Overview

The life insurance industry in 2024 looks very different to 15 years ago. Low interest rates from 2008 until the inflation surge after 2021 put huge strain on the traditional life insurance business model of using balance sheet leverage and investment income to deliver contractual promises to policyholders, according to Swiss Re sigma 2/2024.

Publicly traded life insurers missed return targets by nearly five percentage points per year on average between 2010 and 2019. Product mix and investment strategies evolved rapidly as a result. Insurers’ ownership structure was a key determinant of the industry’s responses.

Low public market valuations for “capital intensive” business incentivised stock (publicly listed) life insurers to exit core lines of business and divest assets.

Mutuals continued to offer traditional products, but with crediting rates and guarantees in line with the low-yield environment.

Private equity firms entered the sector, acquiring legacy book assets from stock insurers via reinsurance transactions, to fund and expand their private credit operations.

According to Life Insurance & Retirement Savings Report, asset management diversified into private assets, longer duration and overseas markets, becoming a key component of insurers’ hunt for yield above low risk-free rates. European insurers’ illiquid asset allocations have risen by 5–7 ppts on average.

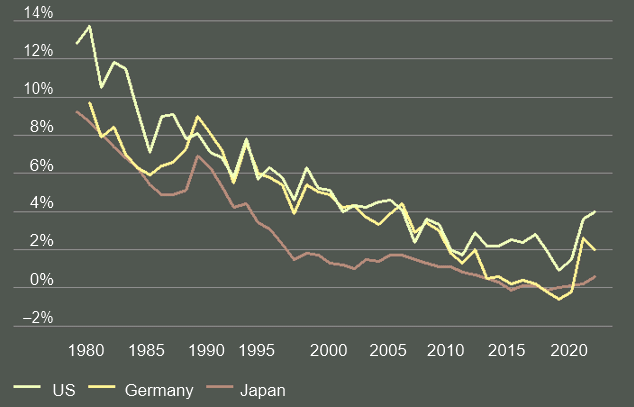

Life insurance is highly sensitive to interest rates

The life insurance industry is experiencing its most significant change since the de-mutualization wave of the late 1990s and early 2000s. The prolonged low interest rates from the 2008–2009 global financial crisis until after 2021 prompted changes in new business products, types of business insurers hold, and their asset management strategies.

Product design issues became evident as interest rates in the US and Europe remained near zero. High minimum interest rate guarantees, feasible when yields were higher, became unsustainable promises.

Overly optimistic assumptions for lapse-supported products led to significant reserve charges.

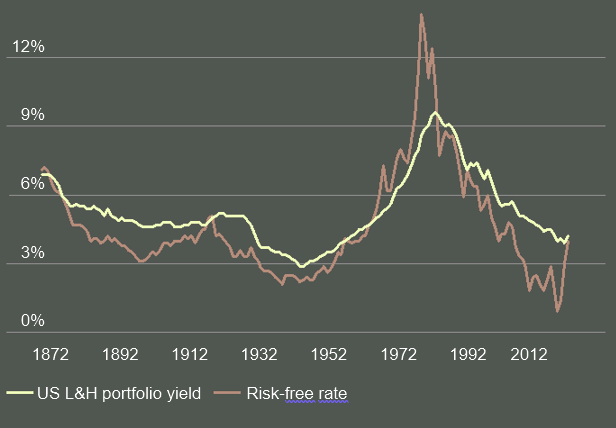

10-year government bond yields, 1980–2024

Insurers responded by updating products and liability assumptions, reducing guarantees for new business, and strengthening reserves for existing contracts.

These actions made products less attractive and reduced demand for new business.

