Overview

The surge in interest rates to 15-year highs significantly improves the outlook for life and annuity insurance. The global life insurance industry today looks very different to 15 years ago. Low interest rates from 2008 until the inflation surge after 2021 put huge strain on the traditional life insurance business model of using balance sheet leverage and investment income to deliver contractual promises to policyholders.

According to Swiss Re sigma 2/2024, after over a decade of low demand due to low interest rates, profitability is recovering as higher government bond yields enhance investment returns and margins on life insurance products.

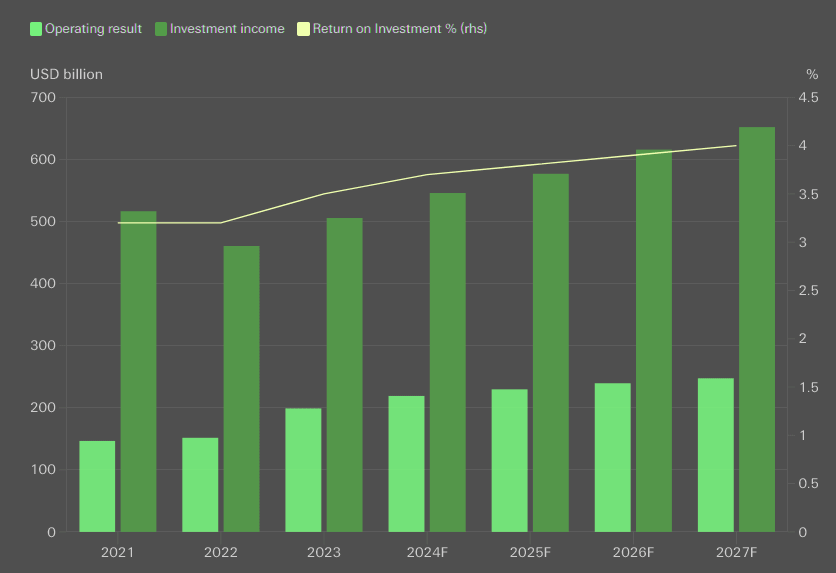

Swiss Re project a more than 60% increase in operating results for insurers in the eight largest life insurance markets over the next five years, driven by a 40% rise in investment income.

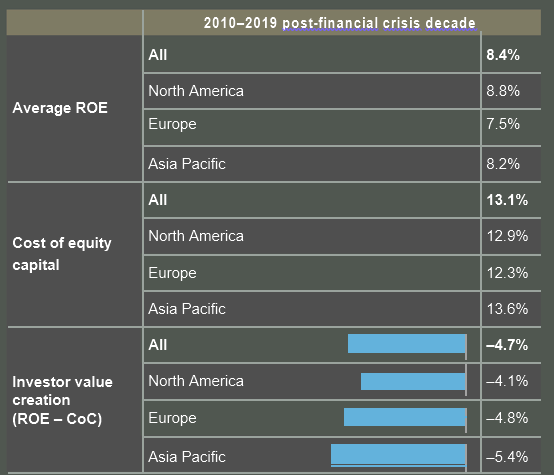

In contrast, the sector missed its cost of capital by nearly 5 percentage points annually on average in the decade following the global financial crisis.

Life insurance stock market indices, which reflect profitability expectations, now outperform broader markets as investors acknowledge the benefits of higher rates. Long-duration business stands to gain the most in profitability over the long term due to compound interest.

Higher interest rates improve the attractiveness of saving products

Low interest rates had made life savings products less appealing. Real premium growth for savings business fell below global economic growth in the decade after the global financial crisis, averaging just 1.1% annually.

Today, consumers are rapidly purchasing life products to secure higher retirement incomes.

Swiss Re expect strong, annuity-driven growth in the life savings market as the interest rate reset makes savings products more attractive.

US fixed annuity sales are projected to reach a new record this year, following a more than twofold increase in 2023 compared to any previous year before 2022.

Life insurer operating results and investment return, key markets

This demand boost should help mobilize the substantial private savings needed to narrow the retirement savings gap between current pension assets and the amount required for secure retirements, according to Top Trends in the Global Life Insurance Market.

