Overview

- Traditional shipping practices are breaking apart

- Marine hull premiums climb amid soft cycle, rising risks

- Marine insurers face rising claims

- Marine insurers weigh war volatility as fleet value climbs

- Marine insurance rates firm as war risk and global trade shifts drive demand

- Cargo insurance steady but MGAs reshape competition in marine market

Marine underwriters are staring at one of the most punishing runs in memory. A soft market, heavy insurance losses, and fractured trade flows are reshaping risk across global shipping. Beinsure analyzed the AM Best’s review and highlighted key points.

According to Gallagher Specialty, the marine insurance sector has been rattled over the past year by armed attacks in the Red Sea and Ukraine, plus high-profile fires. Those claims touch both standard hull and war covers, with premiums running large.

The International Union of Marine Insuranc president Frédéric Denèfle said conflicts are tearing at assumptions that once underpinned shipping.

Seamless globalization, he told attendees, is gone. National interests now edge out cooperative trade frameworks. The consequences ripple through underwriting and pricing.

Key Highlights

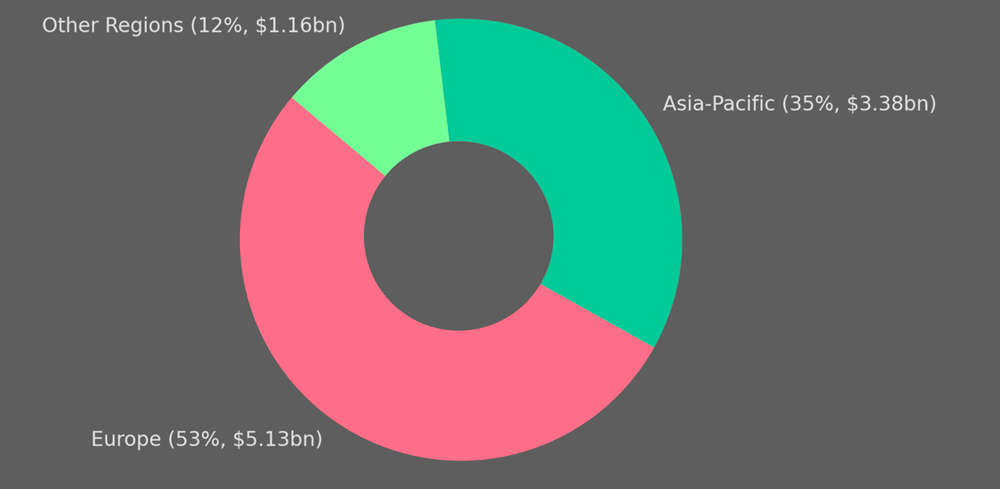

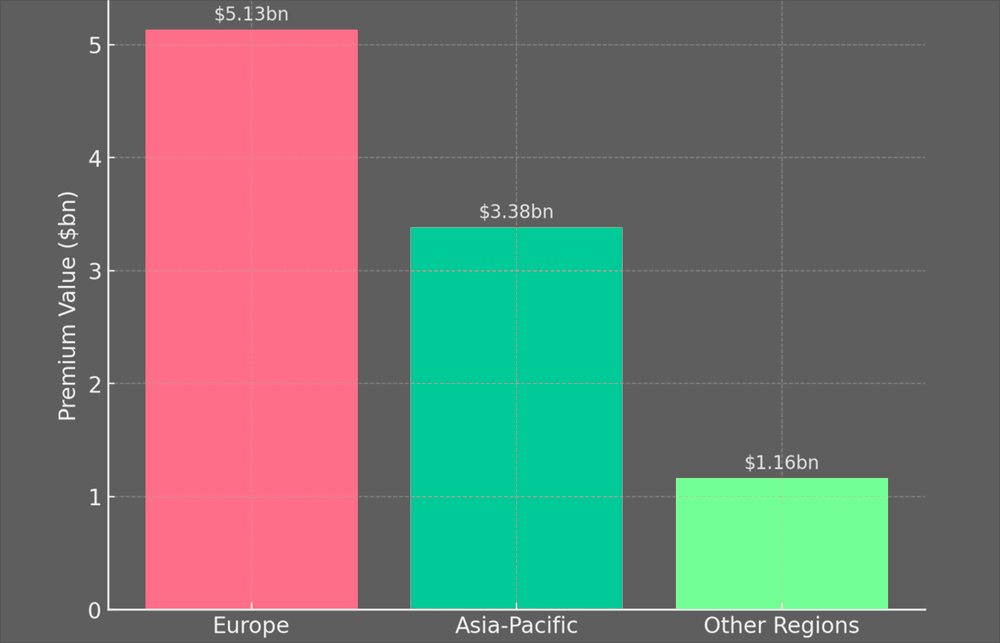

- Hull premiums rose 3.5% to $9.7 bn in 2024, with Europe and Asia-Pacific dominating the market, creating exposure risks if a major loss strikes those regions.

