Overview

4 years after the pandemic began in 2020, many countries still report higher death rates. This trend persists despite differences in healthcare systems and population health. It holds even when accounting for population changes and the varied ways countries report and classify deaths, which complicates comparisons. There may also be under-reporting of excess mortality.

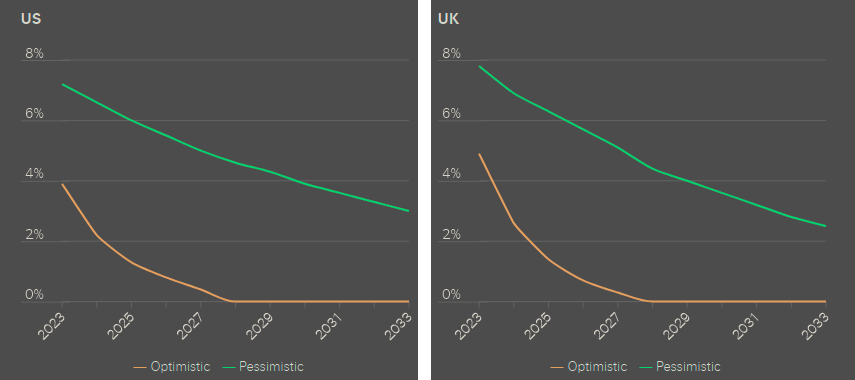

According to Swiss Re Institute’s report The future of excess mortality after COVID-19, if the ongoing impact of the disease is not curtailed, excess mortality rates in the general population may remain up to 3% higher than pre-pandemic levels in the US and 2.5% in the UK by 2033.

COVID-19 is far from over. The US reported an average of 1500 COVID-19 deaths a week for 2023 – comparable to fentanyl or firearm deaths. If this continues, our analysis suggests a potential scenario of elevated excess mortality extending over the next decade.

Paul Murray, CEO L&H Reinsurance at Swiss Re

However, excess mortality can return to pre-pandemic levels much sooner. The first step is to get COVID under control, with measures such as vaccinations for the vulnerable, according to Forinsurer. Over the longer term, medical advancements, a return to regular healthcare services, and the adoption of healthier lifestyle choices will be key.

The key findings

- Report suggests potential excess mortality in the general population of up to 3% for the US by 2033 and 2.5% in the UK, the longest period of elevated peacetime excess mortality in the US

- Key driver of excess mortality is the lingering impact of COVID-19; both as a direct cause of death, and as a contributor to cardiovascular mortality

- Reducing the impact of COVID-19 on elderly and vulnerable populations will be key to excess mortality returning to zero

Excess mortality, insurance and medical advancements

Excess mortality is a measure of the number of deaths above an expected level in a given population. Typically, all-cause excess mortality should be around zero, as the major causes of death remain relatively stable over the long-term baseline assumption (see TOP 100 Life & Health Insurance Companies in the U.S. in 2024).

Fluctuations in excess mortality tend to be short-term, reflecting developments such as a large-scale medical breakthrough or the negative impact of a large epidemic. However, as society absorbs these events, excess mortality should revert to the baseline.

Since 2020, calculating excess mortality has been a significant challenge. Excess mortality refers to deaths exceeding the expected number. Different methods to estimate expected mortality produce varying results.

For Life and Health insurance, this poses a challenge. If population mortality trends continue, insurers could face years of increased claims, according to Health Insurance Market Trends. Persistently high excess mortality may impact the long-term performance of existing life insurance portfolios and affect the pricing of new policies.

Scenario forcasts for US and UK, general population excess mortality

In this research Swiss Re Institute projects excess mortality in the US and UK over the next 10 years under different scenarios, by analysing excess mortality trends globally and disaggregating the underlying factors driving them. We find that excess mortality persists today and may potentially continue for the next decade.

Our general population forecasts suggest that excess mortality will gradually tail off by 2033, to 0–3% in the US and 0–2.5% in the UK. In comparison, by our calculation excess mortality in 2023 was in the range of 3–7% for the US, and 5–8% in the UK.

With COVID-19 this has not been the case and all-cause excess mortality is still above the pre-pandemic baseline. In 2021, excess mortality spiked to 23% above the 2019 baseline in the US, and 11% in the UK.

If the underlying drivers of current excess mortality continue, Swiss Re Institute’s analysis estimates that excess mortality may remain as high as 3% for the US and 2.5% for the UK by 2033.