US individual annuities direct business, first year and single premiums

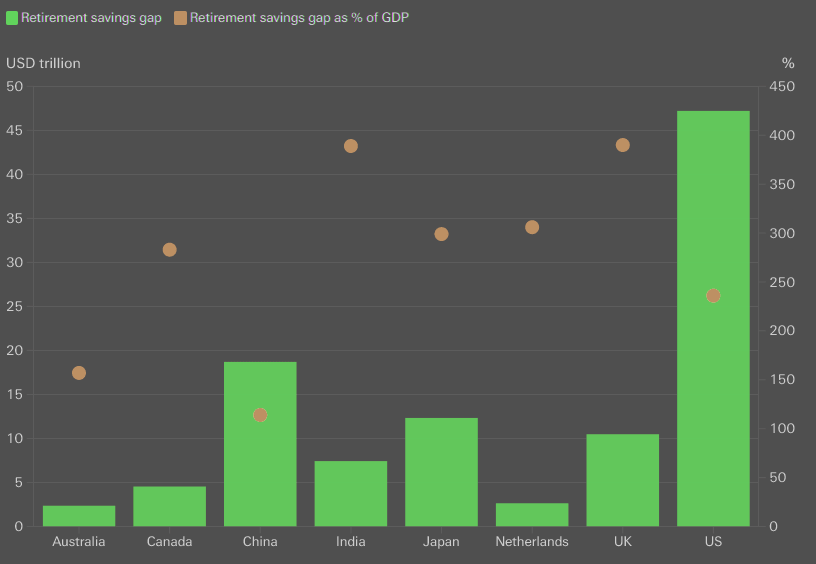

Swiss Re estimate the retirement savings gap for six advanced economies, China, and India at USD 106 trillion in 2022 values.

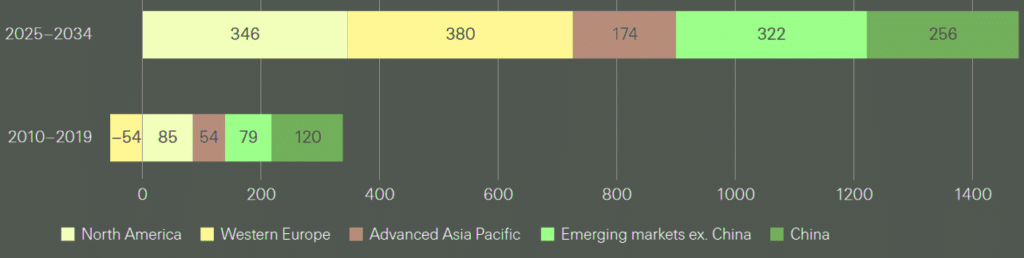

After less than USD 300 billion of premium growth from 2010 to 2019, Swiss Re predict life insurers will gain USD 1.5 trillion in savings premiums over the next decade, reaching USD 4 trillion by 2034.

Low interest rates handicapped the life insurance business model

The environment prompted stock insurers to shift from traditional business to capital-light, fee-based strategies to meet investor return expectations. Private equity firms absorbed the legacy assets divested via reinsurance. Mutual insurers pursued traditional business.

Publicly traded life insurers’ performance under low interest rates in the post-global financial crisis

