged in payment services and/or electronic money), before evolving over time to secure a full banking license. The customer appeal is usually in the modern marketing messaging and social media interactions, user-friendly apps and a seamless digital experience.

Usually there are no account fees, no monthly balance requirements and account opening is a quick and easy process. Some of those neobanks that go on to obtain banking licenses are able to offer higher interest rates on savings due to their lower operating costs compared to High Street lenders.

Top acquirers in FinTech

Norway-based Visma graduate to top acquirer with 17 deals closed over the past 30 months. Visma has been expanding its geographic reach in the EMEA region by swiftly acquiring targets. Most recent targets operated in the Benelux region, Poland, Spain, Denmark, and Sweden.

American-based Payroc LLC inked 9 deals in the period, focusing mostly on various merchant solutions and payment processors.

With 7 acquisitions, MRI Software, Global Software, and CBOE Global Markets, have also been highly acquisitive of Fintech targets.

Amidst ongoing economic uncertainties, deal targets are increasingly inclined to secure current market premiums rather than speculate on future stock rebounds.

The fintech M&A landscape in 2023 was largely driven by transactions in Payments, Crypto & Blockchain, and Banking & Lending segments.

Analysts note the hesitancy in customer adoption of payment initiation services, primarily due to a lack of awareness and understanding. Furthermore, since payment card fees burden merchants and not consumers, there’s minimal incentive for customers to change their payment methods.

A key distinction from the 2008 recession is the unprecedented level of deployable private capital, now at $3.6 trillion.

This abundance of capital incentivizes buyers and investors to pursue acquisitions, particularly when high-growth fintech companies are available at more reasonable prices.

Finally, insights from a Bain Capital survey indicate that M&A deals executed during recessions tend to yield healthy returns, a lesson gleaned post-2008. This historical perspective is crucial in strategizing current and future M&A endeavors in the fintech sector.

Top trends in Fintech

In regulatory environments, only authorized firms can access and initiate customer financial transactions. This exclusivity enables the development of innovative financial management products and services. For instance, the integration of open banking data in credit processes exemplifies efficiency, allowing lenders to conduct comprehensive affordability assessments based on diverse financial data.

The fintech sector, however, confronts challenges in public awareness and market perception, suggesting a potential uptick in M&A activities, especially in areas needing consolidation. Notably, many high-growth firms, despite being valued on revenue multiples, experienced significant valuation declines, unlike their profitable counterparts.

Data breakdown – geography and subsector

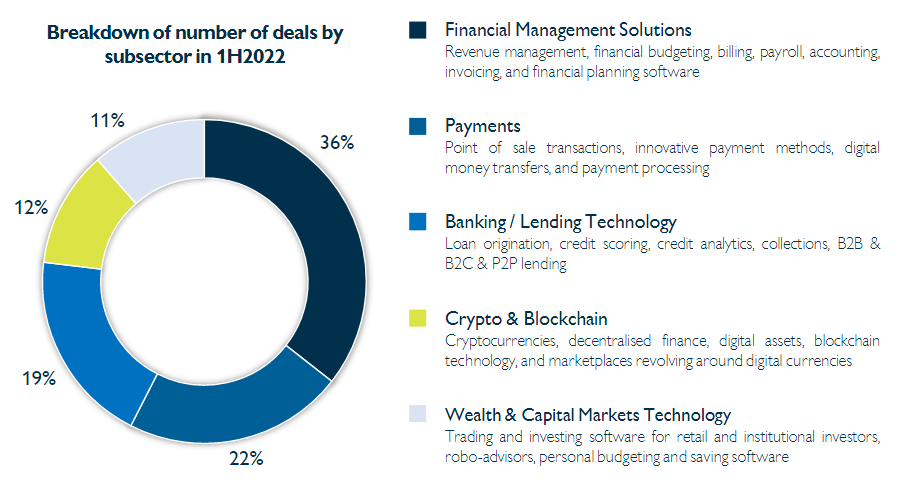

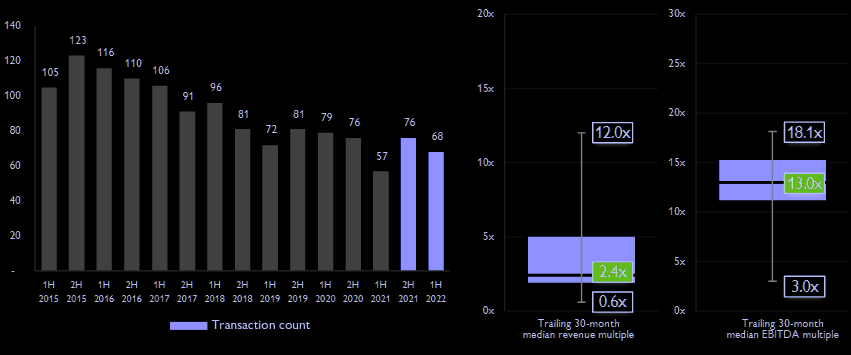

36% of all Fintech deals targeted a firm in the Financial Management Solutions segment and 22% related to Payment solutions. Interestingly, Wealth & Capital Markets Tech now only represents 11% of all deals, whereas it was the most important subsector a few years ago, accounting for one third of fintech M&A activity.

