Overview

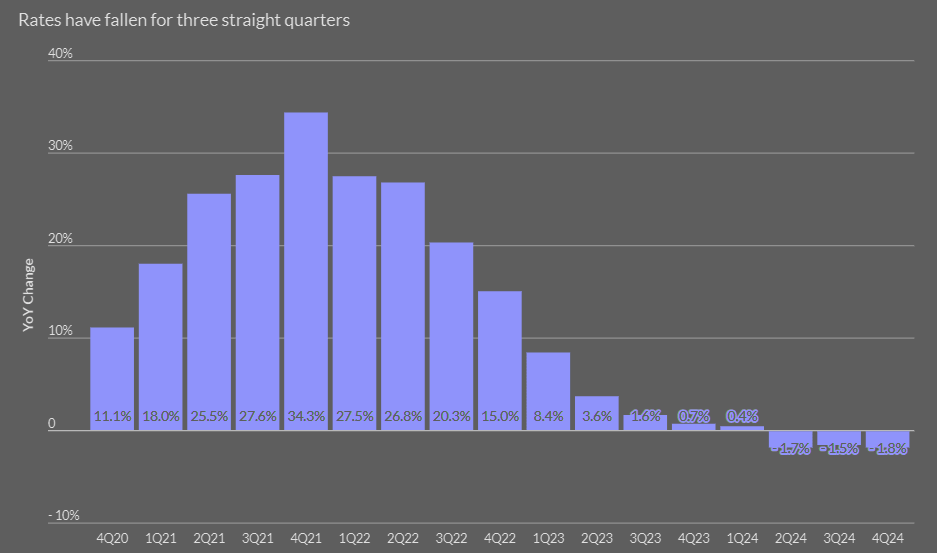

U.S. cyber insurance renewal premium rates have declined year over year for the past three quarters and are expected to remain under pressure in the short term unless a major event occurs, according to Fitch Ratings report.

Although the cyber insurance sector recorded profitability in 2024, direct written premiums decreased for the second consecutive year due to lower rates and a reduced number of active policies.

Insurers face persistent challenges in maintaining underwriting discipline amid increasing market competition, according to Global Cyber Insurance Industry. They must also adjust to a shifting claims environment that is shaped more by technological developments, including artificial intelligence, than by regulatory changes or case law, Beinsure noted.

Declining Premium Rates and Market Profitability

The cyber insurance market is expected to encounter periods of volatility as it adjusts in areas such as coverage limits, terms and conditions, regulatory frameworks, legal considerations, and cyber threats that could result in claims, Fitch notes.

Corporate executives continue to express concern about cyber risks, which is likely to support demand for cyber coverage.

However, the adoption of cyber insurance varies widely across industry sectors and company sizes. Larger companies with more complex operations tend to maintain some level of cyber insurance, while smaller firms with lower revenues are less likely to have coverage or hold policies with lower protection levels.

P&C Cyber Insurance Direct Written Premiums

Cyber insurance is a complex product that demands specialized knowledge and expertise. Despite these challenges, it also presents opportunities for profitable expansion and innovation within the insurance sector, according to AM Best.

Demand Trends and Data Limitations

Available statutory cyber financial data does not offer a complete assessment of segment profitability, as direct results exclude underwriting and adjustment expenses. Additionally, the data does not reflect the impact of ceded reinsurance on premiums and losses, Beinsure noted.

Cyber insurance is a line where primary carriers typically purchase significant reinsurance protection.

New cyber insurance capacity is increasingly matching fast-growing demand, particularly within the United States, and greater competition is said to be leading to decreasing retention levels, as well as lower costs for coverage.

