Insurtech UK has released a roadmap with recommendations for policymakers to maintain and enhance the UK’s leadership in insurance innovation. The plan details how the next government can support the growth of the UK insurtech market. Insurtech plays a vital role in the UK economy.

The United Kingdom is positioned as a global leader in the field of insurtech. A flourishing ecosystem of start-ups, investors, and incumbents is working together to drive innovation and growth in the industry, from AI and machine learning to the Internet of Things.

UK insurtech has an estimated combined value of more than $20 bn, making it the third largest globally after the USA and China, with an annual revenue of £2-3 bn

The industry supports more than 60,000 jobs and contributes nearly £5 bn to the UK GDP. The United Kingdom’s insurtechs have not been immune to the recent global tightening on valuations.

UK’s insurtech market structure

Indeed, of the estimated 3,000 insurtech firms in the world, approximately 280 are located in the UK — the highest number of insurtechs per capita among all major world economies

The UK boasts the world’s second-largest insurtech cluster, characterized by its impressive scale and economic impact:

- Number of Firms: There are 280 insurtech companies, with approximately one-third located outside London.

- Combined Value: These firms have an estimated collective worth exceeding $20 billion.

- Unicorns: The UK is home to 8 insurtech unicorns, surpassing any other European country and second only to Silicon Valley.

The insurtech sector in the UK is notable not only for its size and value but also for its dynamic and diverse workforce.

Opportunities for insurtech growth include developing or deploying new technologies, more partnerships with insurers, and international expansion.

Barriers cited in recent sector surveys include access to funding, access to talent, and new customer acquisition.

The industry is already working together, through its trade association Insurtech UK, to cultivate a proactive ecosystem that inspires and strengthens UK start ups and scale ups.

It employs around 14,000 people, with a notable demographic profile:

- Age Distribution: Two-thirds of the workforce are under 40 years old.

- Gender Diversity: Nearly half of the employees are female, highlighting the sector’s commitment to diversity and inclusion.

The multiples of some of the most successful publicly listed insurtechs fell from 15 times those of traditional peers to below the level of incumbent insurers, and private capital funding decreased 32% compared with the peak in 2021 (see InsurTech`s evolution and investment landscape).

