Overview

With global temperatures 1.54°C above the pre-industrial average, 2024 is on track to become the hottest year recorded. A warming climate has intensified natural catastrophes, especially in Europe, which faced severe flooding. These events resulted in the second-highest flood-related insured losses in the region’s history, as per Swiss Re Institute. Beinsure reviewed the report and highlighted the key points.

- Estimated insured losses from natural catastrophes on track to exceed $135 bn in 2024

- Hurricane Helene and Hurricane Milton severely impacted the US, resulting in estimated insured losses approaching $50 bn

- Major floods hit Europe and the Middle East, causing estimated insured losses of close to $13 bn as of today

In the US, two major hurricanes and frequent severe thunderstorms contributed to over $135 bn in estimated global insured losses for 2024, with the US accounting for at least two-thirds of these losses.

Hurricane Helene’s recent destruction underscores the rising flood risk impacting local economies and tax bases in the Eastern and Southern United States, according to Moody’s Ratings. Analysts warn that both coastal and inland flooding events are becoming more frequent and severe, escalating credit challenges such as rising insurance costs, declining property values, and increased demands for climate adaptation investments.

Global Flood Risk Intensifies

In 2024, severe floods in Europe and the UAE resulted in estimated insured losses of close to $13 bn to date. It was the third-costliest year for this peril globally and the second costliest for Europe which experienced insured losses of approximately $10 bn, according to Swiss Re Institute’s estimates.

Floods can happen anywhere — just one inch of floodwater can cause up to $25,000 in damage. Most homeowners insurance does not cover flood damage.

Flood risk insurance is a separate policy that can cover both buildings and contents.

The devastation wrought by Hurricane Helene across a 500-mile swath of the U.S. Southeast, including Florida, Georgia, the Carolinas, Virginia, and Tennessee, is just the latest example in recent years of the growing vulnerability of inland areas to flooding from both tropical storms and severe convective storms.

Intense precipitation in April caused floods in the Gulf region, disrupting the operations of the world’s busiest airport of Dubai.

In September, Storm Boris caused major floods in Central Europe, mainly affecting the Czech Republic, Poland and Austria. Additional impacts were reported from Slovakia, Romania, Italy and Croatia.

While so-called Vb lows – slow-moving, low-pressure systems – are nothing unusual in the region, the strong intensity of the Vb system connected to Storm Boris is favoured by conditions related to climate change.

Storm Boris mixed cold Arctic air flowing southwards with unusually warm air from the east and south, drawing moisture from a record-breaking warm Mediterranean Sea.

In October, large parts of Spain experienced heavy rainfall, flash floods and hailstorms, which caused severe damage. The floods were worst in eastern and southern Spain, with most of the damage across the Valencia and Castilla-La Mancha regions.

Andalusia and the Balearic Islands were also affected. One year’s average precipitation was dumped in less than eight hours in many locations. Steep clay terrain and drainage systems could not absorb the exceptional amount of water, leading to fast overflows.

Pluvial and Fluvial Floods in Urban Areas

Fluvial floods occur near rivers, building gradually or rapidly after heavy rains. Pluvial floods, however, can strike any area, especially urban ones, where sealed surfaces prevent water absorption and overwhelm drainage systems.

Coastal areas face additional risks from storm surge floods, often linked to tropical cyclones. Flooding also emerges as a secondary impact of major weather events like hurricanes.

Economic development continues to be the main driver of the rise in insured losses resulting from floods, but also other perils, seen over many decades.

Jérôme Jean Haegeli, Swiss Re’s Group Chief Economist

However, with natural catastrophe risks rising and higher price levels, the annual increase of 5–7% in insured losses will continue, and protection gaps could remain high. This highlights the need for adaptation in combination with an adequate insurance coverage that can support financial resilience.

Losses are likely to increase as climate change intensifies extreme weather events while asset values increase in high-risk areas due to urban sprawl. Adaptation is therefore key, and protective measures, such as dykes, dams and flood gates, are up toten times more cost-effective than rebuilding.

Rising Insured Losses Linked to Climate Change

Swiss Re’s Group Chief Economist, Jérôme Jean Haegeli, highlights the dual drivers of increasing losses: economic development and escalating natural catastrophe risks.

Insured losses are growing at an annual rate of 5–7%, with protection gaps remaining high. Urban expansion into high-risk zones and asset value growth exacerbate these losses.

Adaptation measures such as dykes, dams, and flood gates offer cost-effective solutions, often ten times cheaper than rebuilding after disasters.

