Overview

With the global stock market amid some of its worst days in recent history, the impact on InsurTechs and InsurTech investors is undoubtedly being felt. Since the beginning of 2025, through this most recent quarter (Q2), some $9.3 trillion of company value is estimated to have been wiped from the stock markets, according to Gallagher Re’s latest Global Insurtech Report.

Investment in the insurtech space increased by 8.3% from the opening quarter of the year to $2.41 bn, as a rise in the average deal size masked a decline in the overall number of deals

The report follows on this year’s theme of ‘Geographic Trends and Regional Idiosyncrasies’, with a specific look at the EMEA region through an InsurTech lens. In addition to profiling various InsurTech businesses, clients and individuals, this report provides our readership with the most current InsurTech investment data and view on the general market (see How InsurTechs & Tech-Driven Innovation Changing the Insurance Industry?).

- InsurTech is showing signs of a small recovery, with Q2 funding up 8% on the prior quarter as total disclosed global InsurTech funding for the quarter reached an impressive $2.41 bn.

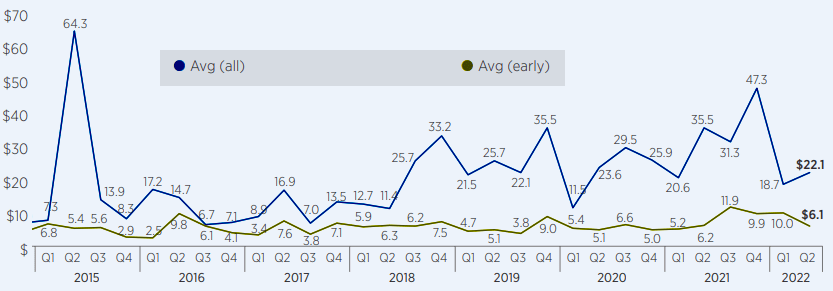

- Average deal size increased for the quarter by 18.3% – $22.11 million in Q2 compared to $18.72 mn in Q1.

- The increase in average deal size is however overshadowed by a 7.7% decrease in total Q2 InsurTech deals. Q2 saw 132 InsurTech deals, compared to 143 InsurTech deals in Q1.

- Total disclosed funding for L&H InsurTech reached $918M in Q2. This reflects a 12.4% increase in funding from the prior quarter, as well as an increase in deals. There were 40 deals for L&H InsurTech in Q2 compared to 37 in Q1.

- $948 mn was raised in six Q2 mega-rounds, including four based in the U.S.

InsurTech ecosystem has met a very interesting juncture; at a macro-level, be swept up in the downgrading of public value, or represent a viable investment alternative to an investor’s portfolio that is otherwise being dragged into generalised bearishness, and at a micro-level; either capitalise on the availability of lower-priced assets or struggle to survive.

Historically, contemporarily nascent technology companies in most industries have been hit hard (and early) during economic and market downturns. This is in part the perceived (and real) vulnerability that exists around their business models which are invariably not profit-making. During periods of economic optimism, the venture and growth capital that supports these firms serves as a core benchmark as it relates to overall company value, but as that optimism dries up (especially at a consumer level), so too does their market value.

This is not unique to InsurTech, but is particularly pronounced in any technological boom where valuations have been especially frothy – which for InsurTechs this has certainly been the case. The speed of gravitational pull back to reality has been very real for a number of InsurTechs in the last six plus months.

According to InsurTech Market Outlook, the global market saw overall growth of 15.4%, even with the COVID-19 pandemic, 2020 grew by 6.9%, and 2021 grew by 18.7%. 2022, however, to date has shrunk by 8.6%. Over that same time period, (known) global investments into InsurTechs recorded a growth rate of 52% in 2019, a 12% growth rate in 2020 and an incredible growth rate of 122% in 2021.

The ‘muted’ growth rate in 2020 was undoubtedly related to COVID-19 – H1 contributed just 35% of the total recorded funding in 2020.

All this to say, until now investments into InsurTechs (as a respective rate of growth) have outpaced relative overall growth in the global stock market. Again, this is not something specific to InsurTech but it is worth having these figures in mind when we begin to evaluate what the future might have in store for InsurTechs in general.

By the end of January of 2025, the global market was down 3.3%, and global investment into InsurTechs, during that month, was $751 mn.