- Soft pricing pressures persist as incumbent carriers expand capacity, while two decades of historic losses still haunt profitability in marine hull.

- Geopolitical shocks (Ukraine, Red Sea, piracy) reshape trade flows, forcing ships onto longer, riskier routes and amplifying demand for war and political risk cover.

- Lloyd’s and major carriers see renewed momentum in marine lines, with Beazley and Skuld reporting strong MAP growth and improved balance sheets despite turbulence.

- Managing general agents (MGAs) enter aggressively, filling niche coverage gaps but also risking oversupply if too many lack differentiation.

Traditional shipping practices are breaking apart

“Traditional shipping practices are breaking apart,” Denèfle said. Routes get longer, riskier, and costlier as carriers avoid dangerous waters. Inland transport and nearshoring may rebound, Beinsure noted.

Rising costs push inflation higher. Reworked supply chains demand new port infrastructure. Artificial intelligence, fresh trade corridors, and emerging markets creep into the mix.

The picture inside hull insurance looks no easier. Ilias P. Tsakiris, chair of IUMI’s Ocean Hull Committee, said the market is slipping back toward softness. At the same time, exposures mount. Aging vessels, severe claims, geopolitical shocks, and the messy complexity of the energy transition are driving risks upward even as premium growth lags.

For marine insurers, the outlook is rough water: thinning margins, swelling claims, and a world trade system that no longer runs smooth.

Marine hull premiums climb amid soft cycle, rising risks

Global hull premiums grew 3.5% to $9.67bn in 2024, according to industry figures. Europe captured about 53% of that base, Asia-Pacific took 35%, and the rest of the world filled out the remaining 12%, Beinsure noted.

The concentration in just two regions, observers warn, leaves the sector exposed if a major loss lands in a premium-heavy center.

Mike Ingham of Gallagher Specialty said the past 18 months reflect a soft cycle. Not many new players entered, but incumbents want to push capacity, write bigger lines, and grab more accounts.

Global Hull Premiums

| Region | Share (%) | Premium Value ($bn) |

| Europe | 53 | 5.13 |

| Asia-Pacific | 35 | 3.38 |

| Other Regions | 12 | 1.16 |

That appetite keeps pressure on rates. Both Lloyd’s and the wider market are expanding, with Lloyd’s authorizing syndicates to stretch further into marine.

Hull remains a marginal slice of the book for many insurers, Ingham added, and only works when pricing holds. Two years of rate hikes offered relief until 2022.

Before that, twenty straight years of cuts and losses scarred the market. Now, with softening back in play, profitability looks fragile again.

Perception also weighs on pricing and sentiment. “Headlines make it feel like an extremely risky year,” said Rich Soja, global head of marine at Allianz Commercial.

Conflicts in the Red Sea and Ukraine dominate attention. “It’s in everyone’s faces,” he said, shaping how risk is viewed regardless of the actual loss experience.

Global Fleet Value Growth

| Year | Fleet Value ($tn) | Growth (%) |

| 2023 | 1.48 | 3.0 |

| 2024 | 1.54 | 4.0 |

For marine hull insurers, the cycle feels familiar: modest premium growth, plenty of capacity, and geopolitical heat that makes clients anxious but does not guarantee sustainable rates.

Marine insurers juggle fires, piracy, and geopolitics

Maritime risks tied to conflicts and piracy aren’t new. Underwriters expect containership fires or hijack attempts every year, and the war market adjusts for geopolitical flashpoints, Beinsure noted.

What’s different now is the volume of attention – heightened by Ukraine, the Red Sea, and the way headlines amplify perception.

Even with the turbulence, some carriers are posting solid numbers. Marine mutual Skuld reported a stronger fiscal first-half member balance, crediting improved underwriting and investments.

Marine insurers face rising claims

Marine mutual insurers and P&I Clubs are planning rate hikes for 2025 year, driven by rising claims and inflation pressures. Marine mutuals are under growing pressure from inflation and increased claims severity, according to A.M. Best research. S&P Global Ratings expects most P&I clubs will achieve near-breakeven results in financial year 2025.