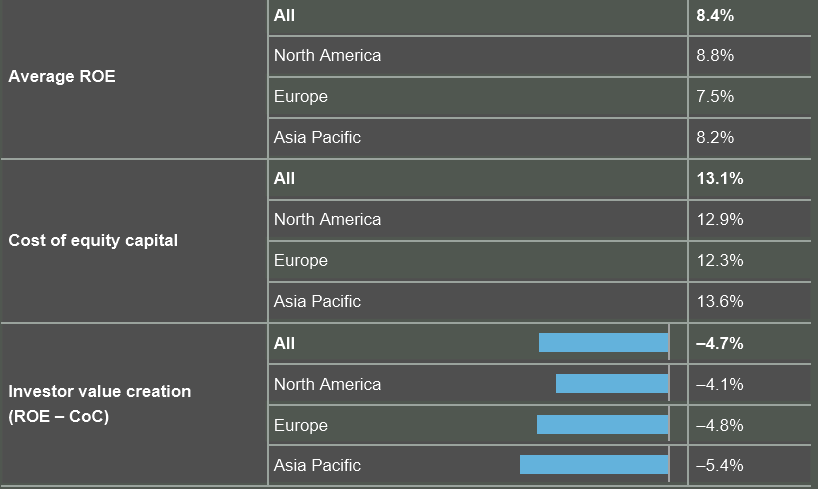

Traditional life insurance profitability well below cost of capital

The traditional life insurance model involves significant leverage, with assets about 10 times equity, as insurers invest funds to meet future obligations. Consequently, low interest rates decrease net investment income’s contribution to return on equity (ROE) more than the reduction in the cost of capital, which generally follows the risk-free rate.

Over time, life insurance portfolio yields closely align with interest rates, significantly impacting industry and policyholder returns.

Publicly traded life insurers failed to meet return targets during the low interest rate years of 2010–2019. Investors in public markets prioritized capital efficiency for short-term profitability over growth and scale at lower margins.

Publicly traded life insurers’ earnings relative to cost of capital

They focused more on cash-based metrics and shareholder distributions, valuing fee-based earnings higher than spread-related earnings.

Analyses by sell-side analysts indicate that fee-related earnings receive a higher price-to-earnings multiple compared to spread-related earnings.

Thus, stock insurers that shift to asset-light earnings benefit from a higher stock price in the short term. However, the advantages of asset-intensive business in a higher interest rate environment may alter this assessment.

Low interest rates led stock insurers to pivot toward capital-light strategies

This led many large, publicly traded re/insurance groups in Europe, North America and Asia to shift their business models, selling blocks of asset-intensive business – which are generally accompanied by capital requirements and thus considered “capital-intensive” – and competing for “capital-light” revenue streams.

Capital-intensive business typically relies on earning a spread between general account investment yields and guaranteed crediting rates or other commitments.

Capital-light business refers to fee-based income including, for example, earnings from unit-linked products in which investment risk is borne by policyholders.

Justification for the strategic pivot to capital-light business appeared to be reinforced as interest rates declined. A lower discount rate increases the present value of fee-related earnings and is associated with an increase in AUM, the basis for determining fees.

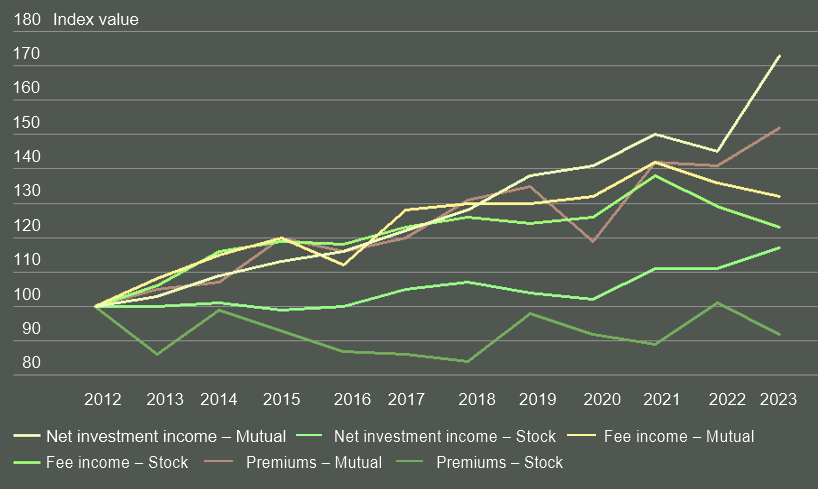

Public insurers’ fee income growth outpaced net investment income during the low interest rate period, but these trends have reversed since 2021, with fee income shrinking.

Overall growth has been muted. The public US life insurance industry’s net investment income increased by 17% and fee income increased by 23% from 2012 to 2023 ‒ less than 2% compound annual growth rates.

