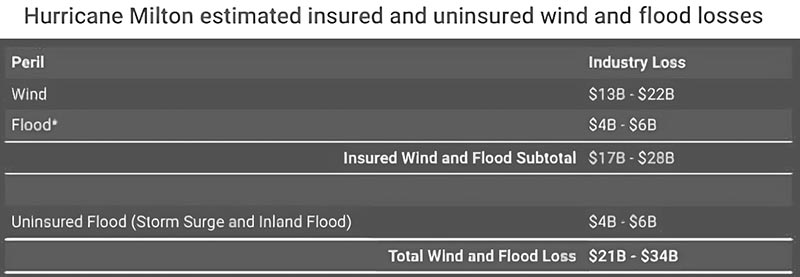

Most of the losses, approximately $13 bn to $22 bn, stem from wind damage, which accounts for the bulk of privately insured losses.

Coastal flooding will impact areas like Sarasota, Naples, and Ft. Meyers, while precipitation-driven inland floods are likely to affect Tampa Bay. Combined flood losses are expected to contribute $4 bn to $6 bn to the total insured losses.

These estimates include damage to residential, commercial, and industrial properties, covering building contents and business interruptions. Flood losses account for storm surge and inland flooding but exclude offshore properties like marine cargo, personal boats, and inland marine.

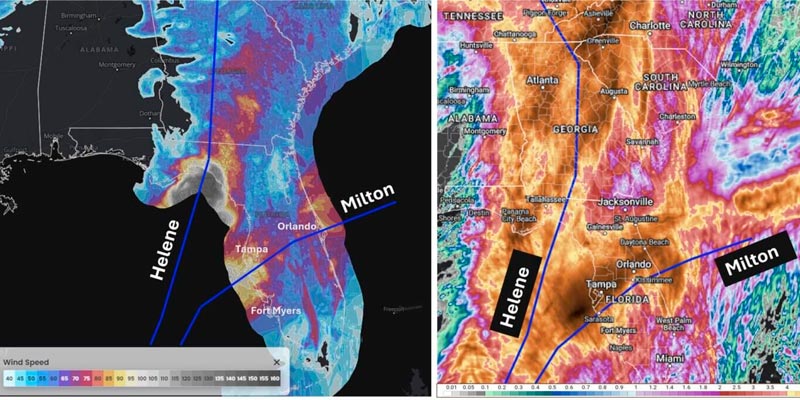

Hurricane Milton forecasts currently indicate a direct landfall over Tampa Bay as a Category 3 hurricane with maximum sustained winds of 125 mph

Jon Schneyer, director of catastrophe response at CoreLogic

“Small changes in the exact landfall location will have monumental consequences on the financial impact of this storm. A direct landfall, or one just north of Tampa Bay, would be a worst-case scenario because the winds and storm surge flooding would be most intense. A more southern landfall would reduce the impact in Tampa Bay but devastate communities along the coast near Sarasota,” said Jon Schneyer.

Hurricane Milton At-Risk Single Family and Multi-Family Homes and Reconstruction Cost Values

| Saffir Simpson Category | Tampa Metro Area | Sarasota Metro Area |

| Cat. 1 | 161,871 | 63,599 |

| Cat. 2 | 250,787 | 101,682 |

| Cat. 3 | 341,396 | 159,961 |

| Cat. 4 | 448,013 | 254,218 |

| Cat. 5 | 541,223 | 301,206 |

| Saffir Simpson Category | Tampa Metro Area (Millions) | Sarasota Metro Area (Millions) |

| Cat. 1 | $38,966.7 | $16,457.2 |

| Cat. 2 | $60,340.9 | $26,011.4 |

| Cat. 3 | $82,830.6 | $40,604.4 |

| Cat. 4 | $109,522.3 | $64,622.8 |

| Cat. 5 | $133,010.2 | $77,173.9 |

The table above indicates the total number of homes with exposure to storm surge damage given the current path of the storm. RCV figures represent the cost to completely rebuild homes in these areas, which CoreLogic estimates using detailed property characteristic data of each unique home combined with current localized costs of materials, equipment and labor.

The calculation does not include the value of the land or lot. The RCV figures assume 100% destruction of all at-risk homes and are not a representation of expected damages.

The insured flood losses come from both private markets and the National Flood Insurance Program (NFIP). Damage from tornadoes associated with the storm is not part of this estimate.

Dr. Daniel Betten, Director of Forensic Meteorology at CoreLogic, noted that Hurricane Milton presented unusual conditions. As the storm neared Florida, it interacted with the jet stream, resulting in stronger-than-expected winds on the northern and northwestern sides. This created two distinct corridors of damaging winds, particularly affecting Sarasota, south of Milton’s landfall point.

CoreLogic’s event response team, based in Central Florida, assessed the damage across the Gulf and Atlantic Coasts. Tom Larsen, CoreLogic’s Associate VP of Hazard & Risk Management, reported that despite the potential for large losses in Tampa Bay, the observed wind damage was less severe than expected, with minimal storm surge impact in major population centers.

In Orlando, the team observed localized damage, such as downed trees and damaged signs, but no significant destruction. Flooding, while severe in specific areas like Siesta Key, where landfall occurred, contributed less to the overall insured loss compared to wind. Maximum rainfall in Tampa Bay measured 19 inches in 24 hours, with widespread totals between 10 and 15 inches.

The overlap between Hurricane Milton and the earlier Hurricane Helene presents challenges for damage attribution, especially in regions like Tampa Bay, where both storms brought wind and storm surge damage.

This overlap could lead to complications in assigning losses to specific storm policies.

Methodology

CoreLogic offers high-resolution location information solutions with a view of hazard and vulnerability consistent with the latest science for more realistic risk differentiatio

The high-resolution storm surge modeling using 10m digital elevation model (DEM) and parcel-based geocoding precision from PxPoint™ facilitates this realistic view of risk.

Single-family residential structures less than four stories, including mobile homes, duplexes, manufactured homes and cabins (among other non-traditional home types) are included in this analysis. Multifamily residences are also included. This is not an indication that there will be no damage to other types of structures, as there may be associated wind or debris damage and are not tabulated in this release.

by Yana Keller