S&P expected an average combined ratio of 100-105% for financial year 2025. The average combined ratio was 95% in financial years 2024 and 2023.

Yet interim results from clubs that publish half-yearly reports suggest that the average combined ratio might deteriorate in financial year 2025.

Shipping losses have sunk to the lowest number we have seen in the 12-year history of our annual study reflecting the positive impact safety programs, trainings, changes in ship design and regulation have had over time.

Fire and explosion incidents cause the most expensive insurance claims in the marine industry, while at a time of rising exposures and inflation, cargo damage is the most frequent cause of loss, according to AGCS’s Top Causes of Claims in Marine Insurance. Allianz analyzed more than 240,000 marine insurance claims worldwide, worth approximately €9.2 bn in value, and has identified a number of claims and risk trends that are driving major loss activity in the sector.

Regional Market Concentration

| Region | Share (%) |

| Europe & Asia-Pacific Combined | 88 |

| Other Regions | 12 |

President and CEO Ståle Hansen said the group remains on guard. Political tensions and economic uncertainty weigh on operations, but careful risk management and financial strength help shield members. Technical and investment performance both moved positively, he added.

“We acknowledge the impact of ongoing geopolitical instability on our operations. The global landscape, marked by political tensions and economic uncertainties, poses challenges.

Ståle Hansen – Marine mutual Skuld President and CEO

“We remain vigilant and adaptable to these external pressures, helping Skuld’s membership and clients to continue to navigate these turbulent times with careful risk management and financial strength,” Ståle Hansen said.

At Lloyd’s, Beazley highlighted marine, aviation, and political risk as its fastest-growing segment. Other lines softened, dragging first-half net income lower, but MAP expansion offset some of that. Demand surged for contingency products along with political risk, terrorism, and war covers.

Fleet Value & Exposure

| Metric | 2024 |

| Fleet Value ($tn) | 1.54 |

| Growth (%) | 4 |

| Exposure Comment | Higher exposure due to fleet value rise |

Across Europe, coastal states are tightening oversight of tankers suspected of carrying sanctioned Russian crude oil by demanding proof of valid insurance, Oleg Parashchak, CEO Financ Media, said. This shadow fleet often consists of aging vessels operating under obscure ownership, switching flags frequently, and relying on low-tier or state-backed insurers that may not cover major oil spills or costly salvage operations.

By targeting insurance—a weak link for the shadow fleet—authorities make opaque operations less viable and raise the cost of non-compliance.

- Norway’s new six-month pilot, led by the Ministry of Trade, Industry and Fisheries, asks tankers in its Exclusive Economic Zone to voluntarily disclose insurance details. The Norwegian Coastal Administration contacts vessels, while the Norwegian Maritime Authority verifies documents. Though no penalties apply for refusal, noncompliant ships risk deeper inspections when entering ports.

- Similar measures are already in place in Sweden, Finland, Denmark, Germany, and the UK. These countries share data to identify high-risk vessels, closing gaps in enforcement. Early results show more than 90% of contacted ships eventually submit documentation, helping regulators assess environmental and safety risks.

This coordinated approach aims to protect marine ecosystems, critical infrastructure, and regional security from the growing risks posed by poorly regulated tankers.

Marine insurance brokers are responding too

Willis unveiled a $200 mn facility dubbed “Undercover,” built with Markel to combine protections against geopolitical exposures for global cargo owners. The firm pitched it as a single proposition for clients facing overlapping risks in unstable regions.

The story across the marine sector isn’t one of collapse but of recalibration. Fires, piracy, wars—familiar threats. What’s shifting is how insurers balance softer markets with client demand for broader, sharper protection.

Marine insurers weigh war volatility as fleet value climbs

The global fleet rose 4% in value last year, reaching $1.54tn. Ilias P. Tsakiris said the surge, paired with brisk sale-and-purchase activity, reflected economic confidence but also ramped up exposure for insurers.

War risk now looms larger

Allianz’s Rich Soja argued the marine insurance ecosystem remains strong enough to absorb the pressure, though volatility is unmistakable. Gallagher’s Mike Ingham noted the war market itself is splitting. Some underwriters stay active, others see the risk as too unstable to touch.

War cover has always skewed toward tiny premiums punctuated by rare, outsized losses. But the current environment looks different.

In the Red Sea and Gulf of Aden, vessel traffic fell by as much as 70% at one stage, compared with the hundreds of ships once moving through weekly. “The rates and stakes are higher,” Ingham said. “Underwriters are going in with their eyes open.”