In February, the market dropped down further still another 3.5%, global investment into InsurTechs during that month was $679 mn, and during March, the market actually picked up 2.3% growth. In that same month, investment into InsurTechs rose back up to $795 mn.

While we should not read too much into these parallels, it is interesting to consider the perception of true value held in these businesses as stand-alone companies, versus the potential for quick equity returns when the markets are otherwise bullish. Another observation on the direct impact that the general state of the market might have on investor confidence; four of the five mega-round deals done in Q1 occurred before the 24 February.

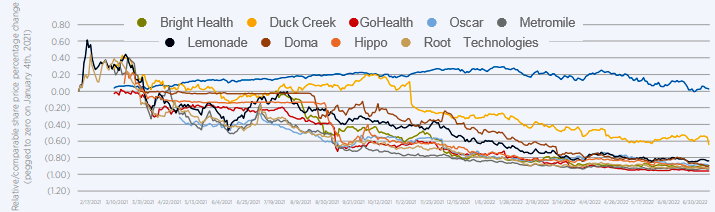

While we have just stated some key statistics referring to relative value as it relates to private investing (into InsurTechs), and the relative change in amounts being invested, below is a graph of InsurTechs who have gone public, pegged back to zero to show the relative change of their stock performance against their public InsurTech peer group, and also the S&P 500.

The markets seem to treat ‘InsurTech’ as one single animal when we consider the incredibly close correlation of their respective performances against one another – made very clear by the graph.

Duck Creek seemed to be the only exception to that rule, and them being an established software as a service InsurTech, versus risk originating InsurTech was often seen as the reason why. At the beginning of Q4, however, their relative performance began to behave and coalesce much more closely to the rest of the InsurTech pack (see 100 InsurTech Startups List that Transforming the Global Insurance Industry).

At the lowest end of the scale, a once high-profile InsurTech experienced penny-stock level share values during Q2, many others have experienced value loss drops of more than 90% in the last 12 months. Even before the market downturn, this trend was clearly occurring which does beg the question.

The impact of the global market downturn can clearly be observed on the graph from around the beginning of the new year.

While much less pronounced in that of the S&P line, we are well reminded that this is a blend of 500 very large, very diverse firms, and we are still observing a general downwards trend. What is particularly interesting is just how concentrated the public InsurTechs have become during these periods of no-confidence.

It certainly would strengthen the view that individual InsurTech performances are not being factored into their overall public value, and are in fact being treated as a group with little distinction between them.

It is not unusual for early-stage technology firms to be hit hard in periods of uncertainty, but what this does tell us is there is also a huge opportunity for discerning investors who are prepared to take the time to decipher which of these firms (at an individual level) is likely to bounce back with the most vigour — especially with some values getting close to pennies on the dollar (as it stands). As the market recovers, so too may a number or all of these businesses.

Relative/comparable InsurTech stock price changes

InsurTechs can still represent viable investment alternatives

As we have discussed, the global markets have struggled since the beginning of the year. In particular, market participants are nervous about overall global economic growth, largely thanks to high oil prices, the war in Ukraine and a spike in Chinese COVID-19 cases.

This overarching nervousness has undoubtedly affected much of the market with even the most robust stock valuations taking a beating. The most confident of investors will view this current climate as an opportunity.

InsurTechs who are set to deliver growth and profitability over the long-term present confident investors with an excellent opportunity to diversify their portfolios.

According to InsurTech`s evolution and investment landscape, in our midst are a number of InsurTechs who will undoubtedly change the face of (parts of) our industry (and in some cases most are already doing so). As the markets begin to recover and individual businesses are released from the bog of generalised scepticism, those InsurTechs should raise to the surface with the utmost buoyancy.

If nothing else, the same conditions that are in part responsible for this most recent dip are actually validating and vindicating what a number of InsurTechs are looking to remedy, improve and even solve. For example, as mentioned, there is now an accelerated shift towards renewable energy.

A number of InsurTechs are helping our industry to pioneer and forge a path forward that could literally revolutionise our industry.

As natural catastrophe events become more commonplace, those InsurTechs who are helping to underwrite flood, wildfire, named storms and climate change are also set to distinguish themselves as companies for the future.

We have already seen the impact that InsurTechs are having on delivering value in cyber and, small and medium-sized business product delivery.