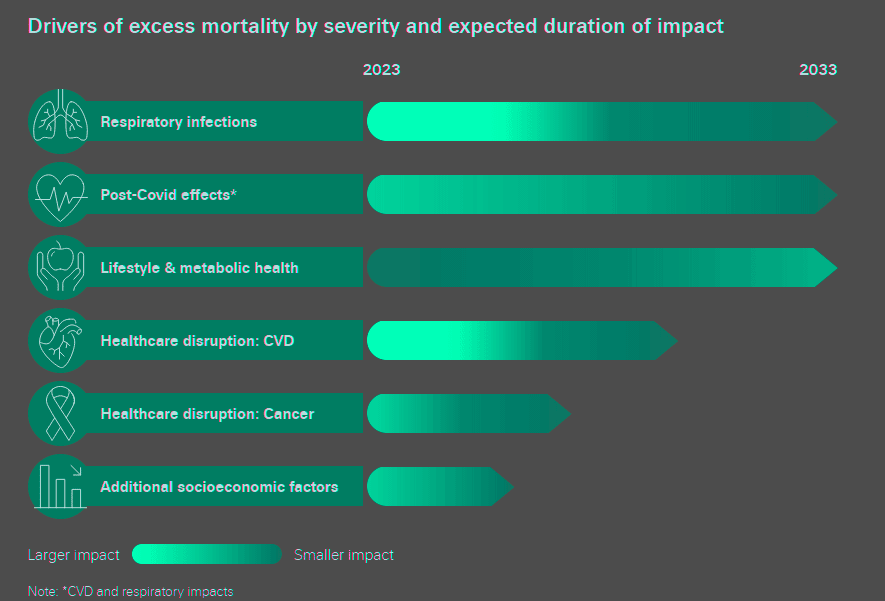

The primary driving factor of both current and future excess mortality is respiratory disease (including COVID-19 and influenza), with other causes including cardiovascular disease, cancer and metabolic illnesses. The cause of death split varies by a country’s reporting mechanism.

Optimistic scenarios require healthcare and medical advancements

Swiss Re’s report examines an optimistic scenario where excess mortality rates return to pre-pandemic levels as early as 2028. In this scenario, medical advances, such as weight loss injectables and cancer developments such as personalised mRNA vaccines, combine with a drop in the impact of COVID-19 and healthier lifestyle choices.

Under an optimistic scenario, we find that US and UK pandemic-linked excess mortality would disappear by 2028, reverting to pre-pandemic mortality expectations. Under a pessimistic scenario, we expect excess mortality to remain elevated until 2033, above pre-pandemic expectations.

The ranges allow for varying mortality improvement assumptions – used to calculate the expected level of mortality – and differing data quality and reporting methods. Our estimates use our chosen approach for the mortality improvement assumption and so may differ from those reported by other institutions.

We created a standardized method to compare pandemic-era excess mortality across countries.

Four key patterns emerge:

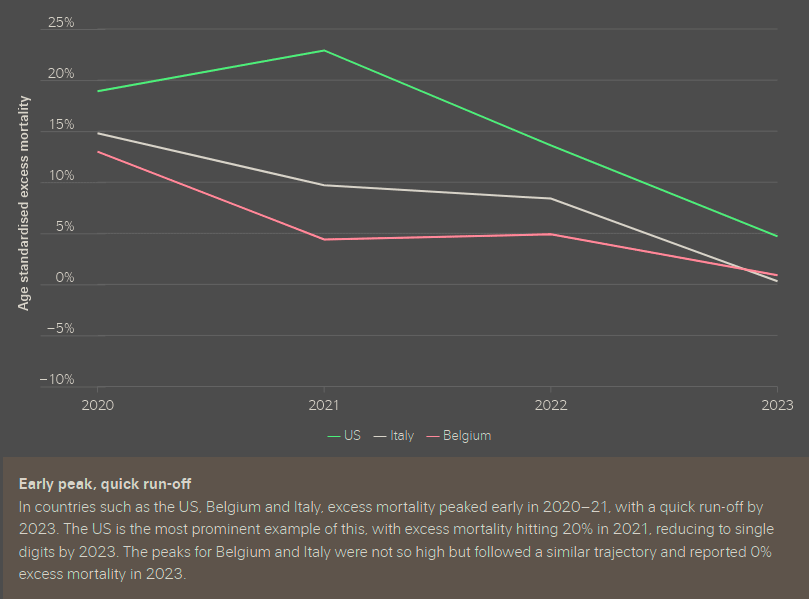

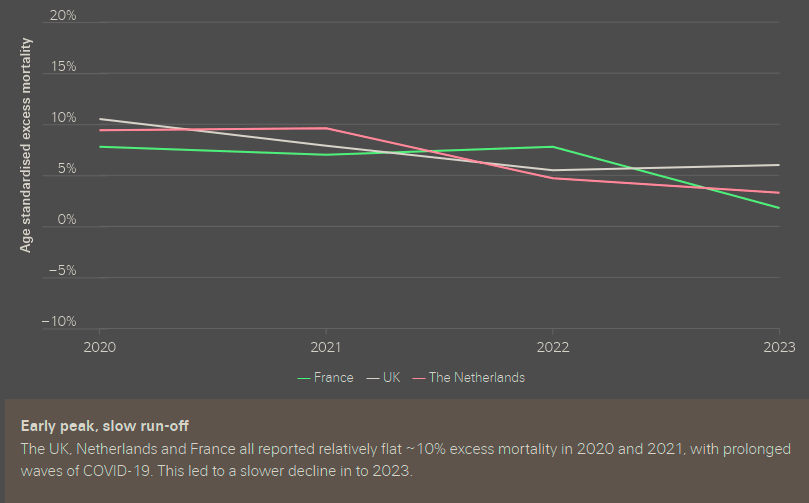

- In the US, excess mortality spiked early and dropped quickly. In the UK, after an early peak, the decline was slower.