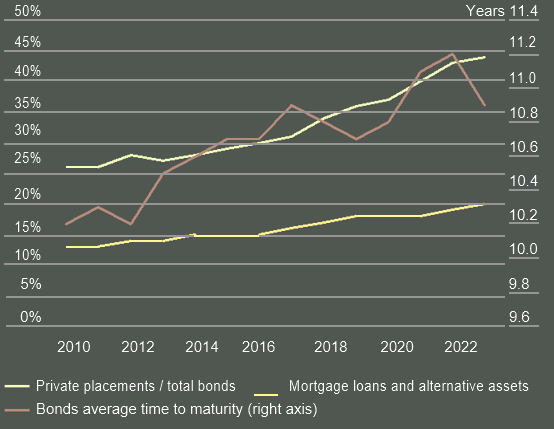

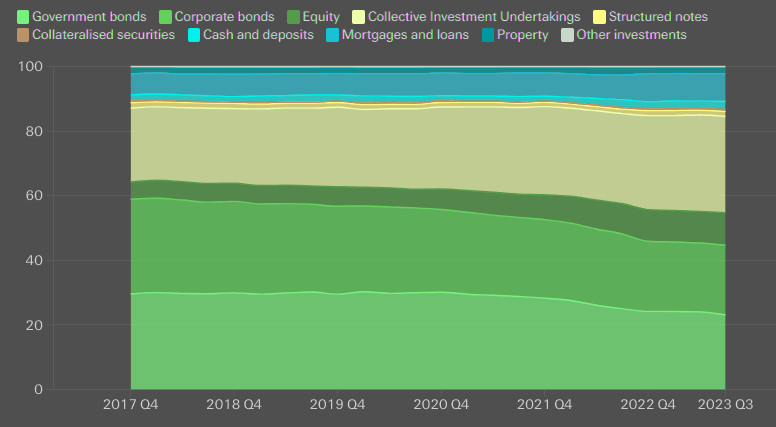

Worldwide, insurers shifted into higher-yielding illiquid and alternative assets and extended the duration of fixed income portfolios.

US life insurance industry portfolio allocations

European life insurance industry portfolio allocations

Life industry is shifting to a sustainable growth mode

Rising interest rates have transformed the competitive and operational environment for life insurers from one of low growth and low profitability to higher growth and higher returns, particularly for asset-intensive business.

Consequently, the life industry is shifting from returning excess capital to shareholders to requiring sustainable capital growth to support asset and biometric risk growth.

From 2009 until the rapid monetary tightening in 2022, stock insurers shifted to capital-light products and used reinsurance transactions to offload legacy liabilities.

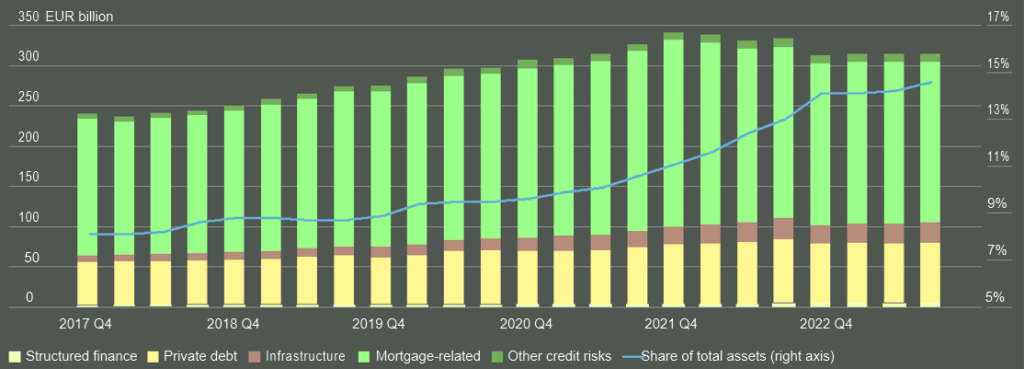

Estimated illiquid and potentially risky investments of European life insurers

Private equity capital acquired many of these legacy annuity assets, recognizing that low interest rates provided an opportunity for asset managers to outperform by investing in higher-yielding, illiquid, and private assets.

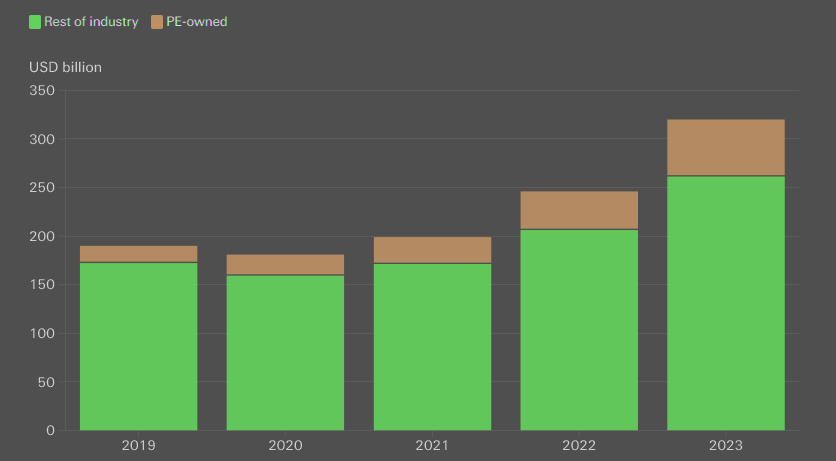

Life and annuity insurers are adding asset management

PE-owned insurers’ acquisitions provided stable funding to develop their investment operations and grow their assets under management (AUM) and earnings. For some, insurance assets now constitute a large share of their total AUM.