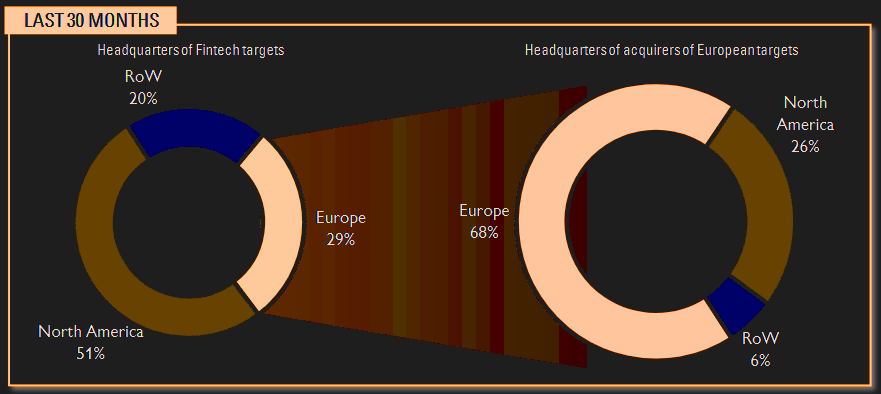

Just over 50% of all deals in the past 30 months targeted a North American firm. European targets were involved in 29% of the transactions during the same period. While over two-thirds of these were purchased by acquirers on the same continent, 32% of the European fintech sellers ended up transacting intercontinentally.

Financial Management Solutions

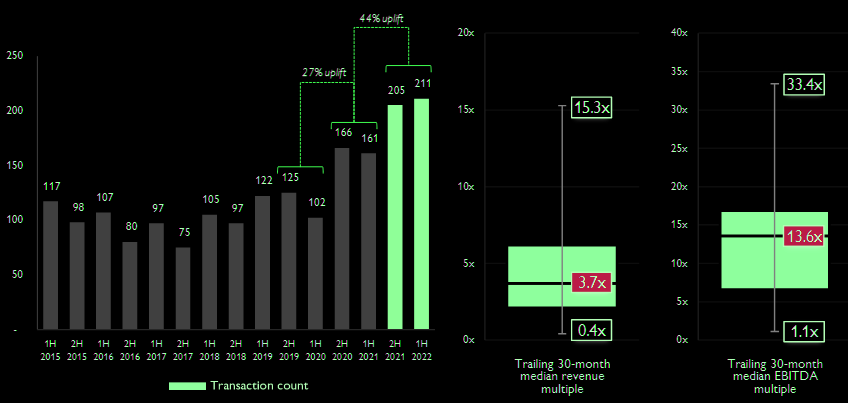

The Financial Management Solutions segment has continued to experience a surge in M&A activity, with a record 211 deals recorded and 416 in the past year. This is a 44% increase from the prior 12 months.

The trailing 30-month median revenue multiple reached a recent high of 3.7x in 1H2023 – a level unseen since 2015. Half of the disclosed transactions were valued between 2.1x and 6.3x revenue. The trailing 30-month median EBITDA multiple came in at 13.6x, with half of the disclosed transactions valued between 6.6x to 16.9x EBITDA.