Stock insurers’ net premiums declined 8% over the same period, partly reflecting offshore reinsurance transactions for legacy business.

Private equity capital provided the demand for assets that public companies divested

Many reinsurance transactions involved PE-owned reinsurers, focusing on annuities. These products carry higher investment risks compared to traditional life insurance. PE firms pursued these assets for management fees and spread-related earnings.

Reinsurance transactions exploited differences in capital requirements, tax rates, investment rules, and valuation philosophies between private investors and public shareholders.

This allowed them to offer attractive pricing to cedents. Additionally, post-financial crisis regulations made certain types of lending more capital-efficient for non-bank institutions, further motivating PE firms.

In Europe, supervisory oversight has increased with the rise of unit-linked offerings. In 2021, the European Insurance and Occupational Pensions Authority (EIOPA) highlighted the need for a common framework to manage value-for-money risks in unit-linked products, focusing on pricing, complexity, and testing.

The UK has also seen a push for customer-centricity with the Financial Conduct Authority‘s new consumer duty rules, mandating that insurers demonstrate fair value to customers.

Mutual insurers continued to grow despite lower returns

In contrast to public insurers’ drive to minimise balance sheets and pursue fee revenues, mutual insurers continued to offer traditional protection and savings products despite the constraints of low interest rates.

With policyholder ownership, mutual insurers’ primary purpose is to provide attractive returns and useful products to members over time, rather than meet short-term profit expectations or provide a return on capital for external investors.

Their decision-making is typically based on a longer timeframe and is less affected by the leveraged impact of risk-free rates on return on equity.

This approach led to stronger organic growth and higher net investment income. From 2012 to 2023, US mutual insurers saw a 73% increase in net investment income, with their investment portfolios nearly doubling in size.

Gains in net premiums also boosted mutuals’ growth in net investment income.

Fee income for mutual insurers rose by about 32%, compared to 23% for stock insurers, indicating potential scale advantages.

If rates stay high, insurers with large balance sheets supporting general account liabilities can achieve greater earnings relative to their cost of capital over time.

Growth in net premiums, net investment income and fee earnings for stock and mutual insurers

The decline in interest rates also changed life insurance asset management. To offset low interest rates after the financial crisis, life insurers, like many other investors, grew their exposures to higher yielding asset classes.

The hunt for yield turned insurers in Europe, North America, and Asia to assets such as structured and private credit, floating rate loans, longer duration securities and looking abroad for markets with higher-yield investment opportunities.

Private assets typically reward investors with a premium over similar publicly traded securities in recognition of their illiquidity, or lack of trading opportunities.

Companies that tap the private credit market also tend to be smaller and carry more debt relative to earnings than counterparts with publicly traded bonds.

Private credit usually has floating rates, while public debt typically has fixed rates. Rising interest rates boost yields for floating-rate debt but also increase risks. Higher payments can lead to more covenant breaches and defaults. Despite this, borrowers have remained resilient in the current cycle.

Illiquidity is essential for the life insurance business, as its long-term liabilities support investments in illiquid and long-dated assets.

