Overview

London Insurance Market have historically competed on expertise and not technology. The route to success was seen to be hiring the best underwriters, in the right numbers.

According PWC`s Report: “Transforming the London Market”, systems and tools were a secondary consideration. Other issues hampered change: it was perceived to be difficult to make the business case for investment; there was a degree of complacency around long-term profitability; and class-specific tactical solutions were deemed satisfactory. Coupled with much of the market’s infrastructure being provided centrally, insurers have struggled.

We now see the landscape changing: the hard market is one catalyst, alongside general perceptions that others are making investments, and that modern, modular tools are quicker, easier and less risky to deploy.

The next generation of underwriters are also more open to new tools and new ways of working. For the first time in decades we are seeing significant investments in the technology used in the underwriting journey, from prospecting to post-bind activities.

In response, PWC asked senior management of London Market insurers their opinions on the drivers, opportunities and risks of these technology investments.

Survey revealed some unique insights into delivering successful transformation and getting the best return on investment.

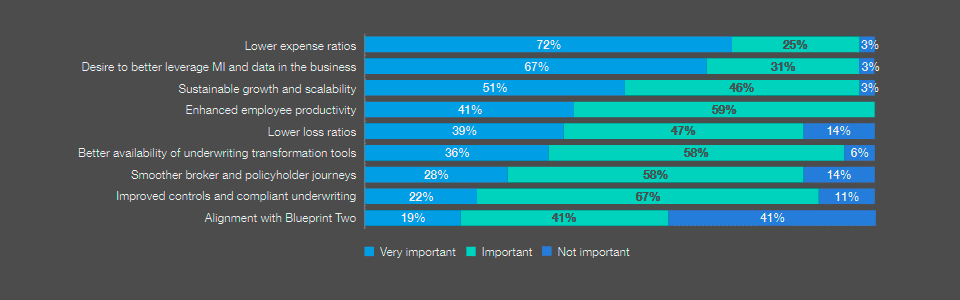

Digital Transformation drivers: insurers’ ambitions for change

London Market insurers are trying to solve a wide range of problems simultaneously: better equip underwriters with the tools and insight they need; lower costs and drive productivity; improve controls and better serve clients and brokers.

London Market insurers have an expense problem, collectively and individually. Unsurprisingly, the survey finds addressing this a top driver.

Building a business case around expense reduction often seems easy, but long-term success requires careful management and tracking of benefit delivery and implementation milestones.

Being clear on programme objectives, and how they link to individual investments, is vital. All too often, benefit delivery is decoupled from technology investment. Technology change should not become a goal in itself.

Technology investments must also be accompanied by tangible change to working practices and target operating models. It is easy to make assumptions about the benefits new tools can bring, but without the right processes and adoption, the benefits of the change often fail to materialise.

Underwriters spend far too little time underwriting. Addressing this not only drives productivity, but also helps firms attract and retain talent. Those with modern tooling and efficient processes have more engaged underwriters and better retention.

Andy Moore, PwC UK, Partner

The survey identified two priorities, and related, areas for investment: underwriting workbenches, and portfolio management tools.

What are the most important drivers for your technology transformation?

Underwriting workbenches are workflow, productivity enhancement, and decision support tools, giving underwriters easy access, in one central location, to everything they need to fulfill their role. New low-code platforms offer cost-effective and fast deployment, allowing underwriters to see benefits quickly. Increasingly they are surfacing portfolio management data alongside case underwriting information.

Historically, insurers have not had the capacity to capture every submission – with an automated process it is possible to capture granular information about every submission (even those not taken up or declined).

This opens up opportunities for insightful MI on portfolio management (e.g. historical claims on declined business).

The majority of firms have already started to move away from spreadsheets in accordance with regulatory best practice. But many are still on the journey and are now ‘half-on, half-off’, leaving the more complex, or smaller, classes to last.

