While life insurers’ exposures to illiquid assets have been rising, it does not necessarily lead to unmeasured risks. Private and illiquid credit cannot be traded or sold and the lender is primarily exposed to default risk. Profitability is improving as well, with greater room for margins in new spread-based products and opportunity to reinvest assets backing legacy liabilities at a higher rate, according to Swiss Re sigma 2/2024.

The growing expectation that interest rates will remain higher for longer gifts the life insurance industry a far more favourable balance of risk and return for taking interest rate risks. It also reduces the pressure to seek yield enhancement through credit and illiquidity risks. All types of insurers are regaining risk appetite for holding assets and writing more asset-intensive business.

As private loans are typically valued relatively infrequently, there can be higher risk that a loan becomes impaired if they are not monitored closely.

Higher interest rates for life insurers put additional strain on borrowers’ ability to repay loans, and default rates on corporate debt in the US and Europe, though low, are beginning to rise. Corporate insolvencies are also increasing.

Life insurance savings products

Demand for life insurance savings products is surging, with US fixed annuity sales in 2023 more than twice as high as in any other year other than 2022. Insurers expect record sales in 2024 too.

It is essential that private credit investors monitor loans closely and are well protected by covenants and other loan clauses that give them recourse to take action should a borrower default on the debt (see Life Insurance & Retirement Savings Forecast).

Illiquidity is not of itself a risk for hold-to-maturity investors such as life insurers which do not require high levels of portfolio liquidity given their long-dated liabilities.

For long-dated illiquid asset classes such as infrastructure debt, life insurance capital can be an excellent fit with investment needs. IFRS17’s illiquidity assumptions illustrate how illiquidity is a recognised part of the life business model.

Commercial real estate: limited risk for life insurers

The corporate real estate (CRE) sector is a specific pocket of credit risk globally. Concerns are focused on steep valuation declines in the retail and office sectors as increasing home working and online shopping reduce demand for physical space.

U.S. life insurers’ commercial real estate exposure is predominantly via commercial mortgage loans, with more modest exposure to commercial mortgage backed securities (CMBS) at less than 5% of cash and invested assets, with equity real estate not a meaningful allocation.

Coupled with higher refinancing rates due to the rise in interest rates, this is reducing some property owners’ ability to refinance maturing loans, so leading to higher default risk.

In the US, over USD 900 billion of commercial mortgage loans – including 25% of all outstanding US office commercial mortgage loans – are due in 2024, according to Goldman Sachs.

The extent of the refinancing risk will depend on when interest rates begin to decline again. We see lower risk in Europe, where we expect interest rate cuts to begin earlier than in the US and peak debt maturity is only in 2026 with the maturity of about EUR 40 billion of loans.

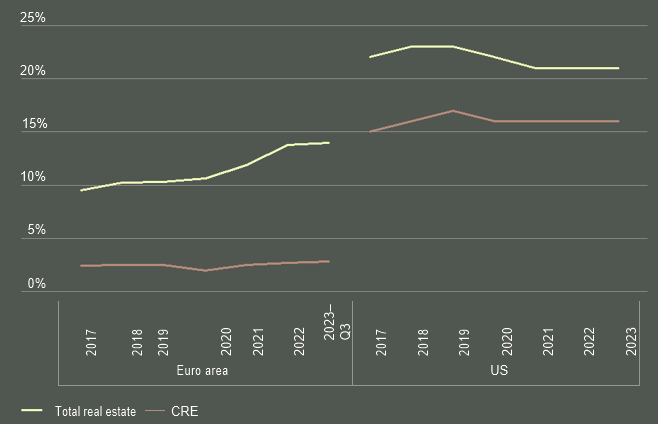

Life insurers’ total exposure to real estate assets

Euro area exposure is shown on a solo insurer basis. It excludes unit- and insurance-linked assets and CRE exposure excludes own use. For the US, CRE exposure includes CMBS and mortgage loans (excluding residential).

US exposures are based on NAIC statutory filings. CRE is defined as non-residential mortgage loans plus CMBS; total real estate exposure is CRE plus residential mortgage loans and RMBS. We use net admitted cash and invested assets for the denominator.

According to Global Life Insurance Industry Evolution report, US life insurers hold more than 20% of their portfolios in real estate assets, primarily mortgage loans. About a third of those mortgage books were in the office and retail sectors as of the end of 2022.

The life insurance industry in 2024 looks very different to 15 years ago. Low interest rates from 2008 until the inflation surge after 2021 put huge strain on the traditional life

Despite the relatively high exposure of US insurers to real estate, risks are viewed as manageable given the characteristics of these investments, such as low loan-to-value ratios, high debt service coverage ratios, low overdue/foreclosed loans on the whole loan side, and highly rated tranches of CMBS.

In Europe, direct and indirect exposures to CRE credit is stable at 2–3%, with below-average asset exposures in the largest life markets. In the UK, we estimate CRE exposure to be close to 7%. In South Korea, overseas CRE exposure is about 3% of the insurance sector’s total invested assets, concentrated in the US and mainly indirect via alternative investments.

Comprehensive capital requirements limit risky CRE exposures

For life insurers in Europe, CRE loans are subject to capital charges under Solvency II for the spread, currency and interest rate risks they carry, with higher charges for lower quality loans.

Mortgage loans comprised 13% of U.S. life insurers’ portfolios, approximately 85% of which were commercial mortgage loans (CML).

Capital requirements are also higher for unrated loans, especially when the risk-adjusted value of collateral is smaller than the risk-adjusted value of the loan.

Altogether, this limits risky exposures. According to Fitch, a 50% write-down of all direct and indirect CRE exposures would erode less than 10% of European life insurers’ capital base.

In the US, industry analysts consider life insurer portfolios to be relatively secure, benefiting from conservative underwriting on mortgage loans and spaced-out maturities.

……………

AUTHORS: Germante Boncaldo – Head of Reinsurance Business Development at Swiss Re, James Finucane – Senior Economist, Swiss Re Institute, Thomas Holzheu – Chief Economist Americas, Swiss Re Institute, Loïc Lanci – Economist, Swiss Re Institute, John Zhu – Chief Economist Asia Pacific Swiss Re Institute