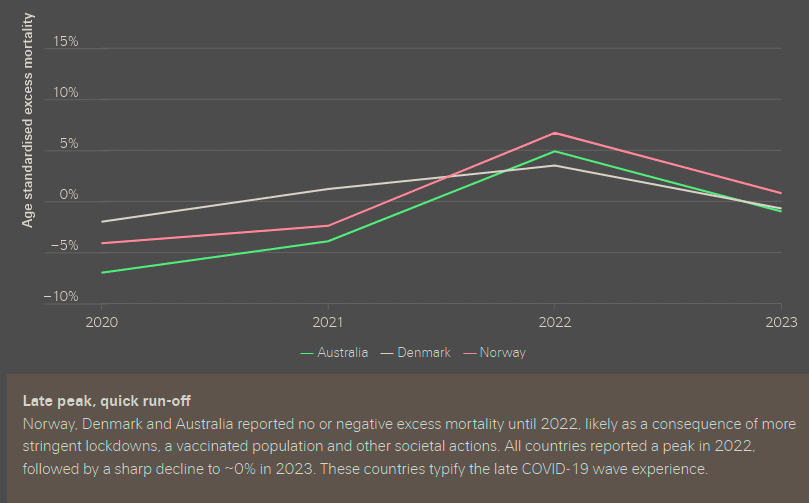

- Australia delayed its peak by almost two years, followed by a rapid decline.

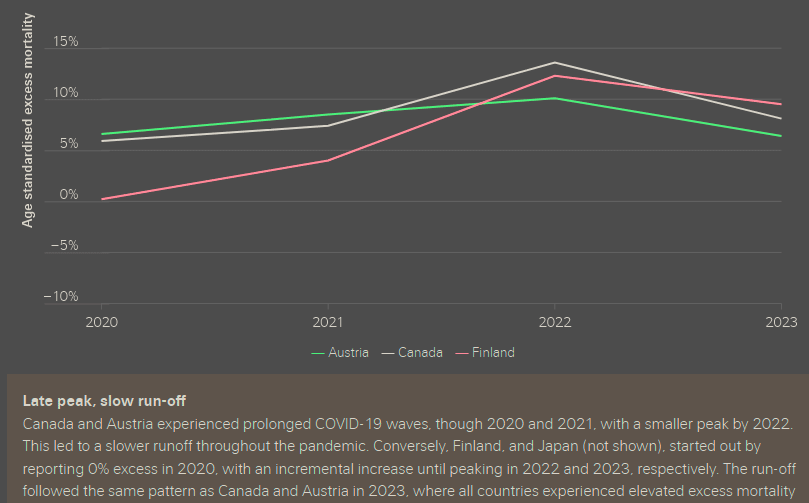

- Canada saw very low excess mortality in 2020, with a gradual rise peaking in 2022 and 2023, indicating a late peak and slow decline.

These trends align with each country’s COVID-19 response, particularly the timing and effectiveness of preventive measures and how quickly mortality rates returned to expected levels.

The pandemic has reshaped the causes of excess deaths. We examined major causes of death since 2020 in developed nations that provide data. Respiratory mortality has been the largest contributor to excess deaths each year since 2020.

However, there is evidence of inconsistencies in recorded causes, suggesting that some deaths were misclassified as COVID-19.

UK and US data show a sharp, unexplained rise in cardiovascular disease (CVD) deaths since 2020. Some countries also reported excess deaths over pre-pandemic levels for other major causes like cancer.

Drivers of excess mortality

COVID-19 continues to drive excess mortality both directly and indirectly, based on current medical trends and expected advancements. In the long term, lifestyle factors like poor metabolic health, obesity, and diabetes may also contribute to rising mortality rates. Insurers should closely track excess mortality and its underlying causes in the general population and compare trends with the insured population.

Indirect impact of cardiovascular disease (CVD) mortality

The interplay between COVID-19 and cardiovascular death rates is significant for excess mortality. The virus itself has a direct impact because it contributes to causes of death such as heart failure.

Further, COVID-19 has had an indirect impact via the disruption to healthcare systems – a factor which emerged in the pandemic years.

This disruption has led to a backlog of essential cardiac tests and surgeries, meaning that conditions such as hypertension have been underdiagnosed and therefore not treated.

Implications for insurers

Excess mortality in the general population is an important indicator for insurers, as shifts in the major causes of death may require a reassessment of additional risk in their mortality portfolios.

The current levels of excess mortality are of concern. However, there are a range of tools available for insurers and reinsurers to manage this trend.

Specific actions include adapting the underwriting philosophy, risk appetite, and mortality assumptions in pricing and reserving. Insurers can be proactive in targeting prevention programmes for policyholders, helping them in the joint effort to support longer, healthier lives.

………….

AUTHORS: Daniel Meier – Life & Health R&D Manager, CUO L&H Reinsurance at Swiss Re, Prachi Patkee – Life & Health R&D Analyst, CUO L&H Reinsurance at Swiss Re, Adam Strange – Life & Health R&D Manager, CUO L&H Reinsurance at Swiss Re