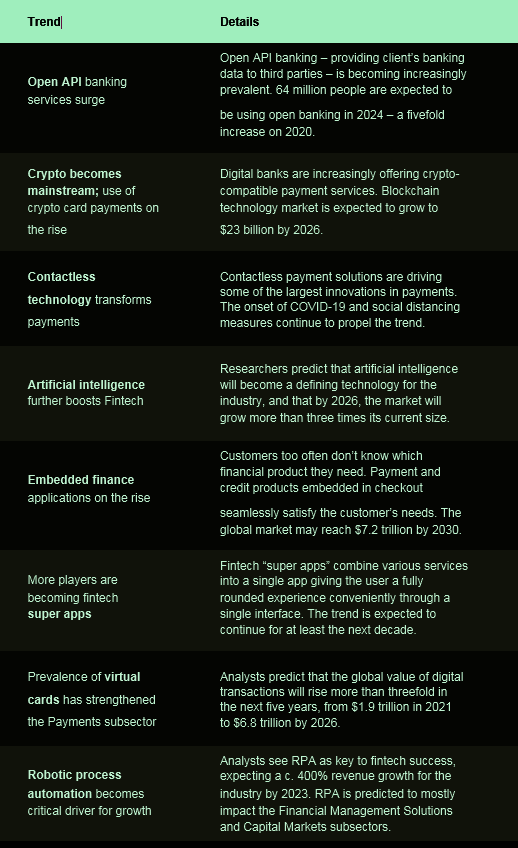

Software development companies with a focus on finance are creating software robots that mimic human actions to streamline and quicken repetitive tasks such as data entry, management of financial information, generation of financial reports, handling of insurance claims, and evaluation of business risks.

Robotic Process Automation (“RPA”) will be a key determinant of Fintech players’ success; analysts predict growing demand for RPA and 400% revenue growth in the industry by 2023.

US-based OMEGA Processing Solutions – a provider of AI and RPA-based transaction processing, payroll solutions, dashboards and analytics – was acquired by US-based Celero Commerce for an undisclosed amount. The acquisition highlights buyers’ increasing interest in targets with key RPA and financial management SaaS capabilities.

Payments

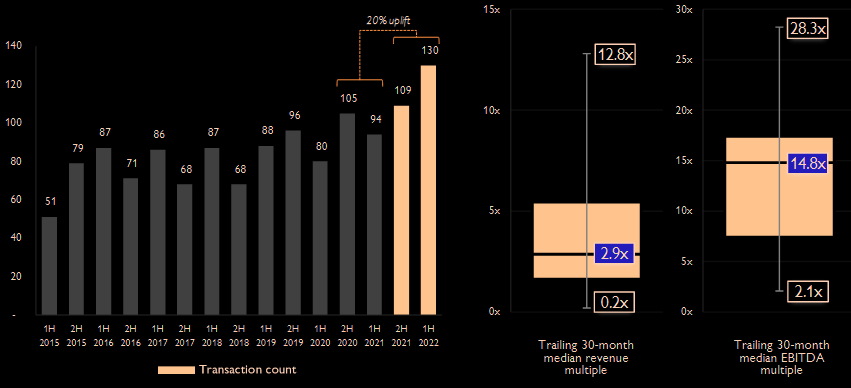

The Payments subsector has seen reasonable growth especially in the past 12 months. The number of deals in the space rose with a total of 130 deals inked, representing a 19% increase relative to the prior half-year period.

The 12-month period deal volume reached a record high of 239 deals, showing a 20% increase year-over-year. The payments category is the second largest Fintech subsector and continues to attract investor interest.

Though the market benefitted greatly from a boost at the height of Covid-19, certain players especially within the Buy Now Pay Later (“BNPL”) category have recently faced major headwinds.

These challenges are evident from its slightly depressed valuation multiples. Transactions closed at lower average revenue and EBITDA multiples in comparison to its previous 24-month average.

The trailing 30-month median revenue multiple stood at 2.9x with half of the disclosed transactions valued at a multiple between 1.6x and 5.5x. Meanwhile, the trailing 30-month median EBITDA multiple came in at 14.8x, with half of the disclosed deals showing an EBITDA multiple between 7.4x and 17.4x.

The online BNPL trend that allows users to spread payments into interest-free installments has seen huge popularity, particularly with Gen Z and millennials.

On the business side, online merchants cite BNPL as having improved customer acquisition, customer loyalty, and average order value. Across Europe, adoption has been robust: 74% of European retailers now offer the service at checkout.

Yet, criticism of BNPL mounts as more people worry it encourages young consumers to become embroiled with debt. Companies now fear that regulators may implement strict requirements limiting operations. Key players, Klarna and Affirm, recently saw their shares drop 85% and 77% respectively. Still, as the market evolves, analysts foresee growing opportunities for M&A activity as BNPL becomes mainstream.