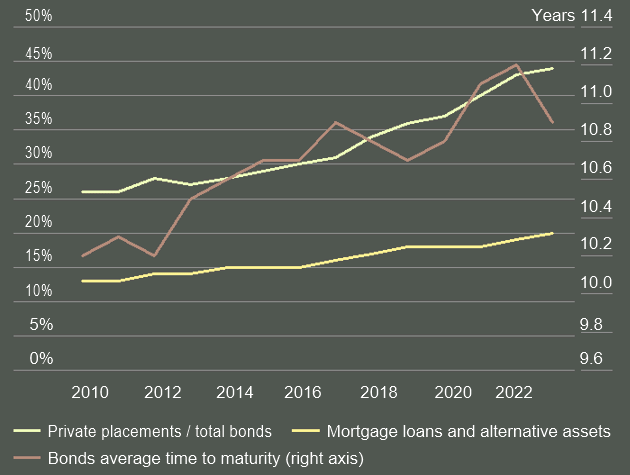

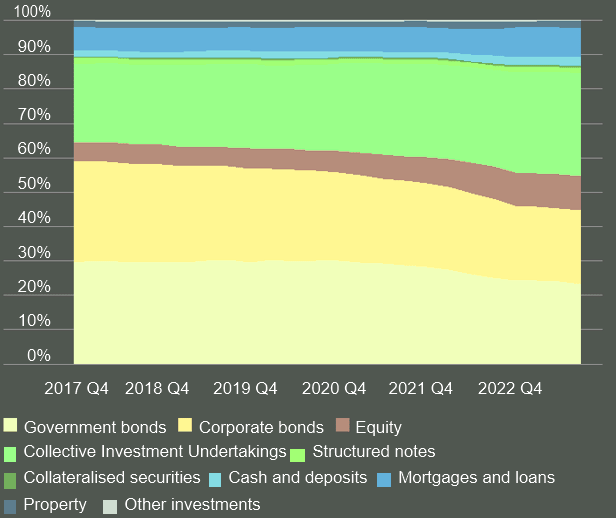

From 2017 to 2023, US life insurers reduced direct corporate debt holdings, shifting towards real estate and alternative investments.

US life insurance industry portfolio allocations

US interest rates and L&H insurance industry portfolio yield

By the end of 2023, securitizations, real estate, and other alternatives made up 39% of investment portfolios, up from 34% in 2017. Bond portfolio durations increased, averaging 11 years to maturity in 2022, compared to nine years in 2008.

Allocation to private placement securities has also risen over the period to 43% of fixed income investments from 24%. This trend towards greater private placement is not unprecedented and we expect it has further room to grow.

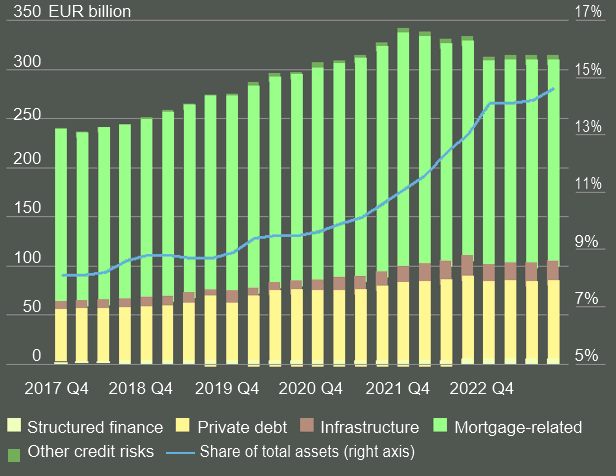

European life insurers have also allocated more to higher yielding private and illiquid assets. Swiss Re estimate that about 15% of European insurers’ portfolios backing traditional saving product liabilities were invested in illiquid assets and potentially risky exposures in 2023, up from 8% in 2017.

About a third (30%) of assets were allocated to pooled third-party private assets funds including real estate, infrastructure, and PE in 2023, up from 23% in 2017.

European life insurance industry portfolio allocations

European life insurers’ estimated illiquid and risky investments

In the UK, life insurers hold about a 25% allocation to illiquid credit, primarily in commercial mortgages, infrastructure debt and private debt. Meanwhile, capital quality has remained relatively stable since 2017, according to data published by the Bank of England.

Drivers for the rise of private equity

Private equity players met the demand of stock insurers seeking to pivot away from their legacy business. Regulatory changes after the global financial crisis, which accelerated non-bank lending as a new asset class, supported the move.

These companies seized an opportunity to establish a foothold in the life segment, expand their asset base and grow private lending operations in a hunt for yield that was impacting the broader asset management industry.

Private equity firms have generally followed one of three strategies in the insurance industry, acting as (1) pure reinsurers and liability originators, (2) run-off reinsurers and liability consolidators or (3) insurance asset managers.

Both liability originators and consolidators focus on accumulating annuity liabilities, typically using affiliated offshore reinsurance to lighten capital requirements. Originators focus on reinsurance business (flow or closed block) and have manufacturing and distribution capabilities, while consolidators focus on reinsuring runoff business.

Companies following the insurance asset management strategy primarily rely on insurers’ desire for higher investment returns and demand for increased direct origination / private credit capabilities to grow through investment management agreements.

Swiss Re estimate that private equity-affiliated reinsurance vehicles have accumulated more than USD 1 trillion in global life insurance assets since 2009. Although most have been acquired from US carriers, a significant amount are from Europe.