Initiatives and tooling

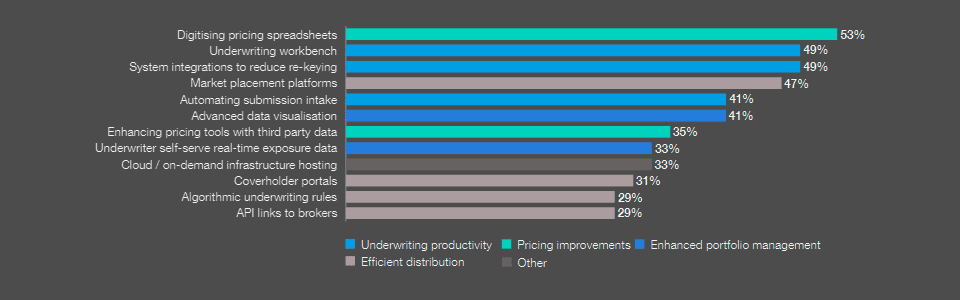

Insurers are showing ambition in the breadth of the technology change they are committed to implementing: a third are investing in more than four tools simultaneously. On the next page we offer our perspective on some areas to focus on to get the best value from investments.

In which of the below is your company actively investing in the next 12 months?

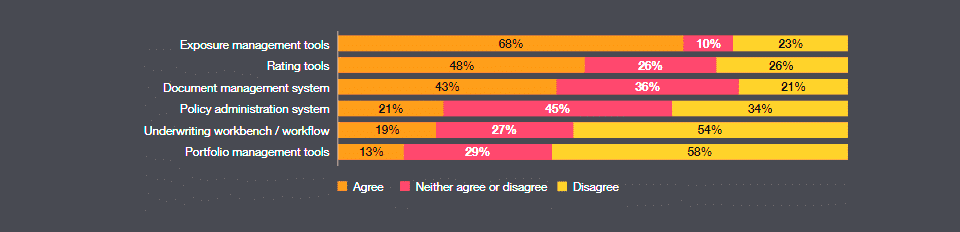

To what extent do you agree your current tools are fit for purpose?

Insurers are on a spectrum when assessing and implementing workbenches.

Large multinational insurers have often already invested in this space, using workbenches to measure and drive underwriting productivity across classes and geographies.

Some Lloyd’s carriers are currently selecting tools and defining their requirements, where others see the potential benefits but lack the data architecture to surface the information.

Insurers have a multitude of overlapping legacy systems, with substantial dual-keying across the estate.

For many years, insurers focused on reducing this expense through near- or off-shoring, but this opportunity has been exhausted. The next step is to eliminate re-keying at the source.

IT estates are being modernised piece by piece. As insurers invest in new tools, they find themselves trying to integrate modern cloud-native API-enabled tools with legacy infrastructure.

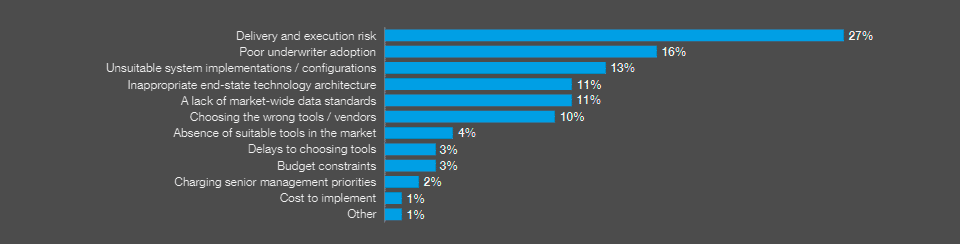

Risks and dependencies

Deploying new technology can be fraught with risk: many insurers spend a lot of money but fail to deliver on business cases. Below we highlight some key risks from the survey, alongside actions you can take to mitigate those risks and improve your chances of success.

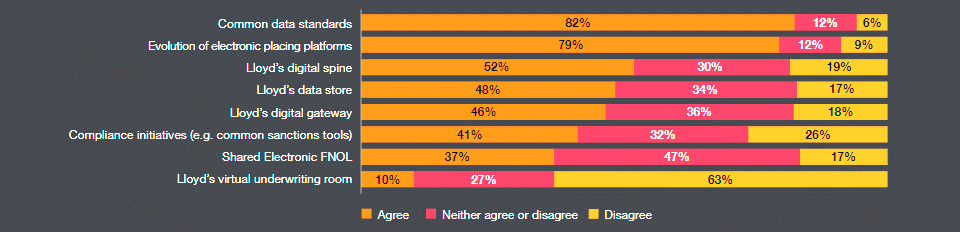

What do you think are the biggest risks to the success of your technology transformation?