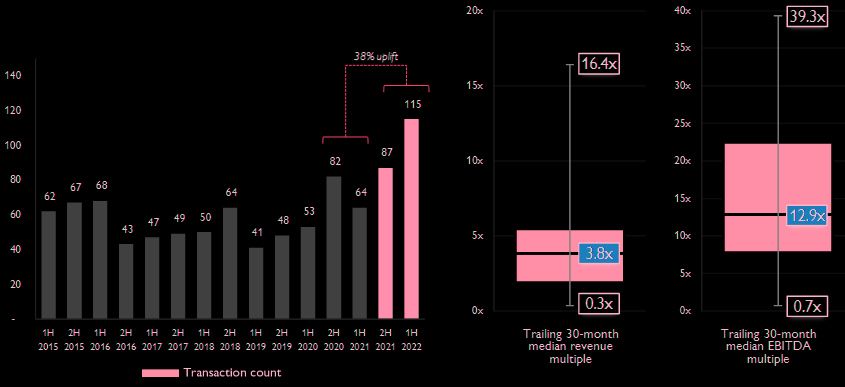

Banking & Lending Technology

The Banking / Lending Tech segment continues to attract investor attention with a strong 115 deals recorded in the space. The total number of deals recorded over the past 12 months amounted to a record of 202 transactions, indicating a 38% rise year-over-year.

The trailing 30-month median revenue multiple stood at 3.8x, with half of disclosed multiples between 1.9x and 5.5x. Meanwhile, the trailing 30-month median EBITDA multiple came in at 12.9x, with half of disclosed deals valued at an EBITDA multiple between 7.8x and 22.5x.

Yapily Limited acquired finAPI, a provider of open banking, data intelligence, KYC and payment SaaS worldwide. Yapily has focused its efforts on official API integrations covering thousands of banks. With its acquisition of finAPI, Yapily consolidates its position in Germany and Europe.

The European PSD2 regulation, effectively in force since September 2019, requires banks to offer APIs so that customer data can integrate more effectively with third-party services (under user consent). Users are beginning to realise the benefits of working with open data as smooth information exchange improves user experience and quality of financial services.

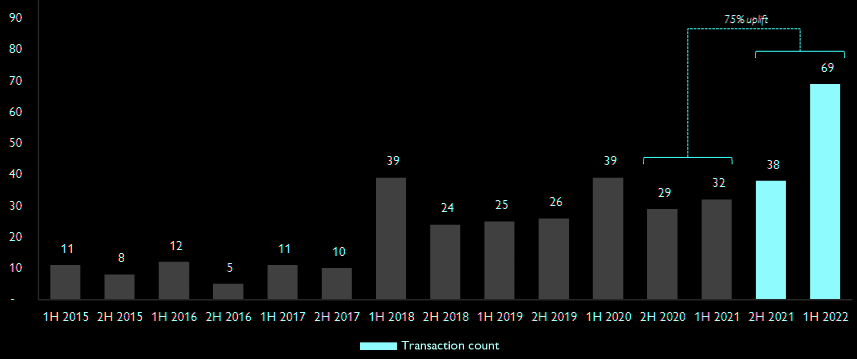

Crypto & Blockchain

The Crypto & Blockchain segment experienced a significant jump in the number of deals in the past 12 months, with a total of 107 transactions recorded, representing 75% growth year over year. In the latest period 2024, a record number of 69 transactions were logged, representing a 82% increase over the prior period.

The improved transparency offered by distributed ledger technology and growth in venture capital investments are key factors driving the growth of the market

The online realm of the metaverse now occupies the attention of companies and investors worldwide. The operation of the metaverse, however, is fully reliant on blockchain technology for recording transactions, often as part of a decentralised public database known as an encryption-secured ledger.

As blockchain technology enables monetisation in the metaverse, companies are now piling in to create a wide array of digital assets. In February, investment firm Republic Realm paid a record $4.3 million for land in Sandbox, currently the largest metaverse platform. Similarly, technology enterprises are expanding their online platforms allowing people to work, play, and socialise.

US-based Descrypto Holdings acquired OpenLocker, a provider of an online NFT trading portal and marketplace for $11 million.

OpenLocker enables the sale and trading of racing prospect collections. The transaction is the latest in a string of investment activity within the cryptocurrency space as the metaverse becomes monetisable and the popularity of NFTs increasingly propel the adoption of crypto.

Wealth and Capital Markets Technology

The trailing 30-month median revenue multiple stood tech subsector has remained relatively stable since at 2.4x, with half of all disclosed deals valued between 2020 but has seen a gradual slowdown in recent years 1.8x to 5.1x.

The trailing 30-month median EBITDA the segment saw 68 transactions, and a multiple was 13x, with half of all disclosed deals total of 144 transactions over the latest 12-month period valued between 11.1x to 15.4x.

With covid came a surge in retail investment activity: the emerging investor class propelled trading platform revenues from $4 billion in 2017 to $11 billion in 2020. This growth has shown no sign of stopping.