The private equity industry overall is US-centric as well, with US companies accounting for more than 70% of global assets under management, and seven of the top 10 global PE firms based in the US.

Growth in PE-owned life insurers has been particularly high for the last six years with 11 of the top 18 vehicles formed since 2018. Listed life insurers have ceded these assets as blocks of business to enable a strategic realignment of their business and/or to de-risk their balance sheets.

Private equity in Europe: opportunity and barriers to entry

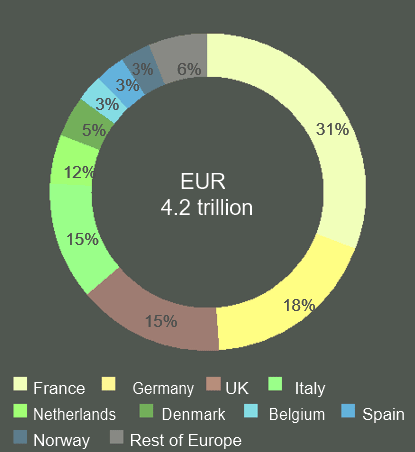

With over EUR 4 trillion of liabilities to tap, the European life sector offers significant potential for consolidation due to its fragmented markets and distribution networks. PE vehicles have entered the European life market in small numbers.

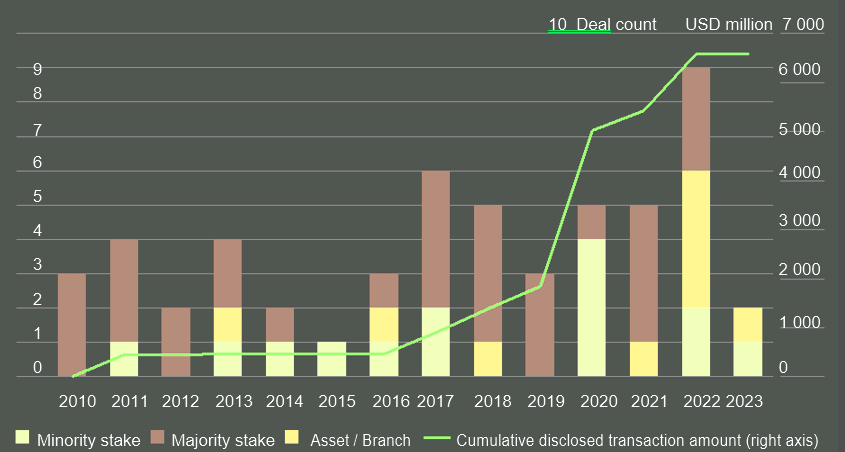

Since 2010, we estimate that there have been 54 transactions with PE influence, accounting for 7% of all reported M&A activity.

Life insurance liabilities in Europe

Number of PE-influenced deals in Western Europe

Initially dominated by majority stake acquisitions, the activity has evolved towards minority and asset/branch consolidations. Transaction value has surged since 2019 after a series of landmark deals in the Netherlands, the UK, Germany and Italy.

Establishing a presence in the European life insurance market presents several challenges due to significant entry barriers. In France, large bancassurance and insurance groups dominate the market, utilizing established broker networks and work-based arrangements. Local employment laws further complicate entry for foreign companies.

In Germany, life insurance companies are looking to offload legacy portfolios that require substantial capital. This creates opportunities for consolidators, but they must adhere to conservative reserving rules. Italy’s market has seen significant consolidation recently, including involvement from private equity players.

In the UK, higher interest rates have improved funding levels in defined benefit pension schemes, leading to record buyouts worth GBP 49 billion in 2023, a 73% year-over-year increase, according to the Association of British Insurers (ABI). De-risking volumes are expected to peak in 2026–27.

In the Netherlands, pension reforms in 2023 have paved the way for an estimated EUR 1.5 trillion in pension risk transfer (PRT) transactions, with three transactions already completed.

…………….

AUTHORS: Germante Boncaldo – Head of Reinsurance Business Development at Swiss Re, James Finucane – Senior Economist, Swiss Re Institute, Thomas Holzheu – Chief Economist Americas, Swiss Re Institute, Loïc Lanci – Economist, Swiss Re Institute, John Zhu – Chief Economist Asia Pacific Swiss Re Institute