Global Hull Premiums Share by Region

Tim Prince of AM Best framed marine as a sprawling, sometimes complicated global risk. Carriers often pick their spots, concentrating on particular slices rather than the whole.

That specialization might become even more important as fleet values climb and geopolitical instability keeps reshaping trade routes.

Marine insurance rates firm as war risk and global trade shifts drive demand

War risk sits with specialist underwriters, Tim Prince of AM Best said, while hull and cargo typically run short-tail. For years, rates softened, but pricing has firmed again, most noticeably on complex liability lines.

- Demand still tracks global trade. If tariffs drag volumes lower, insurers will feel it. Whether that drag is temporary or structural remains unclear.

- Energy shipments add another dimension. Oil and gas move primarily by sea, so coverage needs swing with demand for those commodities. The war in Ukraine has already shifted sourcing and routes, creating knock-on effects for risk placement.

Marine business is often written through specialist brokers, with delegation common. Lloyd’s continues to stand as a major hub.

Terrorist attacks on vessels also fall under war risk, which remains a narrow but critical discipline. Lloyd’s has even flagged marine as a segment to watch, Prince noted.

It wasn’t long ago that marine underwriting was bleeding red. Rachel Turk, chief underwriting officer at Lloyd’s, reminded the market that subclasses once faced direct intervention after years of losses.

Marine, along with aviation and property treaty, had watched premium volumes sink sharply across the past decade. The current firming offers some relief, but history shows just how fragile those gains can be.

Cargo insurance steady but MGAs reshape competition in marine market

Cargo has held steady despite a rough backdrop. Rachel Turk of Lloyd’s pointed to a five-year trend showing the class broadly adequate, though activity stalled during the COVID-19 years.

For big multiline carriers, cargo serves another purpose. Mike Ingham of Gallagher said it works as a diversification line, non-correlating and non-aggregating like aviation, giving balance to portfolios.

Competition, though, is shifting. Allianz’s Rich Soja noted that many new entrants are MGAs. Some bring longevity because they focus on underserved niches, carving out gaps the majors overlook. Allianz sometimes partners with those players, offering capacity.

Still, the model cuts both ways. Too many MGAs chasing the same space without a real edge can crowd the market and push oversupply. Soja said it comes down to differentiation—those that stick to sharp, narrow products may endure, while others risk fading fast.

FAQ

Because they face a triple squeeze: a soft market, heavy claims from fires and conflict, and fractured global trade flows. Gallagher Specialty said the Red Sea and Ukraine crises rattled the sector, adding to already large hull and war losses.

Frédéric Denèfle told the Singapore conference that seamless globalization is over. National interests now override cooperative trade, disrupting long-standing shipping practices, pushing vessels onto longer and costlier routes, and reshaping underwriting models.

Industry data showed hull premiums up 3.5% in 2024 to $9.67bn. Europe accounted for 53%, Asia-Pacific 35%, other regions 12%. The concentration makes the market vulnerable if a major loss hits one of those premium-heavy centers.

Volatility. Some underwriters continue to write business, others pull back. The Red Sea and Gulf of Aden once saw hundreds of ships a week; at one point traffic fell 70%. “The rates and stakes are higher,” said Gallagher’s Mike Ingham.

Some are. Skuld posted a stronger first-half balance on underwriting and investment gains. Beazley saw marine, aviation, and political risk become its fastest-growing segment, even while softer lines dragged net income down.

Marine demand tracks global trade. Tariffs can slow volumes, though it’s unclear if that drag is temporary. Energy shipments—mostly oil and gas—still move by sea, and the war in Ukraine has already shifted global supply chains. Cargo insurance stayed adequate through a five-year stretch but went quiet during the COVID-19 years.

They’re reshaping competition. Some MGAs thrive by filling ignored niches, creating long-term viability and drawing in capacity from players like Allianz. But oversupply is also a risk—too many MGAs offering lookalike products without differentiation can crowd the space.

……………….

QUOTES: Mike Ingham – executive director of marine hull at Gallagher Specialty, Frédéric Denèfle – International Union of Marine Insuranc president, Rich Soja – global head of marine at Allianz Commercial, Ståle Hansen – Marine mutual Skuld President and CEO, Rachel Turk – chief underwriting officer at Lloyd’s

By David Pilla – AM Best, Edited by Yana Keller — Lead Re/Insurance Editor of Beinsure Media