Do you agree your transformation is dependent on the success of these market-wide efforts?

The drive to adopt market placement platforms has been accelerated by a shift to hybrid working. It’s clear that there are significant benefits from adopting these platforms. Underwriters are significantly more productive when they place business through, for example, PPL or Whitespace. But to reach their potential a lot of development is still required (e.g. API integration).

Everyone loses unless the market moves together towards common data standards. London’s continued success as a global insurance hub depends on successful digital transformation.

Andy Moore, PwC UK, Partner

Underwriters and portfolio managers have been poorly served with data. Analysis to support portfolio management and business planning has been created on an ad-hoc basis, through various spreadsheets.

Modern data visualisation tools offer a relatively inexpensive and easy way to aggregate and interrogate data, presenting it in meaningful ways to aid decision making and control.

6 key actions a technology deployment programme for insurers

- Confirm your business strategy is informing your technology transformation. To future-proof your plans, you need to make explicit assumptions about how your business will change. For example, making assumptions about digital distribution and the need for API integration with brokers and other intermediaries.

- Set clear and realistic objectives aligned to the business case for your transformation. Be explicit about what you are trying to achieve, and what defines success. The objectives must be instilled in day-to-day programme activity, otherwise development can easily go in the wrong direction.

- Set an end-state technology design for your business. This can be flexible, but you need a picture of which applications will support which business activities. Don’t work backwards (i.e. procure the technology and then work out what to do with it). Start with the business requirements and then decide how technology can best meet them.

- Align technology investment with any cultural change programme and hybrid working efforts. Many such programmes fail because users do not use new tools in the way they were intended.

- The biggest gains are made by combining new technology with improved and standardised business processes. Some aspects of specialty underwriting will forever remain class specific, but much activity is performed differently class-by-class because of historical practice, not real business need. Harmonising activity across classes creates a ripple effect of efficiency gains throughout the quote to post-bind process.

- The adoption of Common Data Standards, starting with the Common Data Record (CDR) is vital to the transformation of the market as a whole. Play your part in driving these new ways of working: in some ways we are all in this together, dependent on each others’ adoption and approach.

FAQ

Workbenches are digital tools used by insurers to measure and enhance underwriting productivity across various classes and geographies. Large multinational insurers have already invested in these systems, leveraging them to streamline operations and improve efficiency.

Insurers often operate with overlapping legacy systems, leading to inefficiencies like dual-keying. While initial solutions focused on off-shoring, the next step is eliminating re-keying at the source. Modernizing IT systems is a gradual process as insurers integrate new cloud-native tools with existing infrastructure.

Key risks include failing to deliver on business cases, overspending, and encountering integration challenges with legacy systems. To mitigate these risks, insurers should ensure their business strategy drives their technology transformation and set clear objectives tied to measurable outcomes.

Hybrid working has accelerated the shift to market placement platforms like PPL and Whitespace. These platforms significantly improve underwriter productivity by streamlining business placement, though further development, such as API integration, is needed to maximize their potential.

Common Data Standards, like the Common Data Record (CDR), are essential for enabling seamless integration across the insurance market. They ensure consistency and collaboration, which are vital for London’s continued success as a global insurance hub.

Insurers must ensure that technology investment aligns with cultural change programs and hybrid working initiatives. Successful adoption requires aligning user behavior with new tools and standardizing business processes to maximize efficiency.

Modern data visualization tools provide a cost-effective way to aggregate and analyze data. They allow underwriters and portfolio managers to make informed decisions and improve business planning by presenting data in meaningful and actionable ways.

…………………..

AUTHORS: Andy Moore – PwC UK Insurance Partner, Lloyd’s and London Market Leader, Michael Cook, Dip CII, Partner at PwC UK – Claims Advisory and London Market Consulting Lead