Estimated total economic and insured losses

| 2024 | 2023 | Annual change | Previous 10-y average | |

| Economic losses (total) | 320 | 302 | 6% | 254 |

| Nat cat | 310 | 291 | 6% | 241 |

| Man-made | 10 | 11 | –8% | 13 |

| Insured losses (total) | 144 | 125 | 16% | 108 |

| Nat cat | 135 | 115 | 17% | 98 |

| Man-made | 9 | 10 | –7% | 10 |

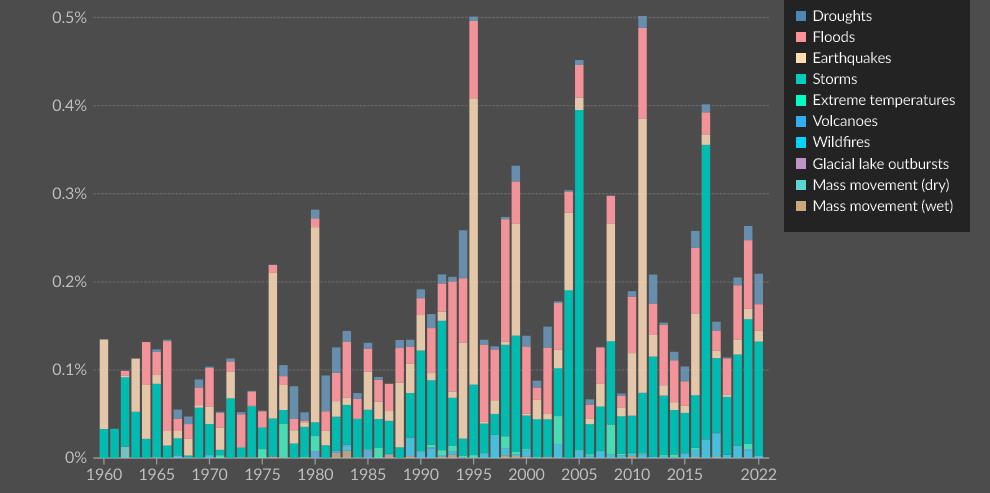

Economic damages from disasters as a share of GDP, World

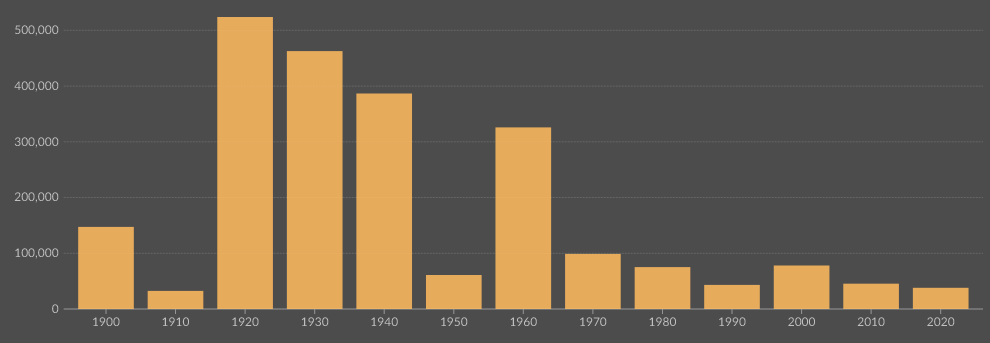

Annual number of deaths from disasters, World

Hurricanes and Thunderstorms Dominate US Losses

The US bore the brunt of insured losses in 2024, driven by hurricanes and severe thunderstorms. Hurricane Helene struck Florida on 27 September, followed by Hurricane Milton on 9 October, with combined insured losses estimated at under $50 bn.

Severe thunderstorms added over $51 bn globally in insured losses, making 2024 the second-costliest year for this peril after 2023’s $70 bn record.

Balz Grollimund, Swiss Re’s Head of Catastrophe Perils, stressed the ongoing burden of insured losses surpassing $100 bn annually for the fifth consecutive year. Contributing factors include urban value concentration, economic growth, and rising rebuilding costs.