The case is the same for potential around electronic vehicles, and of course no contemporary commentary on this topic would be complete without a nod to ESG-related matters (although our industry is still a far way off defining what they mean by this in any kind of meaningful manner — that can be consumed by the masses).

Capitalise on the availability of lower-priced assets

In the wake of any Schumpeterian gale of disruption, those displaced, or at least on the wrong side of victory, will present a further opportunity for (relatively) well-priced asset capture — whether that be human capital, technological assets or assumed market share.

This most recent downgrading of company values could well usher in conversations of M&A or divestitures that might have seemed unlikely even six months’ ago.

Historic shifts in the market do create bergschrund fissures for some industries and our own industry will almost certainly see cases of dislocation (we already are).

In the wake of a realisation of value, it could even be well-advised for certain InsurTechs to offload, and certain investors (even InsurTechs themselves) to acquire in this climate. If nothing else, this market downturn has coalesced together certain businesses and thrown a cold bucket of water over many InsurTechs who previously considered themselves special or unique. For both sides of the trade, this could be seen as an enormous opportunity.

The new face of survival – keeping hold of the cash

Very much in line with the opportunities surrounding the chance to acquire discounted assets is the very real, brutal reality of how much of this comes about – the struggles experienced by individual InsurTech businesses.

While InsurTech news is awash with big raises, big exits and expectations of grandeur, individual company struggles have always been a real feature of the InsurTech phenomena.

Most choose not to speak about it, but we cannot present a fair representation of what is actually going on (and has been since its inception) if we did not.

While company cessation, layoffs, revised growth targets have always existed, this most recent downturn in market performances has led to some fairly high-profile InsurTechs announcing significant staff layoffs.

At the end of May, a well-known U.S. InsurTech announced it was laying off 30% of its staff, despite having raised $50 mn at the end of 2021. At the beginning of June, another very high-profile InsurTech similarly announced the beginnings of a regrettable staff layoff, despite just two months before doubling its total funding to $250 mn in a Series E (see TOP 10 InsurTechs by the most venture capital).

This could of course be coincidental, but given the increased number of other InsurTechs announcing layoffs and the shutting of doors, there is a sense that for many InsurTechs, the last few months have been a real struggle to deliver what was once expected.

There will also be a feeling of real unrest with regards to ‘how long does this money need to last?’, and the obvious thing to do is to rein in expenses.

The issue of staff layoffs presents an interesting evolution of InsurTech capital raising; at the height of bullishness, let’s call it 2020 and 2021, one of the key mechanics to ‘add prospective value’ was to make a number of senior hires (usually seasoned (re)insurance individuals), and have a big development team on staff — at one point, certainly from the outside in, this seemed to be one of the biggest differentiating factors between InsurTech firms that could close on their mega-round deals.

When things are going well, and there is limited speculative fear that the next round of funding/liquidity event is not too far away, this is a very rational strategy

It is a very real reminder that for newer firms, especially those with limited revenue, being lean will always have its advantages. In most markets we are seeing a very real issue arising in the timing between fundraises.

While, as we have seen in Q1, there is still a good amount of capital available for pre-seed and seed funding, there is a concern (particularly among earlier stage investors) that Series A and B funding is a) no longer so readily available, and b) taking longer to be deployed.

The impact of this will then ultimately fall back on those pre/seed rounds unless InsurTechs bring to the table a very clear view of revenue generation almost out of the gate. Investors’ tolerance to fund losses indefinitely is understandably low.

Unfortunately, from an investor PR perspective, this momentum will undoubtedly take a lot of the shine and glisten away from InsurTechs in a way that has arguably not happened since 2012. It will also start sorting the wheat from the chaff (which is ultimately a good thing). Perhaps this scything motion from the market is the reality check we have been waiting for and expecting.

Geography in focus – Europe, the Middle East and Africa

As mentioned in first report, this year’s reports will have the prevailing theme of geographical regional idiosyncrasies and global trends.

We wish to review which businesses have honed their offering to specific areas, and which businesses have the prize of the global (re)insurance industry in their sights.

Given technology’s transcendental nature, and increased globalisation, it is perhaps unsurprising that many InsurTechs are looking to offer their products and services worldwide. In this second quarter, we will look at Europe, the Middle East and Africa (EMEA).