Swiss Re estimate that more than USD 1 trillion of life assets have transferred to PE-owned insurers globally since 2009.

They now own roughly 25% of US individual annuity liabilities and are expanding in markets like Japan.

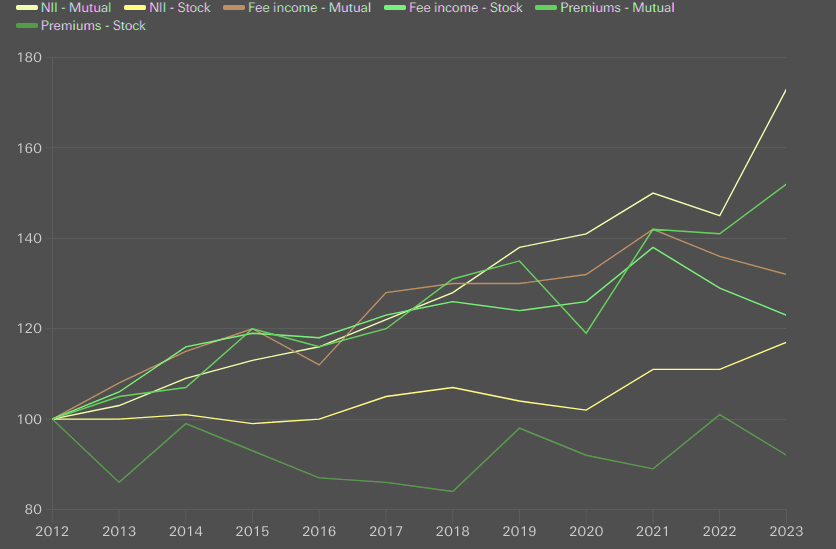

Growth in net premiums, net investment income and fee earnings for stock and mutual insurers

However, PE-owned insurers face increasing competition from insurer-owned asset managers, as insurers expand their own asset management capabilities, benefiting from the rise in unit-linked business.

Retirement savings gap, USD trillion

Swiss Re expect further growth and competition in asset management, with more hybrid product launches.

Rising interest rates transformed life insurance to higher profitability

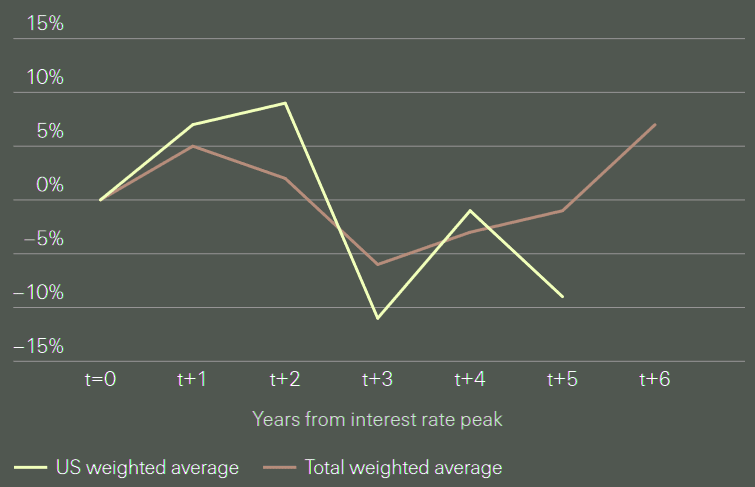

Rising interest rates tend to increase policyholder lapse rates while putting pressure on asset prices. In extreme scenarios, this can cause liquidity or solvency issues for insurers. Lapse rates have risen in key markets since 2020, but our modeling suggests that the peak lapse risk has passed.

A 100-basis point rise in policy rates correlates with a 30–35 basis point average increase in lapse rates, all else being equal.

However, about 50% of the lapse risks associated with rate rises materialize within the first three to four rate-hiking periods, which is behind us in advanced economies.

Rising rates have also increased credit risks in areas such as commercial real estate, but life insurers’ exposures are generally manageable.