Consumer-focused trading platforms have become less costly, and more user friendly, but also because:

- Fractional investing features allow investors to seamlessly purchase even fractions of shares

- AI-based investment recommendations by robo-advisors help amateur investors make decisions

- Access to a variety of ESG, value-based, and sector-specific funds allow investing that matches perfectly with an investor’s preferences

Robust global M&A expected to slow

Inflation rates rise and a recession looms

Inflation rates have risen to 40-year highs in countries across North America and Europe amid mounting fears of an impending recession. While economists do not foresee a recession striking in 2023, persistently high inflation and increasing interest rates may substantially dampen consumer spending in the new year, making a recession increasingly likely in 2024.

Gloomy outlook unlikely to stifle M&A activity “in the near term”

The expected impact of the current economic climate on M&A is counterintuitive. Although worries of a possible recession has escalated, appetite for deal making has hardly disappeared according to an elaborate survey conducted by KPMG. In fact, quite the opposite.

80% of executives signaled their appetite for deals is stronger. 61% indicated they expect M&A activity in their sector to increase over the next 12 months.

Despite the highly unstable market, the fundamental drivers of M&A remain in place. Companies use M&A to remain competitive, expand, acquire new capabilities, enter new markets, and dispose certain assets to cut costs and sharpen their focus. Such operational initiatives remain as vital, if not more, during recessionary periods. Indeed, if a recession does occur, economists foresee a decline of deal activity.

Currently though, companies have been using M&A to prepare themselves for a transformed economic atmosphere. They intend to acquire competitive capabilities through acquisitions before interest rates rise even further and dispose of non-core assets to cut unnecessary costs before the economy considerably declines.

A more encouraging outlook for tech M&A

Buyers’ strong appetite for technology acquisitions has remained strong in 1H2022. As competitive pressures increase in a battle for market share, the ever-growing need for digital transformation and technological advancements has fueled M&A activity. Covid-19 intensified such competitive pressures in the sector and a looming recession has enticed technology companies to act quickly.

Technology businesses such as software and internet companies can scale easily, allowing them to quickly reap the benefits from M&A activity (e.g., realising improved customer reach, product breadth, and enhanced data). Analysts expect a robust level of technology M&A activity to continue and potentially accelerate in the near term.

M&A relating to financial management, payments, banking, lending, crypto, defi, digital assets, trading and investing, broadly categorised as Fintech, has maintained its record levels of activity and high valuations during these uncertain times.

Despite record inflation, supply chain and geo-political risk, and concerns of a recession – or perhaps precisely because of these factors – deal-making in Fintech has been particularly robust thus far: we tracked nearly 600 acquisitions – the highest volume for a six-month period on record.

Many Fintech companies raised significant investment capital recently. Some will grow and mature to serial acquirers in their niches. Many other Fintechs will be sellers in what continues to be an attractive M&A market.

Analysts foresee a continued rise in related M&A as increasing numbers of private Fintech companies run out of money needed to fuel and maintain their operations.

Their options will be to

- raise capital from venture capital firms (although VCs have become increasingly selective amid heightened uncertainties);

- sell to private equity or strategic acquirers;

- entirely shut down business operations.

These options make a sale appear attractive.

At the same time, public companies with massive capital and PE with large amounts of dry powder, well financed late-stage high-growth private companies, and traditional financial services companies who look to remain relevant, are on the lookout for good assets in the sector.

FAQ

The Fintech sector has experienced a sharp increase in M&A deals, driven by the need for consolidation, strategic partnerships, and access to capital. Economic pressures and lower valuations have made many fintech companies attractive acquisition targets.

Many fintech companies went public at high valuations, which later declined due to market corrections. Investors shifted their focus to profitable companies, resulting in valuation cuts for high-growth, unprofitable fintech firms.

M&A activity is high in Payments, Crypto & Blockchain, and Banking & Lending segments. Emerging sectors like open banking, paytech, regtech, and green finance are also drawing significant interest.

With persistent economic uncertainty, many fintech companies are seeking M&A as a growth strategy, particularly those struggling to raise capital. Sellers are inclined to secure current market premiums rather than wait for stock price rebounds.

Private equity firms remain highly active in the fintech M&A market, representing a stable share of deals. As VCs become more selective, PE firms with available capital are targeting high-growth fintech companies at reduced valuations.

Only authorized companies can access financial data or process transactions on behalf of customers. This exclusivity drives M&A as fintech firms seek partnerships with regulated companies to expand their service offerings.

While global M&A may slow, analysts believe fintech M&A will remain resilient due to high levels of private capital. The lessons from 2008 show that M&A deals executed during economic downturns can deliver strong returns.

…………………….

AUTHOR: Miro Parizek – Principal Partner Hampleton, Fact-checked by Oleg Parashchak – Editor-in-Chief Beinsure Media, CEO Finance Media Holding.