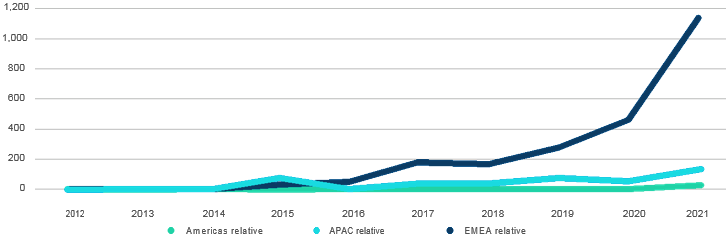

Relative Development of Regions – Total Funding

As a region in focus, EMEA has actually experienced the greatest amount of relative growth (from the starting point of 2012), up until the end of 2021 in terms of funding volume. Per the graph above, from 2012, to the end of 2021, EMEA observed a relative increase change in funding volume by 1,127.1 times.

Without meaning to mislead the reader, we will now reveal that in 2012 only $3.13 million had been invested, and in 2021 $1.1 billion was invested into EMEA — whereas the Americas recorded $344.6 million in 2012, and reached $9.9 billion in 2021.

If we put to one side the use of the label ‘InsurTech’ being more readily applied to U.S.-based InsurTechs in 2012, and the fact that we are essentially starting from a position of zero for EMEA InsurTechs in 2012, it is still a truly tremendous feat, and extremely noteworthy. In the space of a decade, the EMEA ‘InsurTech’ scene has literally exploded.

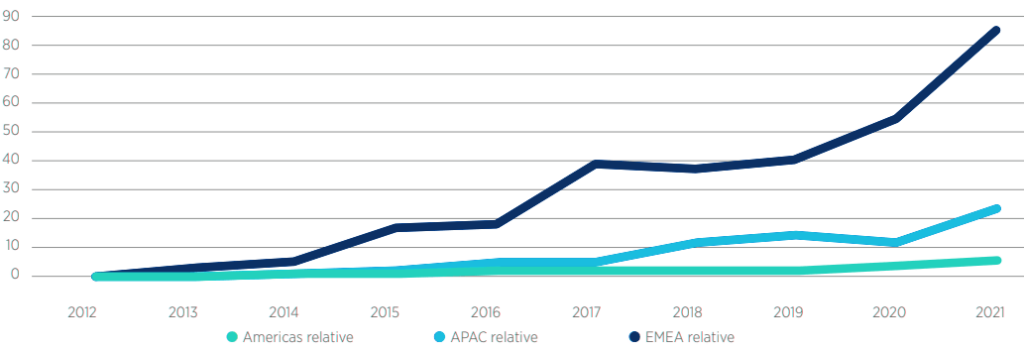

The relative deal count graph (below) shows a very similar story.

Relative Development of Regions – Total Deal Count

Specifically in the EMEA region, the UK tops the chart with total deal count and total amount of capital raised/invested. By the end of 2022 Q2, the UK had overseen 217 deals, which in total raised $3 billion. On both fronts this is second only to the United States (covered in our Q1 report). The UK also leads the EMEA pack with regards to mega-round deals, with six $100+ million deals completed by the end of 2022 Q2.

Existential pressure

We have commented at length on the state of the market, the impact on InsurTechs, and the potential view(s) held by traditional investors. One final mention should be made to the existential pressure put upon our industry more broadly that could also affect the fate of InsurTech as a social phenomenon, and at an individual company level — that of incumbent investment returns.

With many (re)insurer market returns performing below expectations, (re)insurers have understandably had to focus their attention on underwriting, distribution, capital restructuring, and belt-buckling.

While, over the long-term, InsurTechs could conceivably help in all of these areas, in the short-term, (re)insurers have been distracted.

In Q1, only one mega-round deal had any (re)insurer participation in the round (Markel and PruVen Capital into Cowbell Cyber), compared with Q4 2021, where 15 (re)insurers participated in nine of the 14 mega-round deals. As mentioned, there is a feeling that for the time being incumbents need to get back to basics which may be putting inadvertent pressure on technology budgets, but these events do make the case even more important to run maximised efficiency, however this process is slow and costly.

Industry incumbents are also far more discerning these days with their balance sheet allocations to InsurTechs. The risk capital that was once relatively available to unproven InsurTechs has become a precious commodity for many.

With equity returns not providing the hybrid commitment model (equity capital and risk capital) such stability as it once did, the pressure is on the risk returns to justify incumbent participation.