The return to higher rates improves prospects for life insurers but also brings new risks

Higher interest rates strengthen demand for life saving products and insurer profitability. Rising interest rates can also heighten liability and asset stress, but our modelling suggests that peak lapse risk has passed.

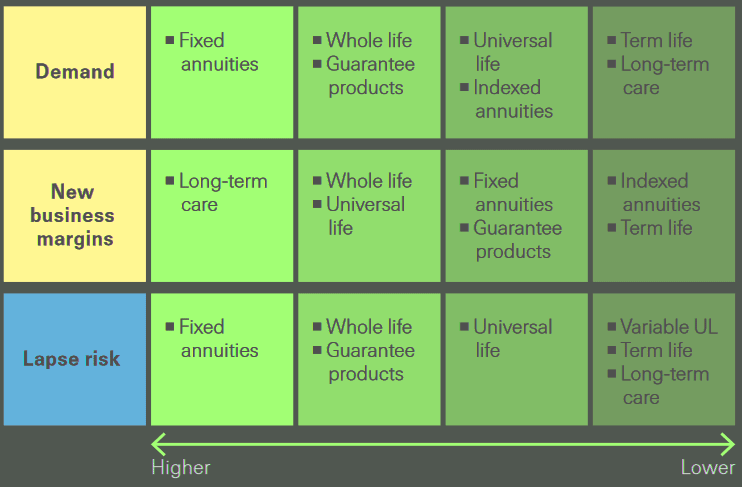

Sensitivity of life insurance products to rising interest rates

Change in lapse risks in monetary policy loosening environments

Today, listed insurers are retaining more of the assets that brought private equity entrants to the life insurance sector, sometimes by establishing “sidecars” to manage assets offshore. Private equity-owned insurers are ramping up direct retail sales of key life products.

Consumers stand to benefit from higher interest rates and greater competition

Strong forecast growth in saving premiums by 2034 should help to address protection gaps and improve retirement security globally.

Life and annuity savings business

Forecast additional premiums 2025–2034, compared to post-global financial crisis decade 2010–2019, USD bn

Higher interest rates dramatically improve the outlook for life insurers. Demand for savings-related products is surging, with US fixed annuity sales in 2023 more than twice as high as in any other year other than 2022.

Swiss Re expect record sales in 2024 too. Profitability is improving as well, with greater room for margins in new spread-based products and opportunity to reinvest assets backing legacy liabilities at a higher rate.

This is possible when the duration of assets is shorter than liabilities, as is the case for the industry in general. Higher rates also raise risks, by creating incentives for policyholders to shop around for new policies at the same time that rising rates reduce the asset values.

The combination of lapse risk and asset risk can create liquidity or solvency concerns. With a few exceptions, these risks are contained.

On net, life insurers materially benefit from the current rate environment as demand and profitability rise in tandem. Ultimately, consumers stand to receive the majority of the benefits through higher crediting rates and more generous guarantees.

FAQ

Higher interest rates improve the profitability of life and annuity insurance. They increase investment returns and margins, making savings products more attractive, which boosts demand.

The life insurance industry has shifted from low growth and profitability due to low interest rates to higher growth and profitability, particularly for asset-intensive businesses, due to rising interest rates.

Profitability has recovered as higher government bond yields have increased investment returns. According to Swiss Re, insurers in major markets are projected to see a 60% increase in operating results over the next five years.

Higher interest rates make life savings products, like annuities, more attractive as they offer better returns. Consumers are buying these products to secure higher retirement incomes.

Rising interest rates tend to increase policyholder lapse rates, where individuals switch policies to seek better deals. However, the peak lapse risk has likely passed.

Private equity firms have acquired legacy assets and expanded their asset management capabilities. They now hold a significant share of US individual annuity liabilities.

While higher rates improve profitability, they can also increase liability and asset stress, leading to potential liquidity or solvency issues. However, most risks remain manageable.

……………

AUTHORS: Germante Boncaldo – Head of Reinsurance Business Development at Swiss Re, James Finucane – Senior Economist, Swiss Re Institute, Thomas Holzheu – Chief Economist Americas, Swiss Re Institute, Loïc Lanci – Economist, Swiss Re Institute, John Zhu – Chief Economist Asia Pacific Swiss Re Institute