Cyber Insurance Quarterly Change in Renewal Rates

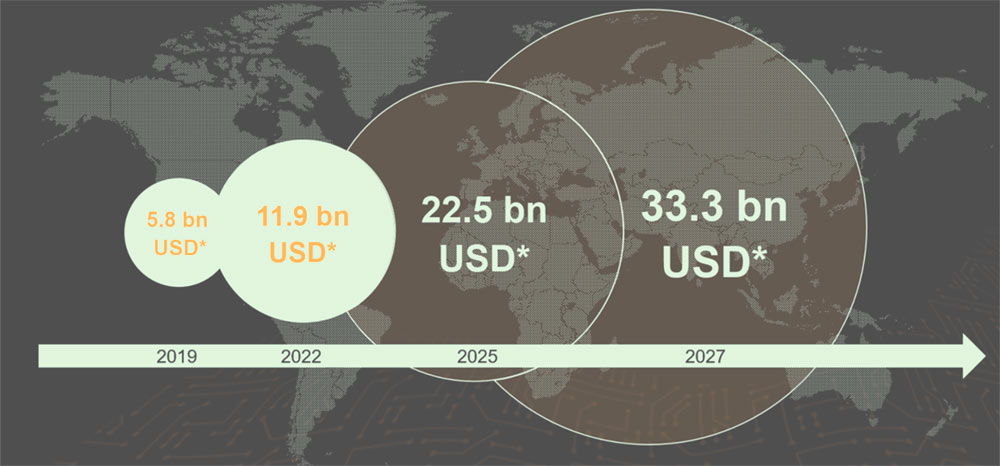

According to S&P report, cyber insurance remains one of the fastest-growing areas within the global insurance industry, with premiums anticipated to exceed $20 bn by 2025

Global cyber insurance market has further matured. Cyber risk continues to increase, driven by rapid technological advances such as generative artificial intelligence or cloud technology, Beinsure noted.

Global cyber insurance market outlook

Global industries are increasingly dependent on IT, Internet of Things, Operational Technology and digital services, such as cloud computing, each of which represent a critical part of the supply chain for many risk owners.

ILS Market Growth, Catastrophe Risk, and Regulatory Updates

The cyber insurance-linked securities (ILS) market has expanded significantly and is projected to remain a source of market growth.

However, it faces notable challenges in risk modeling, which limit broader participation from investors.

The 144a ILS market is valued at approximately $51 bn, with cyber insurance accounting for about 2% of that total (see How ILS Can Support Additional Re/Insurance Capacity for Cyber Risk).

Catastrophe exposure related to cyber risks continues to present substantial uncertainty concerning the nature, probability, and cost of the most severe cyber incidents.

Insurers and risk modeling firms allocate significant resources to assess risk aggregation and estimate probable maximum losses from large-scale cyber events.

Cyber Risk Models Lag Behind Natural Catastrophe Modeling

However, cyber risk models remain less developed than those for natural catastrophes, which have benefited from decades of refinement.

Recent changes were made to the filing requirements for the statutory supplement on U.S. cyber insurance, Beinsure noted.

Premiums are now categorized into three groups: primary, excess, and endorsement, replacing the earlier two categories of standalone and package. Despite the new categorization, the overall totals remain comparable.

Further analysis of segment results and company market shares will be provided in Fitch’s detailed report on the U.S. cyber insurance market, scheduled for release in early summer.

According to Cyber Insurance Market Dynamics Report, economic vitality, business continuity, and successful digitalization rely on cyber coverage – and a sustainable cyber insurance market demands transparency.

Future cyberattacks will be increasingly accelerated by key technology trends such as artificial intelligence like ChatGPT, the so-called “metaverse” and the expanding worlds of IT, Internet of Things and operational technology.

All these converging technologies offer great opportunities for society, businesses and governments, though new attack surfaces, vulnerabilities and systemic risks will continue to emerge at the same time.

FAQ

Premium rates have fallen year over year for the past three quarters due to increased market competition, lower rates, and fewer policies in force.

Yes, the sector remained profitable in 2024, although direct written premiums decreased for the second consecutive year.

Insurers face intensified competition and must adapt to a claims environment driven more by technological advancements, such as artificial intelligence, than by regulations or case law.

Larger companies with more complex operations are more likely to hold cyber insurance policies. Smaller firms typically have lower adoption rates or reduced coverage levels.

Statutory financial data does not fully capture profitability, as it excludes underwriting and adjustment expenses and does not reflect the impact of ceded reinsurance.

The 144a ILS market totals approximately $51 bn, with cyber insurance representing around 2% of this figure.

Cyber risk models remain less developed than natural catastrophe models, which have undergone several decades of refinement. Carriers and modeling firms continue to invest resources to improve cyber risk assessments.

……………….

AUTHORS: Gerry Glombicki, CPA, CISSP, CCSP, CISA, ARM – Senior Director, North American Insurance at Fitch Ratings, Laura Kaster, CFA – Senior Director, Risk for North and South American Financial Institutions, Credit Commentary & Research at Fitch Ratings, Tana Marcom – Senior Director, North American Insurance at Fitch Ratings