(Re)insurers in particular have been burned by many InsurTech experiments and many in the industry are just not going to tolerate this going forward. InsurTechs are having their underwriting capabilities and growth projections grilled in a way that we have not previously experienced.

Finally, some InsurTechs themselves are wanting to cool off their own growth stories. It is increasingly common for individual InsurTech businesses to shy away from the pressure of enormous valuations, and unrealistic growth expectations that make for very high intensity working conditions. Where capital is readily available, and founders have a great deal of confidence in their offering, more and more InsurTechs are actually driving for small rounds at smaller valuations.

Now is not the time to be yoked with unrealistic expectations. Founders and investors alike have become a lot more discerning about valuations and prices in general — the complete absence of companies going public is the best guide to show us this. If we also think of the number of unicorns created during certain periods of 2020 and 2021, and compare them to 2022, this is another sobering reminder of how companies themselves and investors are viewing their investable value.

We focused on Betterfly in our first report who themselves achieved unicorn status in 2022, and in Q2 Branch Insurance also achieved this once mythical status after a $147 million raise, valuing the business at $1.05 billion. Perhaps this cooling off period will once again reinstate the rarity and scarcity that the term unicorn suggests for future rounds of funding.

Average Deal Size ($ mn)

If we look back to Q1 data, there is still a huge drive to invest into InsurTech businesses at certain parts of the investment lifecycle — ‘early stage’ funding was at a record high, while overall funding was dramatically down, and overall deal count remained unmoved.

This would suggest that investors are reverting back to hedging their bets with wide nets, which is producing a healthy availability of capital at the truest venture phase, and democratising the allocation of capital.

This trend could well help InsurTechs in the long run by forcing them to consider profitability earlier in their growth story which could ultimately ensure that stronger foundations are built at such a vital stage of company growth.

We had also seen in recent quarters a huge allocation of capital at the very top end of the investment lifecycle (C, D and E rounds). If we combine these two contemporary observations together, we are left with the conclusion that the appetite for investors into ‘InsurTechs’ at both the unproven and proven ends of the spectrum remains very strong indeed.

InsurTechs now need to bridge the gaps themselves with actual results as the propping capital of Series A to C becomes increasingly discerning in these uncertain times. As mentioned, at a macro level at least, this market downturn is possibly the best thing that could of happened to improve the quality of InsurTech offering — the days of wheel stabilisers and kid gloves looks over. InsurTechs, prepare to graduate.

InsurTech showing signs of small recovery, with Q2 funding up 8% on the prior quarter

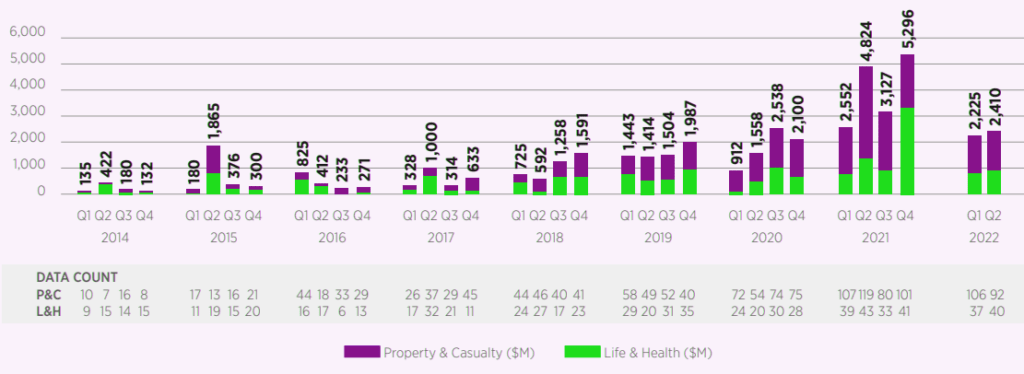

Total disclosed global InsurTech funding for the quarter reached $2.41 billion. Global InsurTech funding increased 8.3% in Q2 compared to Q1—a stark difference from the 58.0% drop in funding in Q1. Funding for InsurTech is however down 50.2% year on year.

It is noteworthy that a year ago, saw the second-most funding for InsurTech on record at $4.84 billion. What a difference a year makes.