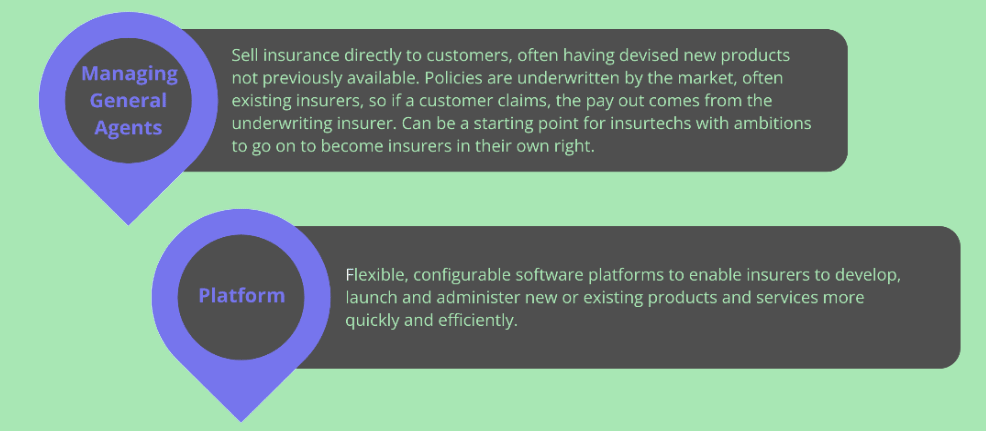

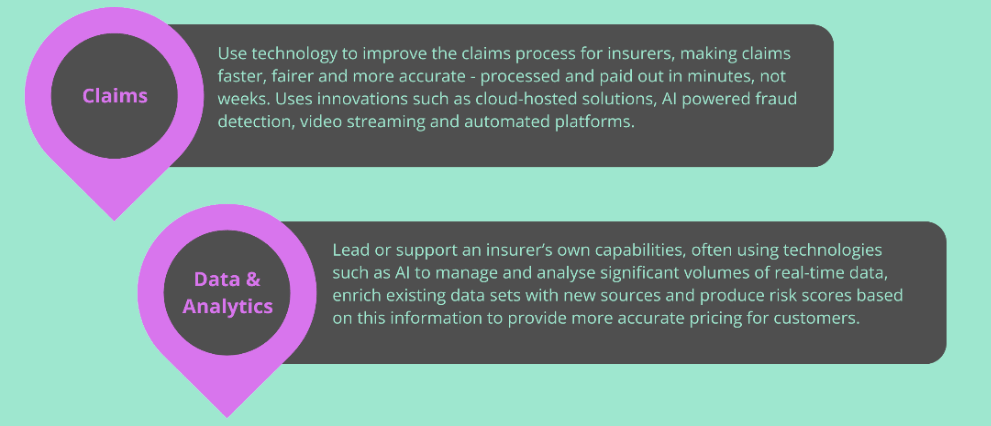

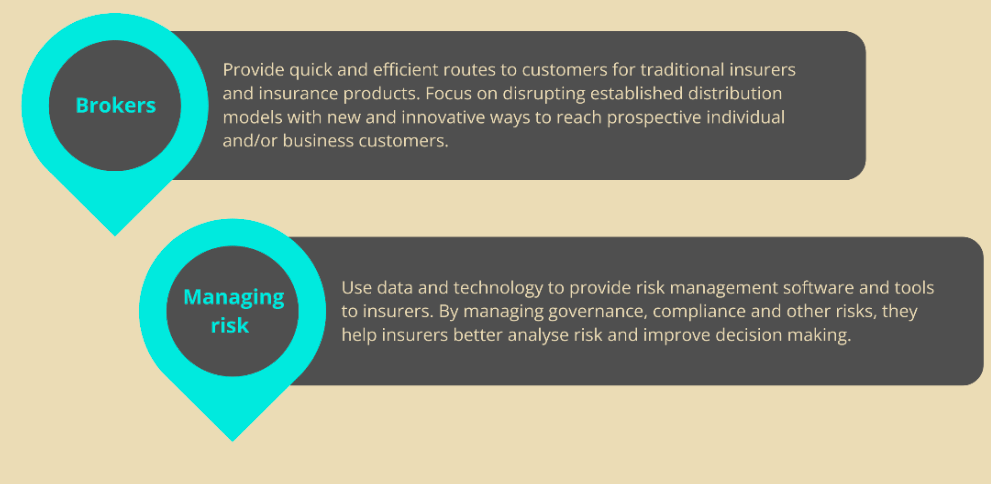

Categories of Insurtech

The UK InsurTech sector in 2024 continues to thrive, characterized by innovation and growth

Startups and established companies alike leverage advanced technologies like AI, blockchain, and big data to streamline operations and enhance customer experiences.

According to Global InsurTech Funding report, investments in this sector remain robust, with both venture capital and corporate funding driving new initiatives.

The average deal size experienced a reduction of 30.6%, decreasing from $14.14 mn in the fourth quarter of 2023 to $9.8 mn in the first quarter of 2024.

This marks the first time since the third quarter of 2017 that the average global InsurTech deal size has fallen below $10 mn.

P&C InsurTech funding also declined, dropping 22.5% to $605.6 mn in the first quarter of 2024, the lowest since the third quarter of 2018.

The average deal size in this category reached its lowest point since the first quarter of 2018 at $10.09 mn, and the total number of deals decreased to 70, a reduction of six deals from the previous quarter.

The roadmap outlines three main themes for government action to foster UK insurtech growth:

- A regulatory regime that encourages new entrants

- An investment environment that supports funding

- Initiatives to unlock scaling opportunities

Key recommendations include creating a regulatory framework that attracts new businesses and establishing an investment climate conducive to funding and growth.

The roadmap suggests the Department of Business and Trade develop a long-term framework to ease international expansion and investment for UK insurtech companies.

Financial recommendations include extending the (Seed) Enterprise Investment Schemes to all insurtech categories and broadening Enterprise Management Incentive criteria to attract skilled talent (see about Global Landscape of Insurance Digital Transformation).

Insurtech UK calls for government-backed reinsurance schemes to cover new societal risks and support affordable insurance, promoting financial inclusion.

To lower entry barriers and stimulate growth, the roadmap proposes a fairer VAT/IPT regime. These comprehensive recommendations aim to help UK insurtech achieve its full potential.

Key recommendations with the roadmap

Regulation and Digital Transformation

A regulatory regime that enables more new entrants

Recommendation 1

The PRA to maintain momentum in evolving the regulatory regime to the needs and structures of insurtechs as they start and scale, including:

- a: a swifter, more transparent application process for PRA authorisation

- b: clear guidance and communications as the new PRA mobilisation regime is introduced and embedded, meeting the commitment to be in place by end 2024

Recommendation 2

The FCA to work closely with the insurtech industry to ensure the ongoing availability of, and confidence in, a proper Appointed Representative scheme which allows market access for start-ups and enables future innovations in embedded insurance

Recommendation 3

Regulators to deploy a progressive, enabling approach to emerging technologies such as AI, blockchain and Open Finance, taking into account how these may best be applied within an insurance context to maximise consumer benefit and confidence

Access to Finance

An investment environment that facilitates funding

Recommendation 4

HM Treasury should extend SEIS and EIS to all categories of insurtech to incentivise more investment into this high-potential sector, and to prevent a cliff-edge where Managing General Agents may transition to being a regulated insurance firm

Recommendation 5

HM Treasury should significantly extend qualifying criteria for EMI from its current limit of £30 mn gross assets to attract more experienced talent as insurtechs scale

Recommendation 6

HM Treasury should re-extend the long-stop date for Advance Subscription Agreements back to 12 months, removing the additional pressures on concluding accelerated funding rounds that reducing this to 6 months has created

Recommendation 7

An urgent review of the HMRC R&D credit scheme should be conducted to provide clarity, consistency and confidence in both the application of scheme criteria and scheme administration

Recommendation 8

The value and positive impact of Innovate UK’s Professional and Financial Services programme supporting research and development in insurance should be recognised and expanded by HM Treasury in future spending rounds

Tackling barriers and driving growth

Targeted action that unlocks future potential

Recommendation 9

HM Treasury should introduce a fairer VAT/IPT regime, enabling insurtechs to scale quicker and on a level playing field with other tech sectors

Recommendation 10

A three year strategy from the Department for Business and Trade for international promotion of UK insurtech – to facilitate access to key overseas jurisdictions and encourage inward investment, drawing on evidence of priority countries and positive past experiences with insurtech corridors and fintech bridges

Recommendation 11

New government-backed reinsurance schemes (Innovation Re) should be scoped by HM Treasury to enable cover of new societal risks or act as a back-stop for new accessible and affordable insurance policies providing greater financial inclusion in insurance

…………………..

by Peter Sonner — Editor at Beinsure Media

by Peter Sonner — Editor at Beinsure Media