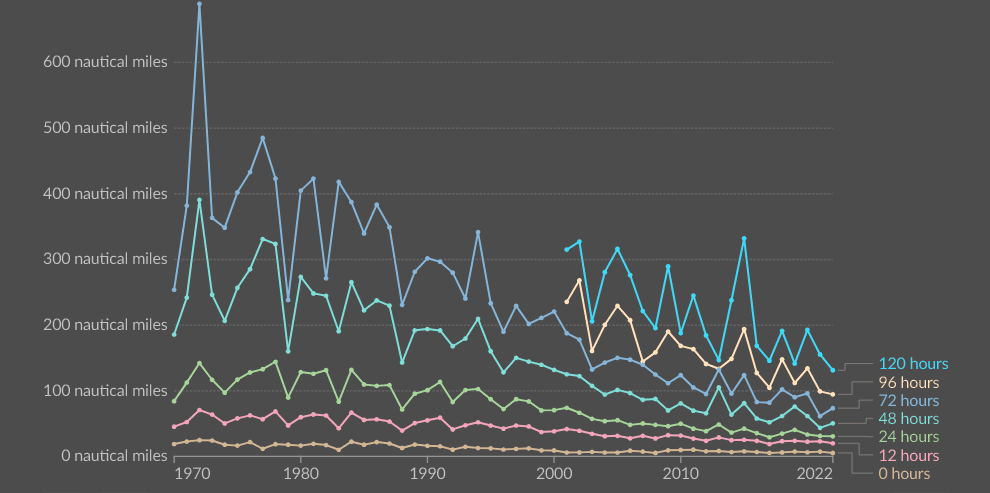

Atlantic hurricane and tropical cyclone track error

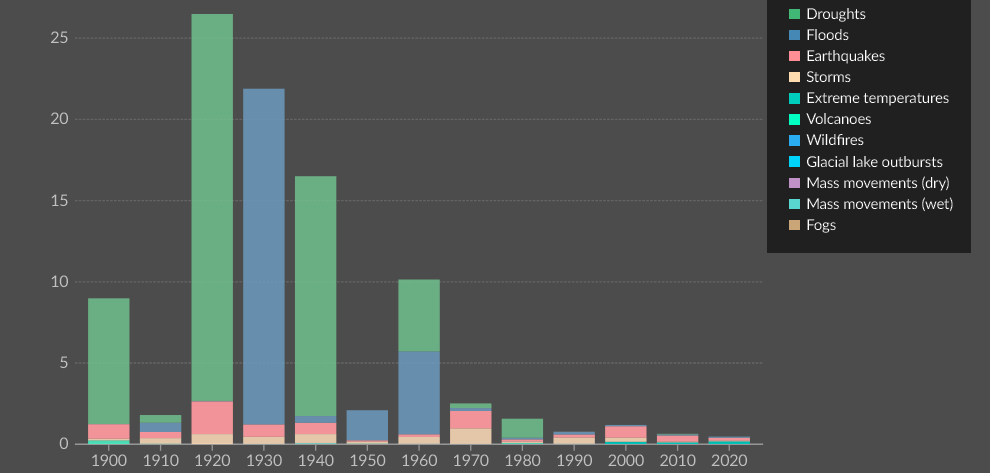

Death rates are measured as the number of deaths per 100,000 people

Source: EM-DAT, CRED / UCLouvain

For the fifth consecutive year, insured losses from natural catastrophes break the USD-100-billion mark. Much of this increasing loss burden results from value concentration in urban areas, economic growth, and increasing rebuilding costs.

Balz Grollimund, Swiss Re’s Head Catastrophe Perils

By favouring the conditions leading to many of this year’s catastrophes, climate change is also playing an increasing role. This is why investing in mitigation and adaptation measures must become a priority.

FAQ

Global temperatures in 2024 have risen 1.54°C above pre-industrial levels. This increase is linked to climate change, which has intensified the frequency and severity of natural catastrophes worldwide.

Insured losses for 2024 exceed $135 bn globally. Two-thirds of these losses come from the US, driven by two major hurricanes and frequent severe thunderstorms. In Europe, severe flooding caused approximately $10 bn in insured losses, the second-highest ever for the region.

Climate change has amplified conditions leading to extreme weather events, such as intense flooding, stronger storms, and prolonged droughts. It has also intensified events like Storm Boris in Europe, which combined Arctic and Mediterranean air masses, creating severe flooding.

Europe and the UAE experienced significant flooding in 2024. Key events included Storm Boris in Central Europe, heavy rainfall disrupting Dubai in April, and flash floods in Spain during October. Global flood-related insured losses totaled nearly $13 bn.

Urban areas primarily face pluvial floods caused by extreme rainfall overwhelming drainage systems. Fluvial floods, linked to rising river levels, and storm surge floods in coastal areas also pose significant risks.

Economic development, urban sprawl into high-risk areas, and higher asset values are driving an annual 5–7% rise in insured losses. Climate change further exacerbates the severity and frequency of extreme weather events.

Adaptation measures such as dykes, dams, and flood gates are critical. These solutions are up to ten times more cost-effective than post-disaster rebuilding. Expanding insurance coverage and addressing protection gaps are also essential to enhance financial resilience.

………………

AUTHORS: Jérôme Jean Haegeli – Swiss Re’s Group Chief Economist, Balz Grollimund – Swiss Re’s Head Catastrophe Perils