Average deal size increased for the quarter by 18.3% — $22.11 million in Q2 compared to $18.72 million in Q1. The increase in average deal size is overshadowed by a 7.7% decrease in total Q2 InsurTech deals. Q2 saw 132 InsurTech deals, compared to 143 InsurTech deals in Q1.

L&H InsurTech growth outpaces P&C InsurTech

Total disclosed funding for L&H InsurTech reached $918 million in Q2. This reflects a 12.4% increase in funding from the prior quarter, as well as an increase in deals. There were 40 deals for L&H InsurTech in Q2 compared to 37 in Q1. Among deals with disclosed funding, the average deal size was $24.81 million for the quarter.

57.5% of L&H InsurTech deals were for companies focused on lead generation or distribution

Funding for P&C InsurTech also increased in Q2, although deals were down 13.2%. $1.49 billion was raised by P&C InsurTech in Q2, which is an increase of 5.9% from the previous quarter. There were 92 deals for P&C InsurTech in Q2—14 less than the previous quarter. Among deals with disclosed funding, the average deal size was $20.73 million for the quarter. The bulk of deals for P&C InsurTech were between companies focused on distribution and B2B — 48.9% and 46.7%, respectively.

Q2 saw $368 mn in early-stage InsurTech funding — a 44% decrease from Q1.

Total disclosed funding for early-stage InsurTech was at $368 million in Q2. Notably, the category saw a 44.4% decrease in quarter on quarter and a 26.1% decrease in year-on-year funding.

This is attributable to a 53.7% quarter on quarter drop in funding for early-stage P&C InsurTech. In Q1, early-stage P&C InsurTech raised $582 million in funding.

Meanwhile, Q2 saw early-stage P&C InsurTech raise $269 million in funding. Funding for early-stage L&H InsurTech increased 23.8% quarter on quarter — from $79.81 million in Q1 to $98.83 million in Q2.

In addition to the funding drop for early-stage InsurTech, deals and average deal sizes also decreased in the quarter. Q2 saw 70 deals for early-stage InsurTech, which is five deals fewer than in Q1. Continually, Q2 saw average deal sizes for early-stage InsurTech fall by 38.8%—$6.14 million in Q2 compared to $10.03 million in Q1.

Quarterly InsurTech Funding Volume — All Stages

$948 mn was raised in six Q2 mega-rounds, including four based in the U.S.

Q2 saw $948 million raised in mega-round InsurTech funding, which is a 42.8% increase quarter on quarter and a 69.7% decrease year on year. $605 million was raised across four P&C InsurTech mega-rounds whereas $343 million was raised across two L&H InsurTech mega-rounds.

Four of the mega-round InsurTechs for the quarter are U.S.-based. Together, the U.S.-based InsurTechs raised $635 million in funding.

San Francisco-based Newfront Insurance, a technology-powered commercial insurance brokerage, raised $200 million in Series D funding in April. Newfront Insurance’s deal was the largest mega-round for the quarter.

U.S.-based InsurTechs also raised the most deals in Q2, which is consistent with the rolling average across previous quarters. In total, the 60 deals raised by U.S.-based InsurTechs comprised 45.5% of global InsurTech equity deals.

Outside of the U.S., the UK. saw a big increase in its share of global InsurTech deals. 12.1% of global InsurTech deals in Q2 were for U.K.-based InsurTechs—a number over 4% points higher than the rolling average.

(Re)insurers made 28 private technology investments in Q2.

There were 28 InsurTech investments in Q2 by (re)insurers, which is five less than the previous quarter. With 61 deals for the year, however, InsurTech investment by (re)insurers exceeds the 48 deals by (re)insurers in Q1 and Q2 of 2021.

Notably, Series A investment by (re)insurers comprised 32.1% of all (re)insurer InsurTech deals—the highest level since 2020.

On the partnership side, notable activity comes from Coalition and Munich Re. San Francisco-based Coalition, a provider of cyber insurance and security, announced two partnerships with insurance carriers in Q2.

The first with specialty insurer Ascot Group in April and the second with Allianz in June. In May, Munich Re announced the establishment of the “Mobility Technology Center” with three partners—ERGO Digital Ventures, In-tech, and MaLiBu.

Other partnership activities include Beazley’s partnership with London-based Cytora and SiriusPoint’s partnership with Munich-based Garentii.

………………………………..

AUTHOR: Andrew Johnston – Global Head of Gallagher Re InsurTech